Explore the predictions we think will prevail in the global economy in 2022, including our GDP and inflation projections and the impact of COVID-19.

As we usher in the new year, our clients and the wider business community will be refreshing their business plans in the hope that the year ahead is less eventful than the last. To help provide some clarity, in this edition of the Global Economy Watch, PwC takes a look at what 2022 might have in store for the global economy.

At risk of sounding like a broken record, we remind our readers that the new variant of COVID-19, Omicron, introduces a huge level of short-term uncertainty to our outlook. The predictions in this paper, as well as our gross domestic product (GDP) and inflation projections, are based on our assumption that Omicron’s economic impact will be limited and that the current set of booster vaccines, or indeed those that are likely to be introduced at the end of Quarter 1 / beginning of Quarter 2, provide adequate protection against serious illness. We should get more clarity on this in the next few weeks, and it is possible that this assumption does not hold. We therefore also outline the shape of a plausible downside scenario in the Box 1, at the end of this page.

Here, we set out some key themes and predictions for 2022 in our base case scenario.

Chinese economy bigger than the European Union (EU): In our base case scenario, we expect the world economy to grow by around 4.5% next year in market exchange rates, which is significantly above the longer-term average real GDP growth. We expect that the US, China and EU will continue to remain the three largest economic blocks for years to come. There will, however, be some subtle changes within these economies. For example, we expect 2022 will be the first year where the output of the Chinese economy will overtake that of the European Union (EU) and will continue to persist in the medium-term. Focusing on emerging economies, IMF projections show India could become a US$3 trillion economy, reaching a similar level as the combined output of the ASEAN-5 (Indonesia, Malaysia, the Philippines, Singapore and Thailand). The Sub-Saharan African economies are collectively poised to be a US$2 trillion economy.1

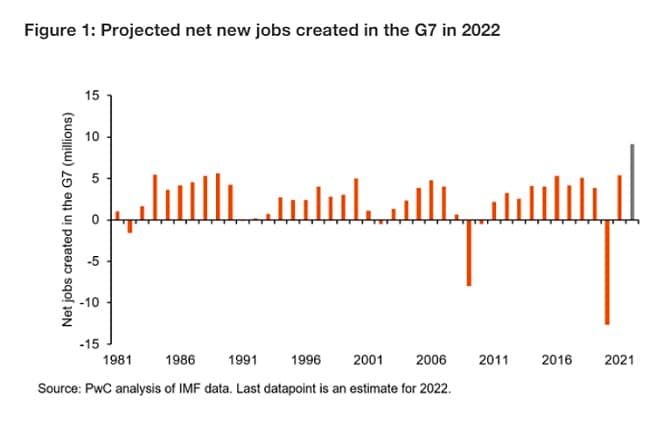

Almost 10 million jobs created in the G7: The Group of Seven (G7) are projected to continue to create jobs at a rapid pace— in our base scenario we estimate these economies could create at least nine million jobs which is the highest figure since at least the 1980s. To set the context, this would mean that a total of 14-15 million jobs will have been created in the G7 two years after extraordinary policy action, such as furlough schemes, was taken to run “high pressure” economies in response to the pandemic (see Figure 1). A closer look at our analysis shows that this picture will be somewhat disjointed as it is only the US and Canada that will have managed to exceed their pre-crisis employment levels. Despite this, we think that a ‘hot’ labour market will mean that employers will continue to experiment with newer, innovative ways to retain existing staff and attract newer ones —we dub this phenomenon as the rise of the ‘flexible employer’.

Predictions for 2022

Rise of the ‘flexible employer’: A hot labour market means that workers will have more bargaining power. We don’t necessarily expect this to translate into sustainably higher nominal wage growth (or indeed a wage-price spiral similar to that experienced in the UK in the 1970s). In fact, adjusting for the effects of the pandemic (compositional issues, distortions from government schemes and base effects) we have seen that the latest nominal wage growth data is more in keeping with historic levels, particularly in the Eurozone and the UK.

What we do expect though is employers to adapt to the high competition for workers experimenting with ways to attract and retain staff by making themselves stand out as ‘flexible employers’. For example, we have begun to see employers offer four day working weeks, hybrid working arrangements, and better non-financial benefits. We expect to see more of these type of trends particularly in the services sector and the knowledge-based sectors.

Economies will enter a monetary policy tightening cycle: We expect tighter financial conditions as central banks in advanced economies hike their policy rates and cut back on their quantitative easing programmes. This process has already started in the US and the UK but effects of the Omicron variant might delay this by a few months. We expect that the Eurozone will continue its accomodative monetary stance as its core inflation rate, excluding changes in indirect taxes, is unlikely to breach its 2% target in 2022.

This won’t spell trouble for most emerging markets. Unlike in 2013, most of the larger emerging economies (Brazil, South Africa etc) have been preparing for “lift off” in the US by raising their central bank rates rates. The exception to this is Turkey, which has decided not to follow the example of other emerging economies, leading to economic turmoil.

Shift from ‘just in time’ to ‘just in case’: We expect supply chain pressures to dissipate. We’ve already seen evidence of this happening in the last few months of 2021 and expect this to continue. By the second half of 2022, this trend will pull down headline inflation via relatively low durable prices. This could give central banks some breathing space to potentially delay future rate hikes particularly if their economies face additional headwinds (due to unexpected epidemiological changes, for example).

The case for developing ‘strategic autonomy’ in a variety of areas ranging from semi-conductors, to artificial intelligence and car battery manufacturing will continue to gather momentum, particularly in the EU which is an open large economy. This will help build resilience in corporates, even though it could have a short-term negative hit on profit margins. Our historic scenario analysis on reshoring some ‘strategic’ sectors of economic activity shows that this could be a US$136 bn to US $272 bn (in 2019 constant prices) opportunity for the G7 countries, but could lead to sub-optimal economic outcomes, particularly if the ‘strategic’ sectors draw up labour from other more productive sectors of the economy.

Reversal of roles between the US and EU in fiscal policy: In the US, for the first time since the beginning of the pandemic, the Hutchins Centre expects fiscal policy to drag economic growth by around 2 percentage points (pp) in 2022.2 This drag could be larger if the Build Back Better programme is delayed or downsized.

Meanwhile in the EU, which is governed by a set of fiscal rules, the story is different as fiscal policy is expected to add between 0.5pp to 1pp to economic growth in 2022. This reversal reflects the suspension of EU fiscal rules until probably 2023 which we expect will be revised to acknowledge the more activist role fiscal authorities will have to play to meet the bloc’s legally binding target of net zero greenhouse gases by 2050.

A third of global electricity could come from renewable sources in 2022 as coal consumption continues to decline: 2022 is likely to be another record breaking year for renewable energy, as falling prices and global momentum from COP26 drive renewable sources to account for over 30% of total electricity generation globally.3

Capacity projections suggest new renewable capacity will increase by 295 gigawatts (GW), the biggest ever for the second year in a row.3 Solar and wind will account for most of this growth, particularly in the US and China. This will facilitate the clean energy transition, following new commitments made at COP26 to phase out coal and end international public support for unabated fossil fuel energy by end 2022.

We expect the discussion on renewables to start to shift to storage and transmission systems, which are a key component of making electricity grids more resilient.

Commodity prices expected to remain steady but geopolitics could derail this: The rapid growth in energy prices, and natural gas in particular, in 2021 is expected to ease over the first half of 2022 based on future prices. However, this assumes no major geopolitical developments, which are a key driver of short-term prices of natural gas, particularly in Europe which has limited energy-related commodities.

1 IMF, World Economic Outlook, October 2021

2 Hutchins CenterFiscal Impact Measure, December 2021

3 International Energy Agency, Renewables 2021

Figure 2: Expected capacity additions by country, 2022

Source: International Energy Agency, PwC analysis

Box 1: A plausible downside scenario for the global economy in 2022

Due to the short-term uncertainty the Omicron variant has introduced, here we outline a potential downside scenario for the global economy

| Base Case | Downside scenario | |

| Epidemiological assumptions |

|

|

| Real GDP growth |

|

|

| Inflation |

|

|

Contact us

Follow us