The insurance industry is growing rapidly in Asia Pacific's developing markets. A significant unifying factor in this diverse region is the adoption of IFRS 17, a globally standardised accounting model for all insurance contracts.

IFRS 17 fundamentally changes the way in which insurers measure contracts, with far reaching effects on a range of business functions. A strategic and carefully considered approach to IFRS 17 implementation will help insurers to identify, improve and even transform ineffective and inefficient systems and business processes.

The aim of this survey is to gain an understanding of how insurers operating in Asia Pacific are conducting their IFRS 17 programmes. The responses provide insights into approaches followed, progress made and challenges faced by those tasked with implementing IFRS 17 for their organisations.

We surveyed 68 insurance executives across 11 countries in the Asia Pacific region. The survey was conducted in May 2020.

How finance leaders are tackling IFRS 17

The majority of respondents see IFRS 17 as an opportunity to enhance their data capabilities, improve their technology and transform their finance function. Only 16% of insurance executives say that they are working towards a minimum viable product, i.e. building a solution that will meet the minimum requirements of IFRS 17.

The approaches do vary by country. We noted that 90% of Korean insurers indicated that they see IFRS 17 as an opportunity to effect full finance transformation, whereas 55% of Singaporean respondents indicated that they are following a foundational approach, i.e. minimum viable product with a wider focus on enhancing their data estate.

Takeaways

The reporting requirements of IFRS 17 severely impact many functions within an insurance organisation, including data requirements, systems, processes, actuarial modelling, finance systems and processes. Many of these impacts only come to light as insurers start designing their IFRS 17 solutions.

The added complexity of IFRS 17 reporting can add significantly to reporting timelines if manual interventions are used to plug gaps. Finance leaders have to think carefully about their strategic goals, to ensure that they develop an IFRS 17 solution that doesn’t put undue reporting strain on their actuarial and finance teams.

What approach are you taking to achieve IFRS 17 compliance?

May 21, 2020: base of 68

Key findings

Focus on finance transformation

More than half of insurance executives see IFRS 17 as a catalyst for finance transformation. The effective date delay gives insurers more time to optimise their business intelligence and reporting capabilities.

COVID-19 is impacting project timelines

53% of respondents say that IFRS 17 project timelines may be delayed due to COVID-19 related business disruption. At least half of the insurers surveyed will intensify their digital transformation programmes to build operational resilience.

IFRS 17 implementation is a long and challenging journey

44% of respondents have not started with detailed design activities. These respondents are particularly worried about time, budget and skill constraints and technical challenges they will face.

Project timeline and progress

Insurance executives say that they expect their IFRS 17 programmes to take them nearly three and a half years to complete, on average. The duration varies significantly between respondents, with more than 25% of respondents indicating that the duration will be five years or longer. The programme duration estimates were consistent across life and non-life insurers. Composites and reinsurers expect their programmes to take a few months longer.

Respondents believe, on average, that it will take an additional two and a half years after IFRS 17 implementation for their organisation to fully stabilise and return to business as usual.

We see significant variability in the progress made on IFRS 17 programmes. 10% of respondents say that they have not kicked off their IFRS 17 programmes, and a total of 44% have not started with detailed design. However, 10% of respondents have already started with parallel runs.

Takeaways

The estimated duration of IFRS 17 programmes shows how complex and challenging IFRS 17 implementation can be for life insurers, non-life insurers and reinsurers.

The effective date of IFRS 17 has been deferred by another year to 1 Jan 2023 in most countries, which gives insurers approximately 30 months to complete their programmes. Insurers that have not started with detailed design of their IFRS 17 solutions should take note of the time and effort required to design and implement the standard.

What is the expected duration of your end-to-end IFRS 17 programme? (months)

How far have you progressed through your IFRS 17 programme?

Impact of effective date delay on IFRS 17 programme

The vast majority of insurers are in favour of the IFRS 17 effective date delay, which would indicate that most insurers believed that they needed additional time to execute their current strategies.

However, only 34% of respondents plan to change their IFRS 17 implementation programme in light of the effective date delay. Of the insurers that indicated that they will change their programmes, 42% indicated that they will slow down IFRS 17 activities and 35% indicated that they will spend more time on data and system enhancements. Only 19% indicated that they will change their IFRS 17 strategy to extract more strategic value.

Only 33% of respondents believe that full implementation of IFRS 17, including data, systems, processes and controls changes will be completed by 1 Jan 2023. Of insurers that have reached the construct and test or parallel run phase, only 44% believe that IFRS 17 will be implemented fully by the effective date.

Takeaways

The IASB’s decision to delay the IFRS 17 effective date to 1 Jan 2023 is welcomed by insurance executives, regardless of how far they have progressed through their IFRS 17 programmes.

Insurers that have not started on their IFRS 17 journeys should not see the delay in the effective date as an opportunity to delay their IFRS 17 programmes further, but rather as an opportunity to execute a strong IFRS 17 implementation strategy, to avoid excessive manual work-around when IFRS 17 reporting goes live.

Insurers that have made good progress with their IFRS 17 strategies see the effective date delay as an opportunity to spend more time on data and system enhancements, to ensure that they have a rigid and efficient IFRS 17 solution in place.

Are you in favour of the IFRS 17 effective date delay?

Will you reconsider your IFRS 17 implementation programme in light of the effective date delay?

How confident are you that your organisations implementation of IFRS 17 will be ready by the effective date (01/01/2023)?

May 21, 2020: base of 68

May 21, 2020: base of 68

Pushing ahead despite of COVID-19

28% of respondents say that they expect a revision to their IFRS 17 strategy due to the effects of COVID-19 on their business. To a sizeable group of respondents (22%), it is unclear whether their strategy will be revised, as they monitor the development of the pandemic and its potential impacts on their business.

Insurance executes do expect delays to their IFRS 17 programmes due to COVID-19 business disruption. 15% of respondents expect significant delays. The majority of respondents believe that their IFRS 17 programme budgets will not be affected by COVID-19 impacts on their business, but 16% do believe that budgets will be cut.

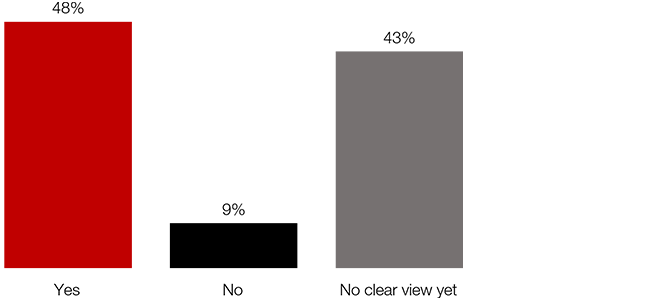

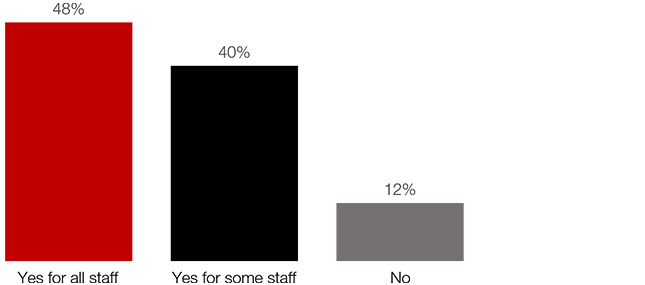

More than half of respondents (52%) say that their programme is affected, as they don’t have the remote working technology in place for all of their staff to perform their IFRS 17-related activities. Many insurance executives are increasing their focus on digital transformation and/or cloud computing as a result of the impacts of COVID-19 related business disruption. About half of respondents do not have a clear view yet of how their organisation will react.

Takeaways

Insurance executives are facing a variety of immediate financial and operational challenges as a direct result of government mandated economic lockdowns. Finance leaders have to balance necessary cost cutting efforts with digital transformation initiatives, to strengthen the resilience of their business.

The general response from insurance executives indicates that IFRS 17 strategy and budgets are not affected, but that the implementation of IFRS 17 may take more time due to business disruption. Insurers that have implemented the necessary technology to allow their workforce to work remotely are able to continue with their IFRS 17 programmes without much disruption. Insurers that don’t have the technology in place are increasing their focus on digital transformation to limit disruption to their business.

Do you expect the COVID-19 pandemic to have a detrimental impact on your IFRS 17 project timelines?

May 21, 2020: base of 68

Do you expect your organisation to increase its focus on digital transformation and/or cloud computing to mitigate IFRS 17 project risk and wider business disruption risk?

Do you have the necessary technology infrastructure in place to enable your staff to continue their IFRS 17-related activities?

May 21, 2020: base of 68

May 21, 2020: base of 68

How much finance leaders are spending on IFRS 17

35% of insurance executives say that they plan to spend less than USD 5m on their IFRS 17 implementation programme. Budgeted spending, as one would expect, closely links to the size of the organisation. For insurers with annual gross written premium (from Asia Pacific operations) in excess of USD 1bn, about half say that they budgeted to spend more than USD 25m.

41% of respondents say that their actual spend is in line with their budgeted spend. 13% say that their actual spend is significantly higher than their budgeted spend.

Takeaways

The implementation of IFRS 17 comes at a significant cost to most insurers, as it affects core systems, data management, actuarial processes, finance systems and reporting. The break-down of costs between these elements will depend on the implementation approach followed by each insurer. In turn, the approach followed by each insurer is informed by their current operational challenges, and their medium to long-term operational and finance strategies.

Typically, outside help in the form of accounting, actuarial and IT consultants and system vendors are required to design and execute the IFRS 17 programme.

How much have you budgeted to spend on your end-to-end IFRS 17 implementation programme?

May 21, 2020: base of 68

How do your actual costs compare to your initial IFRS 17 budget?

May 21, 2020: base of 68

IT approach - to enhance, to build or to buy

Many elements of insurers’ system architecture are affected by IFRS 17. The majority of respondents say that they will enhance their existing core systems to meet the requirements of IFRS 17. Only 6% of respondents will buy new core systems as a direct result of IFRS 17.

44% of respondents are building new data mart capabilities to cope with the significant increase in data required for IFRS 17 reporting, whereas 31% are relying on enhancements to data marts that are already in place.

29% of respondents are looking to vendors for sub ledger solutions (for example, to set and release CSM). This is also the area where many vendors have placed their focus, as such solutions can generally be integrated easily into insurers’ current system architecture.

In terms of reporting and consolidation tools, more than 20% of insurers say that they have not yet decided on the IT approach they will follow.

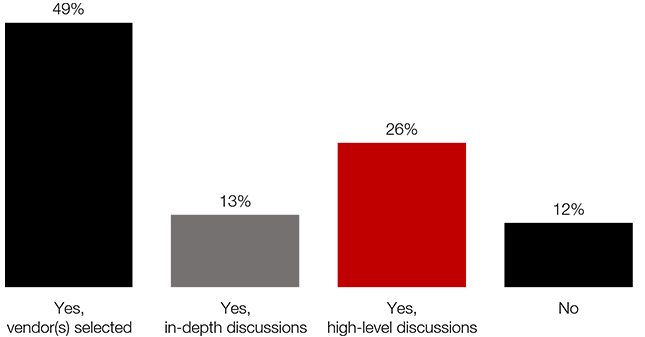

Most respondents have engaged with vendors to understand their IFRS 17 software solutions. Half of respondents have already selected their vendor(s), and another 13% say that they are in in-depth discussions with shortlisted vendors.

Takeaways

In general, we find that life insurers are more likely to build or buy new systems than non-life insurers. For example, 41% of life insurers say that they will build or buy new core systems, compared to 9% of non-life insurers. This discrepancy could relate to the option to non-life insurers to apply the simplified PAA approach to measure their contracts. 54% of non-life insurers believe that all of their business will be PAA eligible, and an additional 14% do not have a clear view yet. We do expect some insurers to reassess their IT approach as they form a better understanding of their data and system requirements.

It is encouraging to see that most respondents have started discussions with vendors. 25% of respondents did however say that they don’t believe software vendors are ready to deploy their IFRS 17 software, and a further 32% said that they don’t have a clear view of whether vendors are ready. Many vendors are gathering additional requirements and releasing updates to their software as they work through the implementation process with their clients. We would expect vendors to release full-capability versions of their software in the coming months, as the requirements of the standard stabilise and industry consensus on best practice is reached.

What is your IT approach to the following systems?

Have you engaged with software vendors to gain an understanding of their IFRS 17 software solutions?

May 21, 2020: base of 68

May 21, 2020: base of 68

Accounting policy, data and technology challenges

Respondents say that they find most aspects of their IFRS 17 programmes reasonably challenging. The biggest challenges relate to setting actuarial modelling methodology (69 out of 100), data constraints (67 out of 100), skill/talent constraints (67 out of 100) and setting accounting policy (66 out of 100).

Insurers that have not started with their IFRS 17 programmes indicated more severe challenges than insurers that have made good progress. Specifically, they expect the most severe challenges to arise from skill/talent constraints (89 out of 100), budget constraints (87 out of 100), and setting actuarial modelling methodology (84 out of 100).

When we look at challenges relating to accounting policy and estimates, respondents find the topics of transition, reinsurance, CSM and risk adjustment the most challenging. Non-life insurers say that they find accounting for reinsurance more challenging than life insurers (76 vs 58 out of 100). Reinsurers say that estimation of cashflows are particularly challenging (74 out of 100).

Takeaways

Insurance executives face many challenges in their IFRS 17 programmes, ranging from time, budget and skill constraints to technical questions around accounting policy and actuarial methodology.

Insurers find it difficult to hire and retain accounting, actuarial and IT resources with IFRS 17-specific skills. External skills are also scarce, as consulting firms experience high demand for their skilled and experienced consultants.

Finance leaders are aware that their accounting policies and actuarial assumptions and estimates can have a significant impact on their financial reporting and KPIs. Insurers often have to make these decisions (and build the necessary data and technology solutions for these requirements) without the luxury of market consensus and industry best practice.

This uncertainty may be one of the reasons why many insurers have not started on the detailed design of their IFRS 17 solutions. The standard has however stabilised, and market practice is becoming clearer. Insurers should therefore push forward with their IFRS programmes to ensure IFRS 17 readiness by the effective date.

How challenging do you find the following aspects of your IFRS 17 programme?

(0 = not challenging; 100 = extremely challenging)

May 21, 2020: base of 68

How much difficulty are you experiencing in setting accounting policy and/or estimates with regard to the following?

(top 4 selected; 0 = not challenging; 100 = extremely challenging)

May 21, 2020: base of 68

Workforce readiness for IFRS 17

44% of respondents have or plan to increase their headcount as a result of IFRS 17 implementation, while 27% say that they don’t have a clear view of staffing requirements yet.

Insurance executives believe that their staff have an intermediate (66%) or limited (32%) understanding of IFRS 17. For insurers that have not reached the design phase, 62% of respondents indicated that their staff’s understanding of IFRS 17 is limited.

Respondents plan to upskill their staff through a combination of formal and informal, on-the-job training.

Takeaways

IFRS 17 is a complex standard which impacts many insurance business functions. The impact of the standard on the day-to-day reporting activities of finance and actuarial teams are generally well understood, and these teams is generally involved in the IFRS 17 programmes from the start.

Insurers do however have to consider the wider impacts of the standard on their business and their people. IT and data teams need to understand the new data requirements and processes required to produce IFRS 17-compliant reports. Sales, marketing and underwriting teams need to understand how business processes and KPIs may change (75% of respondents indicated that they have not started work on identifying and specifying IFRS 17 KPIs). The executive team has to consider how they prepare their workforce for IFRS 17, while considering how their reporting and messaging to the market will change in an IFRS 17 world.

Insurers need to combine multiple avenues of training to prepare their workforce for successful IFRS 17 implementation and business as usual reporting.

Have you or are you planning to increase your headcount as a direct consequence of implementing IFRS 17?

How would you rate your staff's understanding of the IFRS 17 standard and its impact on your business?

How is your organisation planning to improve operational IFRS 17 capability? Select all options that apply.

May 21, 2020: base of 68

May 21, 2020: base of 68

May 21, 2020: base of 68

About the survey

PwC surveyed 68 insurance executives across 11 countries in the Asia Pacific region between May 11 to 18, 2020. Responses were received from a range of small, medium and large life insurers (35%), non-life insurers (37%), composites (18%), reinsurers (7%) and other entities (3%). 37% of the respondents are PwC audit clients. Sign up if you would like us to contact you personally to discuss the survey results, and how we can assist you with your IFRS 17 or related finance transformation programme.