{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

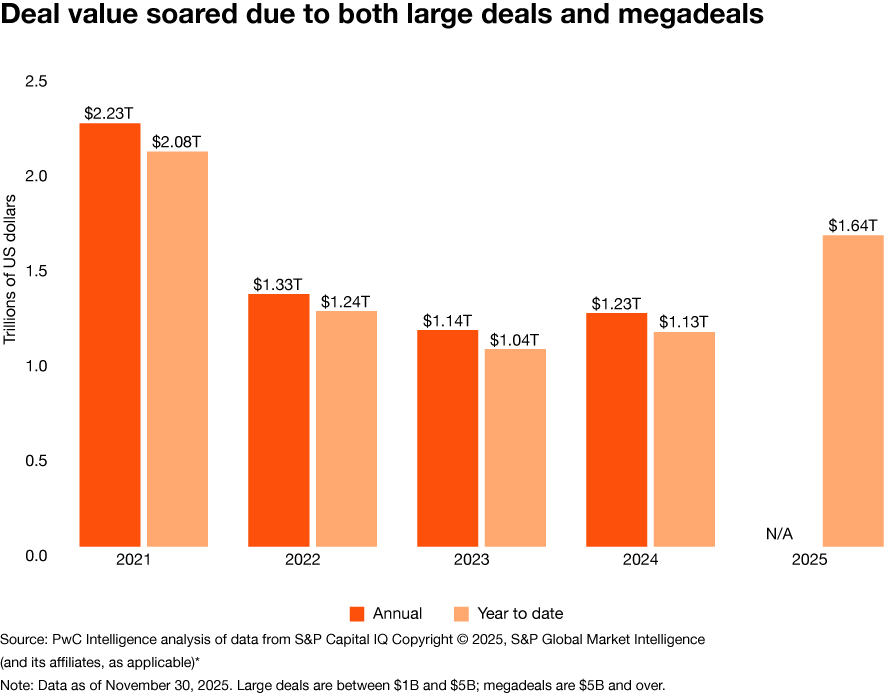

Driven by an AI boom and revitalized private equity (PE) activity, the market notched 10,333 deals worth a whopping $1.6 trillion through November 30, 2025. Even amid major shifts in economic policy—such as tariffs—total deal value rose about 45% from last year and was the second highest ever recorded. While deal volume was only up about 2% over last year, it was still the third largest number in the past decade.

The transformative potential of AI helped drive activity among tech companies—especially in regard to megadeals. More than 20% of this year’s 74 deals valued at $5 billion or more have an AI theme.

Private equity provided another boost. For several years, sponsors have been grappling with valuation gaps created by pre-COVID era exuberance combined with higher interest rates. As economic and monetary conditions changed, sponsors found they could no longer rely on valuation multiples to expand as they had in the prior decade. The subsequent valuation gaps complicated exits and extended portfolio company hold times.

Even so, sponsors still have plenty of dry powder and they deployed it more freely this year. Financial buyer deal volume, which includes PE activity, ticked up about 4% to 1,484 transactions as of November 30, 2025, while M&A value vaulted 54% to $536 billion. By comparison, corporate buyer volume was up about 2% to 8,849 while value rose 41% to $1.1 trillion.

Looking forward, we see some existing market challenges continuing in the year ahead: China-US trade tensions, an uncertain jobs market, and balancing interest rates with the persistent specter of inflation. Yet there’s also reason for optimism. The business and profit cycles are the most important drivers of M&A. From 1990 to 2024, announced deal count rose in almost 90% of years when the economy and profits expanded. With real GDP and S&P 500 EPS expected to grow next year, the macro backdrop should generally support dealmaking.

“For industrial manufacturers, 2026 brings a rare mix of pressure and momentum. Cost and supply-chain challenges persist, but interest rates, AI buildout, and energy infrastructure development are creating real opportunities. It’s a moment where disciplined, well-timed M&A can strengthen our position for the long run.”

“We're seeing a shift from opportunistic acquisitions to purpose-driven partnerships,” one CFO at an electrical contracting company observed. “Companies aren’t just buying scale, they're buying specialization, geographic reach, and management capabilities. Valuations are climbing, driving more firms to consider transacting but at the same time, certain geographies and market segments are seeing slow or stagnant growth due to macro-economic factors such as tariffs and interest rates.”

“We're seeing a shift from opportunistic acquisitions to purpose-driven partnerships. Companies aren't just buying scale, they're buying specialization, geographic reach, and management capabilities.”

California led the way with 13.4% of acquirers, primarily driven by software-related deals and other technology acquisitions. Many of the larger acquisitions aligned with demand for artificial intelligence, cybersecurity, and semiconductors. Private equity buyers led deal-making in No. 2 New York, focusing on targets across diverse sectors such as pharmacy, footwear, and electric utilities. While the largest deal announced by a Texas buyer was in the household products industry, transactions related to oil and gas set the third place Lone Star State apart.

“Companies who are viewed to benefit from AI tailwinds are seeing outsized multiples and deal activities; companies where AI is viewed to be a detractor, or if the AI impact is cloudy, may have no bid.”

Hundreds of billions of dollars have been poured into AI investments, from data centers and microchips to new software development. Even amid concerns over a potential stock market bubble, AI is significantly accelerating software and consumer goods development. Industries with longer R&D horizons, such as pharma and automotive, also are seeing incremental gains. AI is driving investment opportunities for hyperscalers, private credit, and sovereign wealth funds, among others.

M&A leaders must now prioritize assessing the AI readiness and potential impact for deal targets. Will AI-driven use-cases be a competitive advantage or a meaningful disruption risk? Investment targets that are AI enabled—whether to drive operating efficiency or product differentiation—are seeing distinct outcomes.

Technology-focused private equity firms are clearly noticing this difference. For instance, “while we see elevated M&A activity in the tech market, there is a dichotomy between companies who receive outstanding outcomes, and no outcome,” says Ramzi Ramsey, a senior managing director at Blackstone Growth. “Companies who are viewed to benefit from AI tailwinds are seeing outsized multiples and deal activities; companies where AI is viewed to be a detractor, or if the AI impact is cloudy, may have no bid.”

Middle market activity, which often depends more on macroeconomic fundamentals than larger deals, was underwhelming in 2025 and will likely need to grow for overall volume to improve substantially.

Tariff shocks and stricter immigration enforcement were among the factors that hindered GDP growth in 2025. That made it tough for mid-sized firms to chart a path to higher revenues and strong margins. Tariff policy shifts also created uncertainty—making forecasting harder and forcing many businesses to rethink supply chains.

For now, trade policy is stabilizing, which is good for executive confidence and M&A. Policy is obviously subject to potentially sudden changes, however, which could have a negative effect on both. Interest rate cuts this year have already helped mid-tier corporates, and further Federal Reserve Board action in 2026 could go a long way in relieving pressure on them.

However, continued trade policy volatility would reinforce an existing dynamic in which the biggest companies and PE firms are the most active M&A players. Scale gives large firms resilience, enabling them to fund deals even when financial conditions tighten. Large firms also are better positioned to secure trade exceptions from the government than smaller companies.

The potential middle-market swing factor for 2026 is the role of private equity buyouts and exits. PE firms now hold more dry powder and older portcos than during prior large-deal cycles, which could drive additional volume if financing conditions remain favorable.

But valuation gaps are still making it harder for funds to exit and provide returns to limited partners—in turn putting pressure on fundraising. While many funds have capital to invest, they remain cautious. We also believe that shifts in PE buyer behavior, including the use of platform roll-up strategies, help explain some of the decline in middle-market deals.

Competition for quality middle-market assets is likely to pick up though. As sponsors have become pickier about their investments, more large funds have turned to the middle market to find opportunities. Smaller funds will likely need to focus on specific sectors or subsectors to remain competitive. They may also seek to differentiate themselves by bringing in operating partners that can strengthen operations at their portfolio companies.

We expect PEs will continue to deploy various continuation strategies. Longer hold periods do create more potential for value creation, however. Funds that can navigate this dynamic by acting quickly on quality assets and improving the performance of portfolio companies—such as through increased focus on value creation and unlocking the AI opportunity in their business—will be best positioned to navigate these challenges in 2026.

“The 2025 M&A market was defined by AI-powered big deals. Looking ahead, we anticipate a more broad-based recovery as regulatory policy comes into focus and GDP growth expectations actualize, which will better position the middle market to actively participate in the M&A resurgence.”

The IPO market sprang to life early in the second half of 2025 with investors eagerly greeting new offerings. That pent-up demand, plus interest rate trends and growing stability around trade policy, should bode well for 2026 IPOs.

Through November 30, a total of 72 traditional IPOs raised $33.6 billion—surpassing the full-year totals of 2024 (62 IPOs; $27 billion), 2023 (35 IPOs; $17.7 billion), and 2022 (28 IPOs; $7.1 billion). SPAC issuance also posted its most active stretch since 2021, with 122 SPACs raising over $22 billion.

Unfortunately, the strong run hit a significant speed bump due to the government shutdown, which we expect will have several important consequences. First, regulators will need to clear a sizeable backlog; the SEC said issuers filed more than 900 registration statements during the shutdown. IPO candidates and others wishing to access the capital markets should expect delays as the SEC works through accumulated filing reviews.

This backlog will be exacerbated by pent-up demand. Companies that delayed filings during the shutdown may try to list quickly, particularly AI or tech firms that want to capitalize on favorable valuations before any potential policy shifts. The first few IPOs of 2026 may also see conservative pricing as markets recalibrate, followed by potential premium valuations for high-quality issuers as confidence rebuilds.

Technology, healthcare, and industrial products are all likely focus sectors for the US IPO market in 2026. If the macro environment and trade policy continue to stabilize, 2026 has the potential to be the best issuance window in years.

The federal government has been extremely active in shaping markets and the behavior of businesses, consumers, and investors. Trade policy is the most high-profile example of intervention, but not the only one.

The administration has also taken a more activist stance toward some industries and technologies, such as AI, including investing government funds directly in certain strategic sectors. From steel to the microchips needed for AI, the administration is seeking to move manufacturing back to the United States and bolster the country’s strategic industrial capabilities. It also is taking shares in some companies that it assists. Intervention is a global trend: Other governments are also being more aggressive in intervening in economies throughout the world, including through sovereign wealth funds and related entities.

We believe the administration’s interventionist tendencies may provide an incentive for speed in M&A. Our view is that the current deal market is akin to that of the mid 2010s when M&A was driven by idiosyncratic factors including tax inversions, media consolidation, and the early days of streaming. The first companies to act on those trends were able to complete their deals. But waiting carried risks: The rising trend waves attracted the attention of regulators, who began shutting down many of those deals.

The federal government is now even more willing to get involved in business and the economy than it has been in decades. Companies that recognize trends early and act quickly face less risk of regulatory rejection than peers who follow the crowd.

M&A volume growth in inauguration years under unified government

Presidential inauguration years often see a notable jump just in deal activity as political uncertainty decreases and, in some cases, new legislation helps stimulate the economy. This past year proved to be an exception, as uncertainty over tariffs and other policies made some dealmakers more cautious.

*Source: PwC Intelligence analysis of data from S&P Capital IQ Copyright © 2025, S&P Global Market Intelligence (and its affiliates, as applicable)* Note: Data annualized as of November 30, 2025

Here’s a closer look at three sectors where M&A activity bears watching in the first half of 2026. Check out our sector special reports for in-depth discussions on these and other sectors.

Deal flow is positioned to rise as strategics realign portfolios around growth priorities, while PE remains an active source of capital. Medtechs that have the ability to deliver durable, above market growth have been increasingly rewarded by investors and M&A activity is expected to intensify around assets that can accelerate growth trajectories.

$92.8B

As industrial manufacturing enters 2026, dealmakers should monitor how sustained policy stability and advancing digital transformation reshape competitive dynamics. If financing conditions remain steady, strategic and private equity buyers may accelerate portfolio realignment and consolidation across automation, electrification, and energy transition markets.

52%

Tech M&A is entering a new phase, defined by the pursuit of AI capabilities and the infrastructure needed to support them. Strategic buyers and PE firms are targeting foundational assets, from data centers and chips to AI-native software and security platforms. Consolidation is accelerating in profitable software verticals, where AI can enhance product differentiation and margins.

31%

Despite several potential challenges, we believe the current M&A uptick rests on solid ground. If trade policy stabilizes, interest rates drop, and AI enthusiasm continues, we expect the market to build on the significant gains it made in 2025. While value growth may stabilize, we expect volume to pick up if macro-economic drivers and renewed confidence help push both middle-market corporates and PE firms back into the M&A arena.

{{item.text}}

{{item.text}}

*S&P Global Market Intelligence Disclaimer Notice

Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact.