A peek inside the pharmaceutical company of the future

Breakthroughs at scale: the future of pharma

Reasons to believe—catalysts driving a new future

Accelerating science: AI-driven drug R&D, synthetic biology, and digital biomarkers are just a few of the here-and-now advances that hold even greater promise in the future. Biopharma venture investment—rebounding sharply to roughly US $26 billion in 2024 after a two-year downtrend2—signals renewed confidence in a new wave of innovation. Advances in molecular biology, computational chemistry, and AI-enabled discovery are collapsing timelines for new medicines and unlocking entirely new therapeutic modalities. Meanwhile, the convergence of data from genomics, real-world evidence, and digital health tools is giving scientists and clinicians unprecedented insight into how diseases begin, progress, and respond to treatment. These breakthroughs are redefining what is possible in medicine and signaling that a new era—defined by precision, prevention, and personalization—is already underway.1

New patient expectations: A new generation of healthcare consumers is taking shape. Patients are no longer passive recipients of care.

They expect faster access to innovation and outcomes seamlessly integrated into daily life. Empowered by data, digital tools, and personalized insights, more and more patients are already putting themselves in command of their healthcare. Extrapolating this trend, patients of the future will demand therapies tailored to their unique biology and behaviors. They will expect real-time feedback on how well treatments are working with customized and holistic recommendations to optimize their care (not just optimize their medicine).

Rapidly expanding role of technology: Technology is already a catalyst for re-defining experiences, expectations, and possibilities. In the future, physicians will likely be AI-native, trained and supported by intelligent systems that inform clinical decisions in real time. Patients, too, can expect AI-enabled, tech-integrated experiences across their health journey, from clinical trials and therapy selection to personalized adherence and wellness programs. In short, technology isn’t just accelerating innovation. It is raising the bar for human experience across each touchpoint of the pharma enterprise and this change is already well underway.

Unsustainable healthcare costs: Another powerful catalyst for change is the growing unsustainability of healthcare costs—now exceeding $5 trillion in the United States and growing 8% annually. Society cannot afford to keep doing the same old things: treating illness late, managing symptoms rather than preventing disease, and accepting waste and inefficiency. This cost pressure is already forcing players in the ecosystem—payers, providers, policymakers, and patients—to demand better value. For pharma, this represents both a challenge and a defining opportunity. The industry will be called upon not just to deliver innovative therapies, but to help break the underlying drivers of high costs—through earlier intervention, precision targeting, digital monitoring, and real-world outcomes that reduce the total burden of disease. In doing so, pharma can help shift healthcare from an expensive system of sickness management to a sustainable model based on prevention and positive patient outcomes.

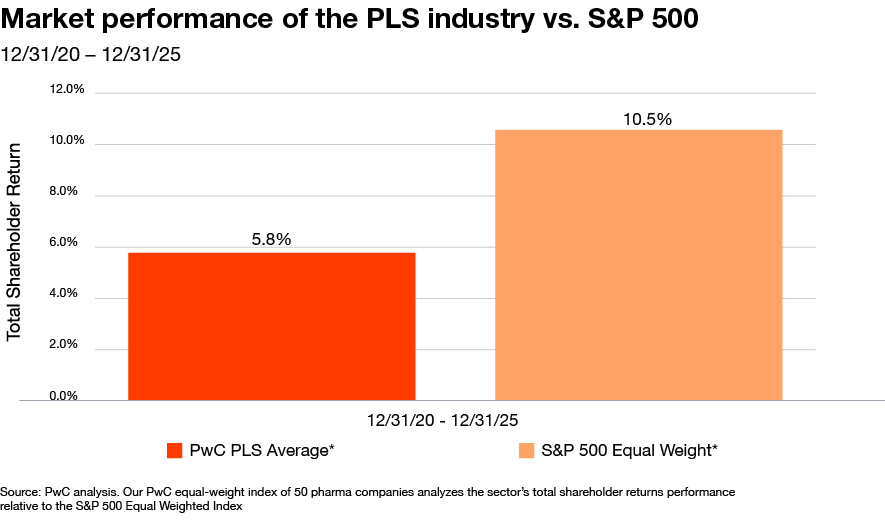

Pharma’s value challenge: Finally, pharma itself faces an urgent need for reinvention. Despite an impressive wave of new drug approvals over the past five years, the sector under-performed in the capital markets over that same period.

Investors are signaling that innovation alone is no longer enough—particularly as many companies pursue similar therapeutic areas, fueling intense head-to-head competition and compressing returns. At the same time, new pricing regimes and tariff policies are adding direct pressure on the P&L. The result is a strained business model where traditional approaches have not delivered the growth and productivity outlook necessary to generate top-tier shareholder returns. To restore investor confidence, pharma will need to redefine where and how it creates value.

Data from Q4 2025 offers a signal for cautious optimism. After years of muted performance and expectations, pharma outperformed the market, suggesting a potential inflection point following a difficult cycle shaped by policy headwinds, patent expirations, and a post-COVID cliff for some companies.

This shift appears to be driven by renewed confidence in a new wave of science, beyond GLP-1s alone, and new strategies for adapting to today’s market realities (e.g., more direct-to-patient engagement, lower cost operating models). While a single quarter does not reverse a multi-year track record, this moment should be viewed as an opening to win-over investors. There is early momentum in both innovative science and innovative business models, powered by advances in precision medicine and AI-enabled discovery that promise to compress development timelines and expand what is biologically possible.

The next decade should reward companies that can combine the rigor of science with the promise of technology, the empathy of consumer industries, and the investment discipline of a rigorous capital manager. In this new era, success will be measured by lives improved, costs avoided, and value created.

Defining the next era of pharma leadership

The pharmaceutical leaders of 2035 could look fundamentally different from those of today. These capabilities separate the winners from the rest.

Harnessing the full power of breakthrough science

Winning companies will operate at the frontier of biology, technology, and data. They will translate advances in genomics, synthetic biology, molecular engineering, and AI-driven discovery into therapies that don’t just manage disease, but cure or prevent it altogether. Their R&D organizations will function as dynamic learning systems, continuously integrating real-world evidence, digital biomarkers, and patient-derived data to accelerate insight and de-risk development. The distinction between “research” and “care” will blur as discovery becomes a continuous, feedback-driven process that adapts in real time to patient outcomes.

Designing novel, lifelong patient experiences

The most successful pharma companies are positioned to redefine what it means to “deliver therapy.” They will move beyond transactional prescriptions to create branded health journeys—providing patients with digital companions, personalized support, and real-time feedback on progress. These companies will understand that the value of a medicine is not just in the molecule, but in the outcomes it enables and the loyalty it creates. By embedding behavioral science, data analytics, and human-centered design, they will build and participate in ecosystems that support patients throughout the life cycle of disease.

Reinventing the enterprise via hyper-intelligent operating models

Behind the scenes, tomorrow’s winning pharma organizations will run on adaptive, AI-enabled operating systems that are faster, leaner, and smarter than anything seen before. They will automate the transactional, augment the analytical, and orchestrate work through intelligent platforms that continuously improve speed, efficiency, effectiveness and risk. End-to-end digital integration—across R&D, manufacturing, commercial, supply chain, and compliance— can dissolve silos and compress cycle times, turning months into weeks and weeks into days. Advanced analytics and decision intelligence can enable resources to flow dynamically to where they create the most value, while automation and generative AI radically reduce the cost to operate. Agentic AI can provide the human workforce with a major productivity boost across each department in the company. These organizations will behave less like traditional hierarchies and more like living networks—self-learning, self-improving, and capable of scaling innovation at the pace of science.

In combination, these capabilities can enable pharma to transcend its traditional role as a maker of medicine and breakout of the capital markets slump that has plagued the sector.

Four strategic imperatives for pharma in 2026

CEOs should be able to point to tangible progress across each of these four imperatives. Together, they form the blueprint for pharma’s next era.

1. Reinvent R&D—redefining what’s curable

In 2026, the most forward-looking pharma companies will begin reinventing how discovery happens—laying the groundwork for an R&D model built for 2035. The old paradigm of linear, insular development could give way to networked innovation ecosystems that blend human ingenuity, artificial intelligence, and global collaboration. In this new model, discovery never stops—it continuously evolves as data, biology, and technology intersect in real time.

The first step is a strategic reorientation of portfolios toward the world’s most urgent and under-treated diseases, areas where breakthroughs can redefine what is curable and restore purpose to the enterprise of science. The “white space” is calling. Winning companies will move beyond incremental improvements in crowded categories and invest boldly in frontier spaces such as reversing organ decline, curing genetic conditions, and extending health lifespan.

To make this possible, organizations should form fluid networks of innovation by linking internal research capabilities with biotech trailblazers, AI discovery platforms, venture incubators, and academic consortia. These living ecosystems can accelerate learning, compress discovery timelines, and dramatically improve R&D productivity. With AI-guided portfolio management and predictive modeling, companies can dynamically rebalance investments in response to emerging science and patient need.

The result becomes an R&D engine that is faster, smarter, and bolder—one designed not merely to compete in existing markets, but to pioneer entirely new frontiers of medicine.

2. Rebuild the enterprise to accelerate the power of AI

The winning pharma companies of 2035 are set to run at the speed of science, enabled by intelligent systems that continuously learn, optimize, and adapt. In 2026, leaders will begin transforming their internal machinery by embedding AI, automation, and digital twins into every layer of the enterprise to accelerate work and reduce costs at scale.

These hyper-intelligent operating models can dissolve silos and connect R&D, manufacturing, commercial, and supply chain into a single, responsive network. Intelligent workflows can orchestrate tasks autonomously, reallocate resources dynamically, and shrink decision cycles from months to minutes. As automation handles the routine and AI augments analysis, people should focus their creativity and expertise where it creates the most value.

Forward-leaning companies can begin now by digitizing their core processes, investing in unified data architectures, and piloting “lights-out” functions that prove the business case for speed and efficiency. Over time, these steps can create operating models that are leaner, faster, and more resilient, matching the pace of discovery with the precision of delivery.

3. Design consumer-driven, lifelong branded experiences

Pharma’s relationship with patients could begin to look more like a partnership and less like a transaction. The most successful companies will design connected health ecosystems that accompany patients across the full spectrum of disease—anticipating needs before diagnosis, supporting them through treatment, and helping sustain long-term health.

Digital platforms, virtual coaching, and predictive analytics can enable personalized, adaptive engagement and deliver the right message, intervention, or support at the right time. Over the next few years, leading organizations can begin building this capability by taking several critical steps.

- Develop direct-to-patient platforms that integrate education, adherence tools, and data-sharing in one seamless interface to transform engagement from one-way communication into a two-way relationship.

- Invest in predictive and behavioral analytics to identify early signals of patient risk or disengagement and trigger proactive outreach.

- Form partnerships with technology and data companies to extend the reach of engagement beyond traditional healthcare channels, embedding pharma into the broader health and wellness ecosystem (e.g., via wearables, biosensors, and other devices).

- Pilot closed-loop engagement models that link real-world outcomes directly to patient support, creating feedback systems where experience continuously informs improvement.

- Redefine success metrics from prescription volume to “patient success”—adherence, satisfaction, and measurable improvement in quality of life.

These actions can lay the groundwork for an era in which engagement is not episodic but continuous, not reactive but predictive. Over time, this shift from “treatment moments” to lifelong health experiences can transform how patients perceive value, how outcomes are achieved, and how trust is earned.

4. Create pharma’s human–AI workforce of the future

In 2026, the line between human intelligence and machine intelligence will blur in productive, empowering ways. Pharma will invest in creating the hybrid workforce of the future, capturing the best of human potential and agentic AI. Job roles, performance metrics, and career paths will be redesigned around adaptability and outcomes. Hybrid teams combining scientific expertise with computational intelligence could accelerate discovery, enhance safety, and personalize patient engagement.

Rather than replacing people, AI elevates them—amplifying human judgment, accelerating learning, and expanding the industry’s capacity to deliver meaningful impact at scale. Companies that start now by mapping future skill needs, creating cross-disciplinary learning programs, and embedding AI tools into everyday workflows can be better positioned to unlock the true potential of human-AI collaboration.

Building the PharmaCo of the future

By the end of 2026, the outlines of the next-generation pharmaceutical company will already be visible. Those that move first—redefining R&D, reimagining patient experience, re-architecting operations—will be in the best position to both outperform their peers and set the stage for tomorrow’s business opportunities.

Winning organizations won’t wait for certainty; they will experiment boldly, scale what works, and hardwire adaptability into their DNA. Investments made today in intelligent platforms, patient partnerships, and a workforce empowered by AI should compound over the next decade.

The opportunity is clear: Act today to design the pharma enterprise of 2035—an organization as intelligent, agile, and human as the future of health itself.

Realizing this vision demands not just new ideas, but new decisions on capital allocation. The traditional funding mix, concentrated in existing therapeutic areas, line extensions and the legacy commercial playbook, should give way to bold rebalancing. Leading companies can redirect investment toward frontier science, emerging therapeutic modalities, and next-generation approaches to discovery. At the same time, they can make larger, longer-term bets on digital engagement and patient experience—treating platforms, data ecosystems, and intelligent interfaces as strategic assets on par with pipelines.

To fund these shifts, many organizations should also rethink their portfolios holistically and assess how to access the capital needed to drive transformative investments. This may mean divesting mature or non-core businesses to free capital for the strategic bets of the future. It may also mean creative arrangements with sources of private capital.

But bold reinvention carries risk. As pharma companies rewire business models and accelerate the pace of innovation, they should embed compliance by design to confirm that governance, data integrity, and patient safety are hard-coded into each process and platform. Intelligent monitoring systems, transparent AI models, and proactive risk analytics can help organizations move fast without compromising trust.

The transformation of pharma will not only be scientific and technological but financial and organizational as well. Companies that align capital and capability with bold vision for transformative role pharma can play will be the ones that define the next era of leadership.

The future of healthcare

Over the next decade, we expect $1 trillion of annual healthcare spending to shift.

Pharmaceutical and life sciences: US Deals 2026 outlook

See where pharma and life sciences M&A is heading in 2026.