Overview

The retail banking industry is undergoing tremendous change. A few years ago, it was a fairly straightforward business, but today, technology and innovation, increasing competition, regulatory complexity, embedded finance, consolidation, and evolving customer expectations are placing immense pressure on traditional business models. This intricate and evolving web of trends influences whom consumers trust and how they prefer to conduct their financial lives. It also forces banks to address the fundamental question of what a financial institution is—and what value it provides.

For leadership teams at incumbent retail banks, now is the time to better understand these trends and prepare for a rapidly changing environment. To help, we activated our community of solvers and developed five hypothetical scenarios for how the future of the sector could play out over the next decade.

Though deliberately exaggerated, all five scenarios represent an urgent call to action for retail banks and point specifically to three priority areas where banks should act immediately and proactively to adapt: tech-powered transformation, data-enabled customer focus and broad-based trust.

Our analysis suggests several possibilities for how the next decade could unfold. Now is the time to consider radical future-facing scenarios to prepare to build the capabilities and resilience that will be necessary to thrive in tomorrow’s far more dynamic environment.

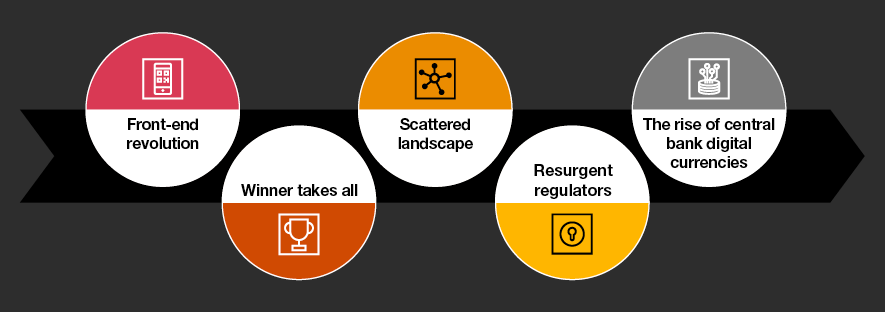

Future shock: Five retail banking scenarios for the next decade

Front-end revolution

New players from outside of traditional finance capture client relationships—the ‘front end’ of banking—and incorporate financial services into their platforms. These companies are established, cash-rich brands in the technology, media and entertainment sectors, capable of creating an improved user experience and hyper-personalised offerings to aggressively control more of the customer relationship.

Established banks—generally facing higher regulatory burdens and dealing with outdated technology—compete as the infrastructure backbone of the financial system. They act as utility providers that offer licenced services and products, but no longer have a customer-facing brand.

Winner takes all

A wave of consolidation results in a few mega banks and fintech companies ruling the banking landscape. These massive, tech-enabled institutions generate a competitive advantage through scale.

Customers gravitate towards the largest, most personalised and convenient platforms and generally have no concerns about data privacy or the ability to choose. Only the largest banks will be able to make the technological investments necessary to create a differentiated customer experience.

Scattered landscape

Amid deteriorating societal trust, customers grow doubtful of global institutions. The supervisory regime favours smaller and local banks, and sentiment gravitates towards nationalistic protection. Clients and assets flow from global players to more locally focused banks with smaller balance sheets, deposits, and lending facilities, and to specialised micro-niche players.

Resurgent regulators

Regulators take an active approach to a wave of Big Tech and other non-traditional entrants to ensure a safe and strong financial system. Government antitrust actions push technology players out of the industry and increase barriers to entry; competition comes solely from firms that hold full financial services licences.

This degree of regulation opens the door for banks to rebuild trust and reclaim their role as the central provider of financial products and services.

The rise of central bank digital currencies

A steady decrease in the use of cash continues alongside the rollout of central bank digital currencies (CBDCs). Digital currencies gain wide acceptance in B2B, B2C and C2C segments.

Incumbent banks lose the basic bank account—which, like customer data, is an anchor of customer relationships that they have long controlled—to central banks. This makes traditional bank business models unviable.

Adaptive ways to think about your business

The industry changes that are already underway hold major implications for all players but particularly for incumbent banks, which must double down on priorities that have long been important but that have proved elusive for many. These priorities—tech-powered transformation, data-enabled customer focus and broad-based trust—are becoming increasingly urgent. Regardless of how the future unfolds, one thing is certain: the result will be a radically different competitive environment than today’s. Retail banking leaders have no time to lose.

Contact us

Global Financial Services Advisory Leader, PwC Netherlands

Tel: +31 6 30 60 43 00

Kurtis Babczenko

Global Banking and Capital Markets Leader, and US Finance Transformation Leader, PwC United States