{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

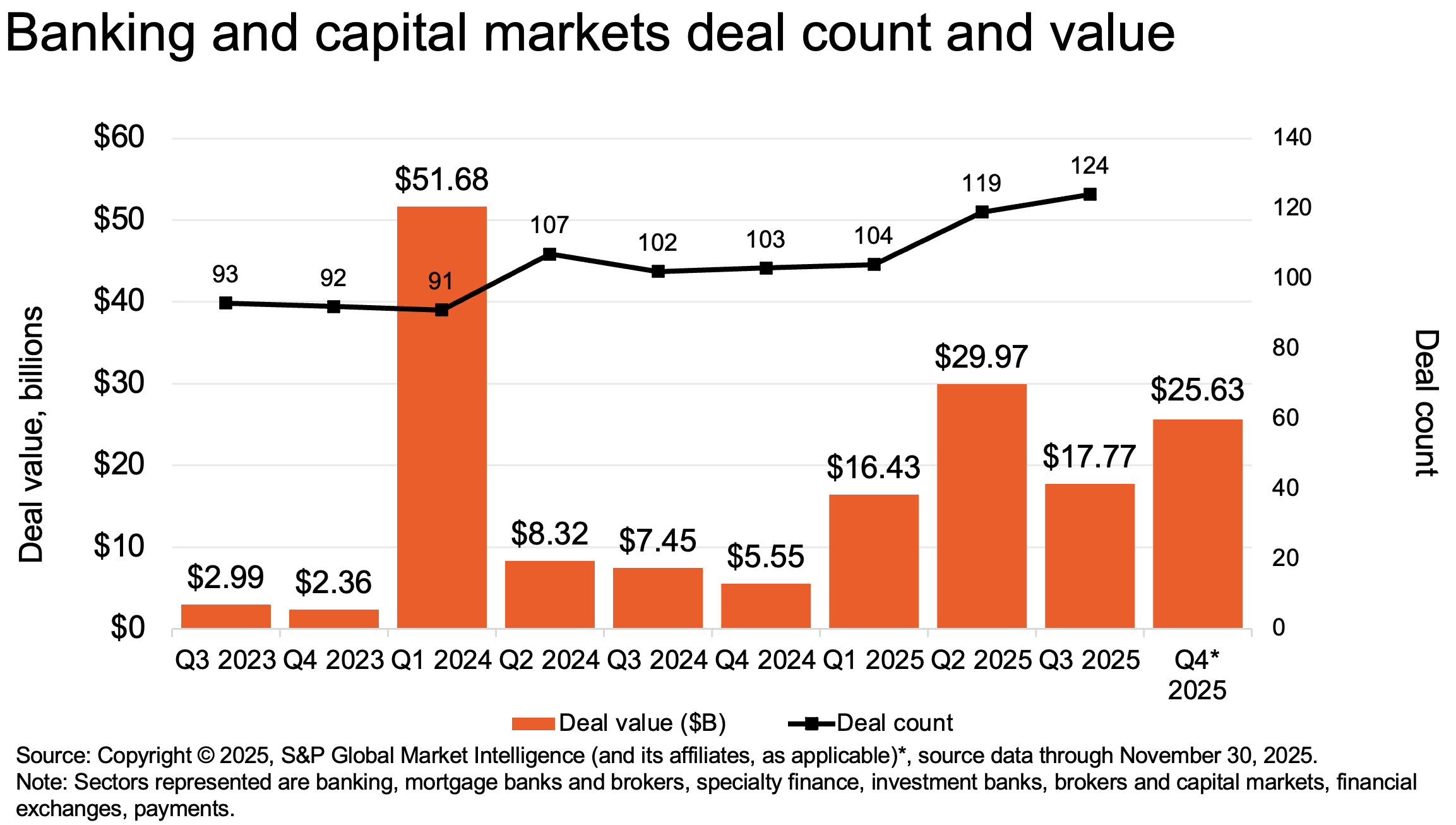

Regional bank dealmaking is on an upward trend in the second half of the year, a wave of activity that we were optimistic about in our deals report at midyear. The desire to increase scale, expand geographic reach, and realize synergies to amplify growth are drivers of the recently announced large bank mergers.

There is, we believe, much more pent-up demand which can fuel greater deal activity. M&A can be an accelerant for change amid the twin pressures to adopt new technologies and operate more efficiently. Those twin forces are the motivating force behind the recent large bank deals that captured the public’s imagination, but make no mistake there is a vibrant undercurrent of activity among smaller institutions facing the same challenges. Also playing a role are changing regulations, yet it is today's shorter deal closing timelines that allow for a more efficient deal life cycle and a higher probability that a deal thesis will be fully executed.

Additionally, we reiterate our expectation that payments and fintech organizations will utilize deals to drive growth and scale. This year’s resurgent IPO market for fintechs could be a leading indicator that the industry will remain at the leading edge of AI powered products and payment capabilities. So far this year, six US fintech IPOs raised about $3.2 billion, the highest level in at least a decade, according to S&P Global Market Intelligence data.

Indicators that support more bank tie-ups are all around us:

Banking fundamentals are healthy with earnings boosted by growing net-interest margins while loan provisions remain stable.

“Synergies plus transformation” is essential. Cost reduction levers (rationalizing branches, reducing overhead) are just one aspect of a deal’s thesis. Now, value comes from tech simplification and core modernization along with greater efficiency.

More interest rate cuts, fewer macroeconomic shocks, and an industry-favorable regulatory climate could provide the clarity that banks need to be even more acquisitive.

We expect buyers to face intense competition in the pursuit of the best assets and growth platforms. They’re putting the most weight on three issues that can determine the success of a future deal:

“Banking deals could dramatically grow in pursuit of transformation. The confluence of lighter regulations, falling interest rates, and powerful technology is profoundly affecting corporate strategy.”

Dan Goerlich,US Banking Deals LeaderIt remains essential for management teams to have a comprehensive playbook for capturing value and growth from transactions. This is especially true ahead of a potentially landmark change in asset-based regulatory categories. The concerns around deposit growth and cost of funds still command center stage. Yet, AI integration is equally important to address. Many institutions see scale as the shortest path to realizing AI's promise. Banking deal activity is likely to remain healthy given the favorable backdrop of a lighter regulatory landscape, a growing economy, and stable profitability.

{{item.text}}

{{item.text}}