{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

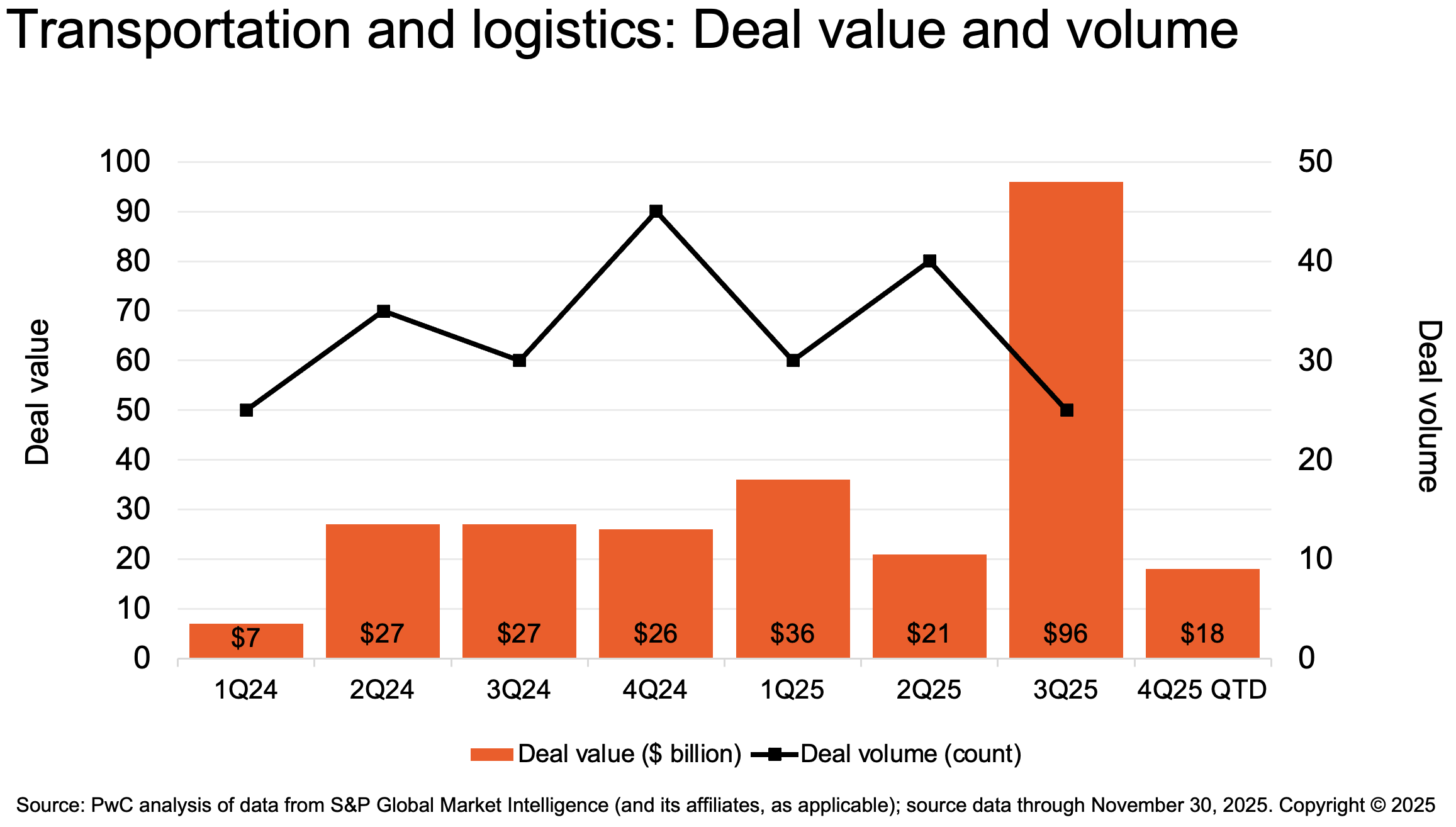

Dealmaking in transportation and logistics (T&L) gained renewed traction in the second half of 2025 as buyers prioritized strategic alignment over scale. Acquirers focused on subsectors offering defensible growth, operating efficiency, and exposure to high-barrier markets. Activity spanned the full value chain—from infrastructure to asset-light platforms—with capital flowing toward technology modernization, resilient supply chains, and specialized logistics services.

What defined dealmaking in late 2025

2026 will bring a series of decision points that could reshape competitive dynamics in the T&L sector. Chief among them is the regulatory outcome of the Union Pacific–Norfolk Southern merger. The Surface Transportation Board’s (STB) ruling may introduce new conditions around pricing, access, and service reliability—and could lead to divestitures of overlapping routes or terminals.

For dealmakers, this means opportunity. Platforms that support rail-adjacent businesses such as track maintenance, railcar services, and transloading operations could see increased demand. Regulatory clarity is also expected to support capital deployment across first-mile, last-mile, and intermodal logistics as providers reposition around network access.

Key developments to watch in transportation and logistics

Rail consolidation outcomes will shape access. The STB’s ruling on the Union Pacific–Norfolk Southern merger will influence how buyers model network access, pricing pressure, and capital deployment. Any required divestitures or service conditions could open new opportunities in track infrastructure, transloading, and short-line partnerships.

Capital costs are easing. Expected interest rate cuts are improving credit access and enabling dealmakers to revive deferred deals. But as capital becomes cheaper, competition for logistics and infrastructure assets may intensify, narrowing valuation spreads and unlocking stalled deals. Sponsors are likely to accelerate exits and recap activity amid a more favorable financing environment.

Trade clarity is supporting strategy. More predictable tariff frameworks and trade policy are boosting confidence in nearshoring, regional integration, and cross-border modeling. Buyers are now more able to assess long-term profitability with fewer geopolitical surprises.

Tech enablement remains a theme. As customer expectations evolve, platforms offering real-time visibility, automation, and network agility will continue to stand out. Digital capabilities are increasingly viewed as core to operational resilience and service differentiation.

Specialized assets remain attractive. Niche categories like pharma logistics, temperature-controlled transport, and reverse logistics align with broader consumption patterns and shifting demographic trends. These areas offer resilient demand profiles and embedded customer relationships.

“The Union Pacific–Norfolk Southern merger is expected to spur 2026 deal activity in rail infrastructure, maintenance, and transloading as investors seek growth in rail-adjacent opportunities.”

Darach Chapman,Transportation & Logistics Deals LeaderM&A activity in 2026 likely won’t be defined by volume. It will be shaped by strategic repositioning, timing, regulatory clarity, and the ability to modernize operations through targeted acquisitions. With a pivot toward quality over quantity, investors are favoring platforms that enable network optimization, automation, and resilience. While regulatory reviews and lingering policy uncertainty may shape deal timing, the fundamentals—including ample dry powder, renewed confidence in financing markets, and accelerating digital integration—all point to a constructive environment for dealmaking across the sector.

{{item.text}}

{{item.text}}