{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

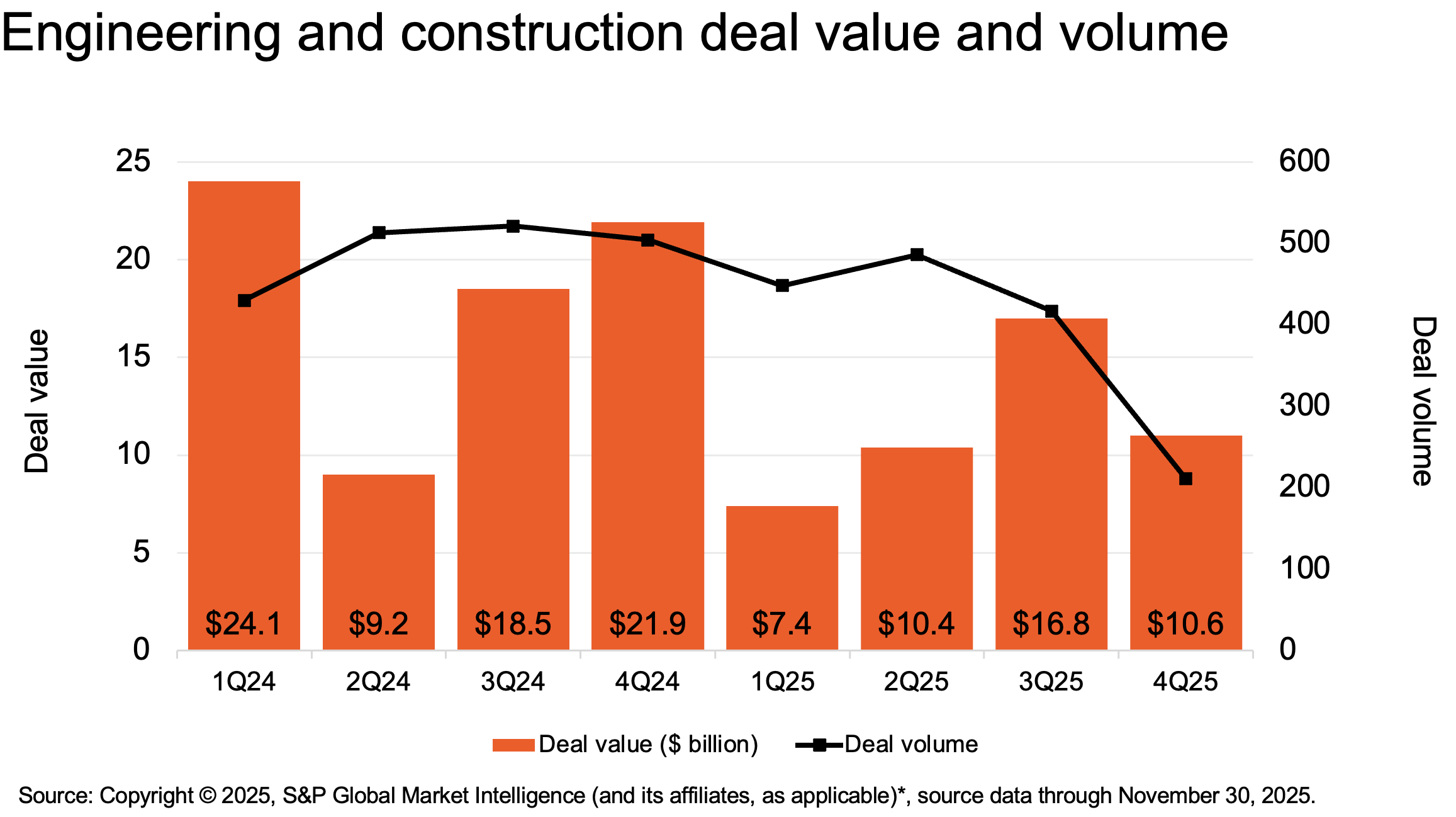

After a cautious first half of 2025, dealmaking in engineering and construction (E&C) regained momentum in the second half, though overall M&A remained below 2024 levels. Large transactions exceeding $1 billion reemerged, lifting cumulative deal value in the third quarter even as deal volume contracted slightly. The pattern reflects a market where confidence is returning at the top end, but investors remain selective amid cost inflation, labor shortages, and uneven access to financing. For many, M&A is becoming less about broad expansion and more about repositioning for policy certainty, supply chain resilience, and productivity gains. Buyers are adapting to shifting U.S. trade and industrial policy by using M&A to strengthen domestic capacity and reduce supply chain risk.

Key developments shaping the second half of 2025:

Together, these trends reveal a market recalibrating around policy stability, cost discipline, and digital acceleration. E&C companies are using M&A not just to withstand volatility, but to modernize operations and capture opportunity in a shifting domestic market.

As these forces continue into 2026, the sector’s near-term M&A outlook will be shaped by how companies build scale, address labor and cost pressures, and adopt technologies that support more efficient and resilient delivery.

In 2026, the E&C sector will continue to balance rising input costs, ongoing labor shortages, and shifting policy dynamics with long-term demand tied to infrastructure investment, advanced manufacturing, and data-center development. These crosscurrents are shaping how investors assess risk and identify opportunities. Two themes are expected to guide M&A activity over the next six months.

Dealmakers who align their strategies with these structural drivers—scale, labor efficiency, technology adoption, and supply chain stability—will be best positioned as the E&C sector moves toward more resilient, digitally integrated, and sustainability-focused models.

“We expect deal activity to tick up as firms use M&A to tackle labor shortages, manage tariffs, and capture growth in data centers and grid modernization.”

Danny Bitar,US Engineering and Construction Deals LeaderE&C dealmaking in 2026 will be shaped by continued consolidation and ongoing technology-driven change. With infrastructure, data center, and energy-transition activity supporting demand, disciplined buyers can use M&A to build scale, improve productivity, and strengthen resilience. As labor constraints, cost pressures, and policy dynamics continue to influence the market, firms that integrate technology, pursue scalable platforms, and enhance supply chain stability will be positioned to lead the next phase of industry transformation.

{{item.text}}

{{item.text}}