{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

The number of Chapter 11 bankruptcies hit a decade-long high in 2025 and activity is primed to continue into 2026. Several trends that drove a measured uptick in restructuring last year will likely continue in the New Year. These include higher input costs—driven by inflation and trade disruptions—and a K-shaped economy, where spending by lower- and middle-income consumers is increasingly strained.

In our view, these trends combined with the overall growth of the economy are likely to generate another modest increase in bankruptcy filings in 2026. Executives at companies facing financial stress should emphasize scenario planning that helps identify possible problems as early as possible while mapping out potential operating remedies or increasingly popular out-of-court liability management transactions. Being proactive before a potential bankruptcy trigger (debt maturity, breached credit covenant, sustained losses, etc.) gives companies more flexibility and options in how they respond while also limiting the length and costs of an in-court restructuring.

Bankruptcy filings increased for the fourth year in a row in 2025.

Source: © 2026 Octus Intelligence

Chapter 11 bankruptcy filings reached a 10-year high in 2025. While elevated relative to historical levels, filings saw just a modest bump compared to activity levels in recent years. The past three years have included a step change in the level of commercial real estate activity due to relatively higher interest rates and disruptions caused by work-from-home trends. Excluding real estate bankruptcies, which primarily relate to smaller single asset filings, restructuring activity trended slightly higher than in recent years.

Loan defaults, including distressed exchanges, averaged about 4.3% of all issuers, unchanged from 2024 but higher than pre-pandemic averages in the 2–3% range. Out-of-court restructuring has become increasingly popular over the past several years because it can significantly lower restructuring costs.

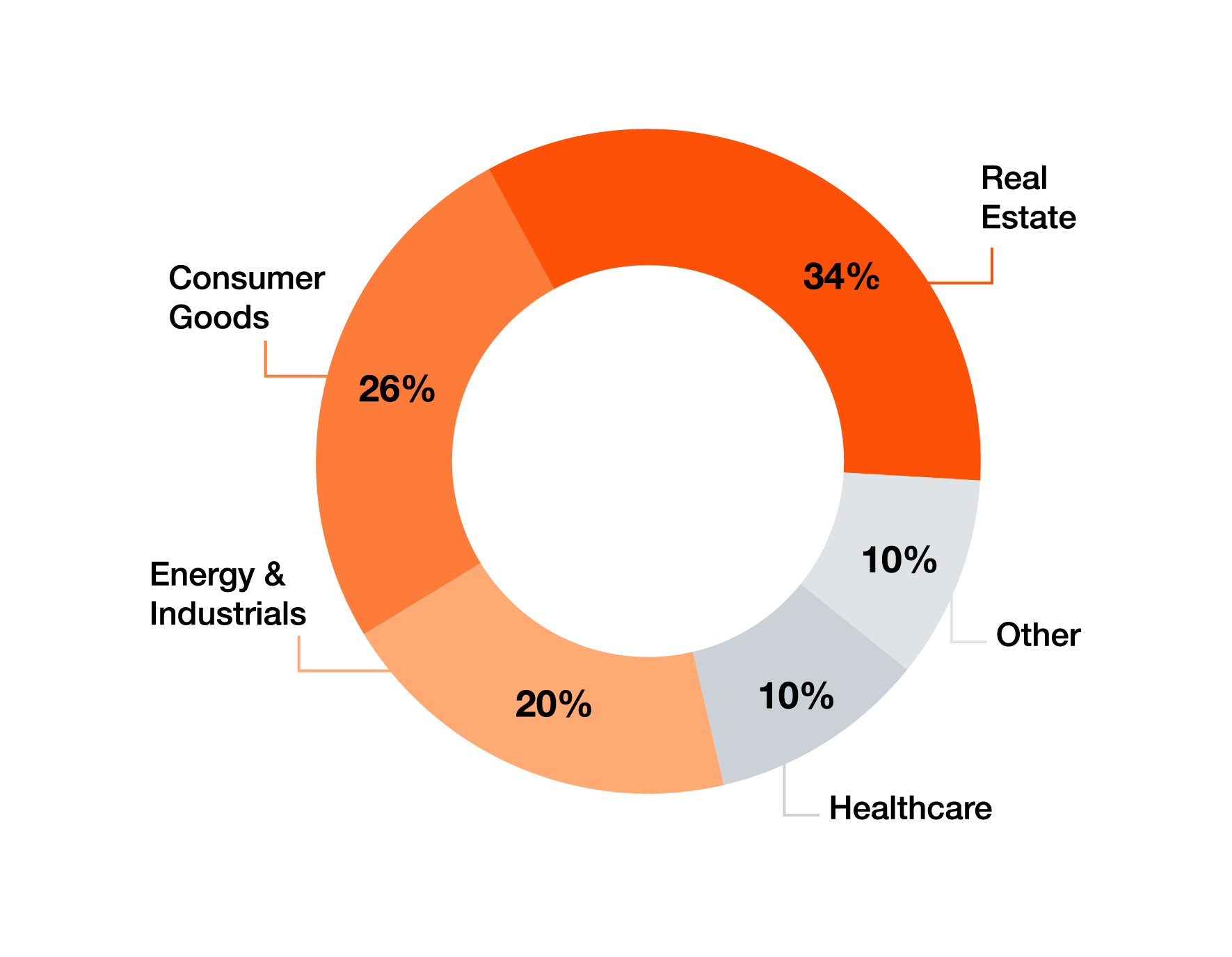

Real estate, consumer goods, and energy/industrial companies dominated 2025 activity, combining for 80% of all Chapter 11 filings. While industry-specific issues played a role, the large number of filings is primarily a result of those sectors’ overall size rather than widespread problems in them.

The real estate, consumer goods and energy/industrial sectors combined for 80% of Chapter 11 filings.

Source: © 2026 Octus Intelligence

The Federal Reserve has adopted a measured easing cycle with policymakers trimming rates to support a softening labor market while keeping an eye on persistent inflation. Despite multiple cuts in 2025, borrowing costs remain relatively high and Fed members have emphasized a meeting-to-meeting approach that limits rate cut forecasts. Continuing this approach could lead to a modest improvement in financing conditions, but it’s unlikely to significantly help overleveraged borrowers whose capital structures were built in a much lower-rate environment.

Borrowers that need more substantial help are increasingly turning to options like liability management exercises (LMEs). These out-of-court restructurings can lower process cost and shorten timelines, but they should also be paired with operational transformation to address business performance challenges. Without addressing underlying operational problems, balance sheet engineering will only delay and complicate a more disruptive restructuring later down the line.

Leadership at companies facing financial stress should keep these mitigation strategies in mind.

Looking ahead, stressed companies should expect economic pressures like inflation, high input costs, and uneven consumer spending to persist. While traditional bankruptcies may increase, many will likely turn to faster, less costly out-of-court financial restructurings. Success depends on early planning, addressing both financial and operational challenges, and engaging promptly with key stakeholders. Key sectors such as consumer markets, healthcare, and automotive face unique hurdles requiring targeted strategies. Ultimately, companies that act early will have more options and better chances to overcome financial stress and emerge stronger.

{{item.text}}

{{item.text}}