{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

As companies continue to undertake large-scale business and technology transformations, either in support of internal operations or to enable cloud enabled technologies, software development has significantly evolved over the past several years. Many organizations now deliver technology through agile, iterative releases, cloud migrations, and continuous deployment – approaches that often blur traditional lines between planning, development, and testing, making traditional stage-based accounting models sometimes difficult to apply in practice.

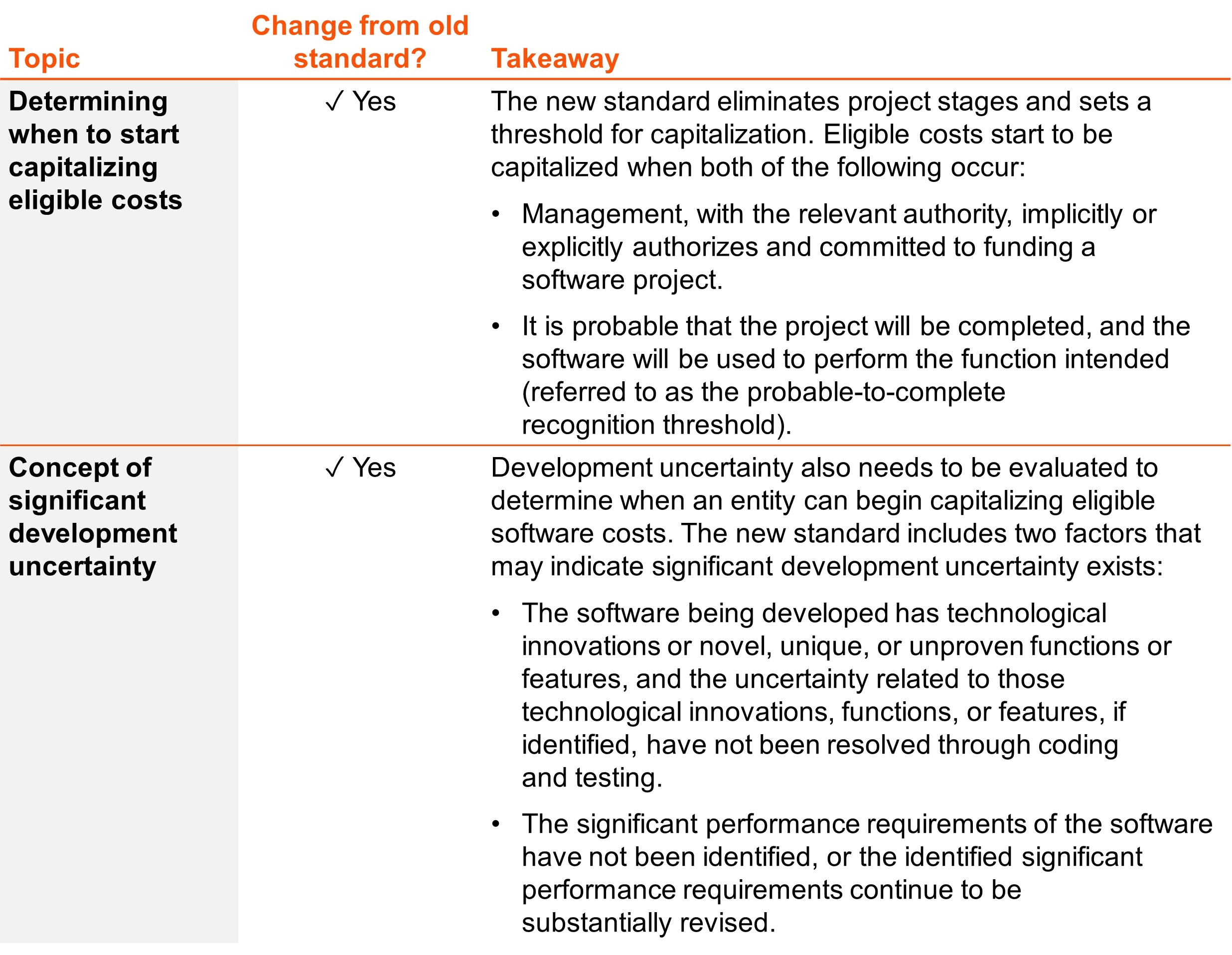

In September 2025, the Financial Accounting Standards Board (FASB) introduced a new accounting standard, ASU 2025-06, set to take effect in 2028 for interim periods of calendar year companies, with the option for early adoption. This update is the FASB’s response to the ever-evolving realities of today’s software development environment and constitutes the most significant update to internal-use software accounting in more than 25 years. The standard modernizes the internal-use software model by replacing the historical project stage framework with a principles-based capitalization threshold that more closely aligns with how modern IT organizations operate. By moving away from project-stage criteria that don’t always necessarily reflect today’s software development realities and instead introducing a new framework grounded in management authorization, funding commitment, and management’s assessment of the probability of project completion, finance teams can better keep pace with ongoing transformation efforts.

While companies will need to navigate some important changes, several key components of today’s internal-use software reporting model remain unchanged. For example, ASU 2025-06 did not impact the following items for internal-use software:

In addition, the new standard does not affect the guidance in ASC 985-20 related to software sold to customers, nor does it affect how companies determine whether a software project is in the scope of ASC 350-40 or ASC 985-20.

The key changes introduced by ASU 2025-06 focus on the timing of when to start capitalizing eligible internal-use software development costs. These updates are highlighted in the table below.

As a reminder, while software capitalization is often associated with technology companies, ASU 2025-06 applies to internal-use software across all industries. From ERP implementations and cloud migrations to analytics platforms and digital customer tools, most organizations develop or customize software for internal operations, making the new guidance relevant regardless of primary business sector.

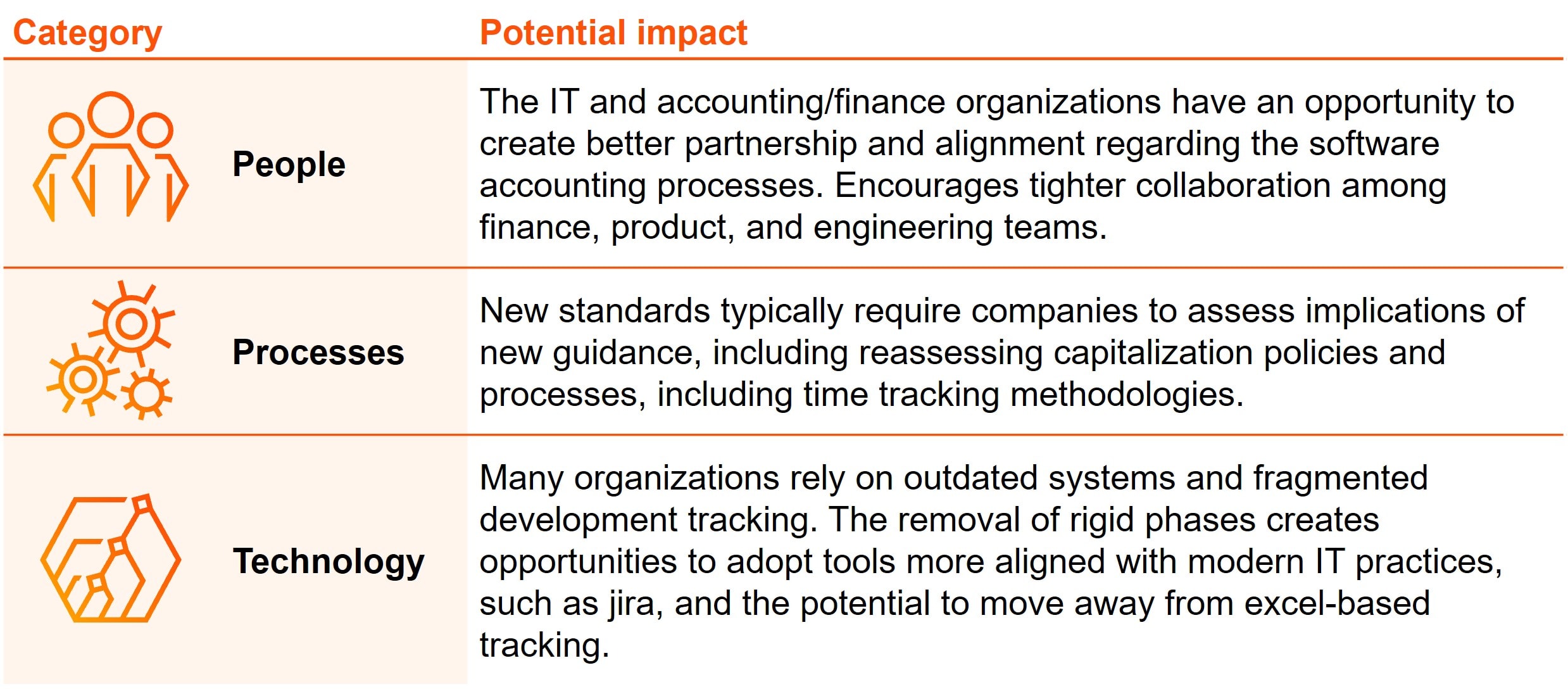

ASU 2025-06 is designed to be more practical in modern delivery environments, but it raises the bar on documentation, governance, and cross-functional alignment – particularly around:

The updated guidance is expected to drive more consistent capitalization conclusions across development methodologies and better align accounting with how technology teams build and deploy software today. As software investment continues to fuel transformation, stakeholders expect transparency and discipline in how these costs are evaluated and reported.

The improvements in ASU 2025-06 do not address how companies should capitalize eligible costs (e.g., detailed time tracking vs a roles-based model). Therefore, regardless of the impact, the new guidance continues to require management teams to exercise significant judgment in applying the model to track and account for the relevant costs, potentially leading to changes in existing policies and processes. For instance, companies with policies and processes centered around stages of development will need to revisit these, resulting in a potential opportunity to better align with how internal IT resources are managed.

Refer to our In-depth and Podcast for more information on the new standard.

Adopting the new standard is much more than a technical accounting change – the application of the new standard may influence reported performance, financing flexibility, and transaction exit readiness, be it an IPO or a sale. The new standard is not optional and applies to all industries. The combination of the new standard and increased IT spending by non-technology companies to digitally enable their businesses has prompted many organizations to review and refresh their existing software capitalization policies, processes and practices now given its impact for key metrics, including a frequently used non-GAAP measure, earnings before interest, taxes, depreciation and amortization (“EBITDA”).

Looking ahead to 2026 and beyond, as discussed in the PwC 2026 US IPO outlook, there is renewed and growing interest in accessing the capital markets, presenting significant opportunities for companies with strong financial profiles. Organizations should strategically consider this evolving capital markets landscape when implementing their software capitalization strategies, as consistently applied financial metrics resulting from a well-defined and consistently applied capitalization framework may enhance their positioning for future funding, refinancing, or exit opportunities and limit the risk of surprises. We have observed instances, particularly in non-technology sectors that invested heavily to tech-enable their business, where not having well established and consistently applied internal-use software capitalization policies has created audit challenges, in some cases delaying IPO processes. Moreover, companies are at risk of missing potential tax benefits when necessary data to perform income tax research and development (“R&D”) credit studies is not available, or not captured in a format that readily allows this work to be completed in a timely and efficient manner.

As the deals market rebounds, the focus on capitalizing software costs is set to intensify. PwC's US Deals 2026 outlook highlights that the next wave of M&A will focus on bigger and bolder deals driven by AI and private equity. This anticipated wave will likely spotlight software capitalization policies and processes of acquisition targets, given the impact of KPIs such as EBITDA on valuations. Additionally, with the growing focus and significance of AI, being able to clearly connect the dots between AI investments and what costs are on the balance sheet will be important.

The application of internal use software guidance has impacts on financial measures under today’s guidance, and these impacts will continue on tomorrow under the new guidance as well. For example, many companies utilize non-GAAP measures such as EBITDA to report results externally. As capitalized costs are recorded and subsequently amortized when expensed, the amortization is excluded from this non-GAAP measure. Other financial measures can also be impacted like debt-to-equity ratios. From an income tax perspective, impacts can be felt as well, since certain software development activities may qualify for R&D tax credits or other tax incentives, subject to applicable tax rules and eligibility requirements.

While the new software accounting guidance provides a helpful framework for assessing how to treat software costs across a variety of technological scenarios, applying it in practice is still expected to be a considerable challenge. Although the terminology and framework for assessing what is capitalizable and when have changed, many companies historically applied varying approaches in this area, in part due to implementation challenges, evolving fact patterns, and interactions with other capitalization guidance (such as ASC 350-40). The updated standards underscore that capitalization of qualifying costs is required under GAAP (subject to materiality).

Investments in emerging technologies, such as Agentic AI or Generative AI, have introduced unique complexities from an accounting and financial reporting perspective. Organizational leaders should champion cross-functional collaboration within their organizations, particularly when capitalizing costs related to software acquisition and development for these emerging technologies.

Key questions for management teams to consider:

Because ASU 2025-06 applies to all entities that develop or obtain software for internal use, virtually any industry undertaking digital or cloud-driven transformation may benefit from reexamining capitalization policies:

PwC is a trusted resource for helping organizations of all sizes navigate the accounting and financial reporting challenges of cloud migration or IT transformation, including through investments in emerging technologies.

Our Cloud Accounting Services specialists can assist with financial reporting questions regarding software costs capitalization, as well as support your organization’s assessment of broader business implications as you invest in the cloud, embrace automation and emerging tech (including AI), and adopt agile methodologies for software development.

Our teams across the broader spectrum of PwC services possess deep experience with analyzing the financial, tax, people, operational, and technological impacts of IT investment, including assisting you in implementation, adoption, and efforts to operationalize your accounting policies.

Our knowledge can help you:

We would like to thank Megan McDonough and Alyman Ouattara for contributing to this article.

{{item.text}}

{{item.text}}