{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

At PwC we believe that a family office’s main purpose is that of supporting the strategy and legacy of your family, and ultimately provide peace of mind that all is being taken care of in a professional, systematic and efficient way.

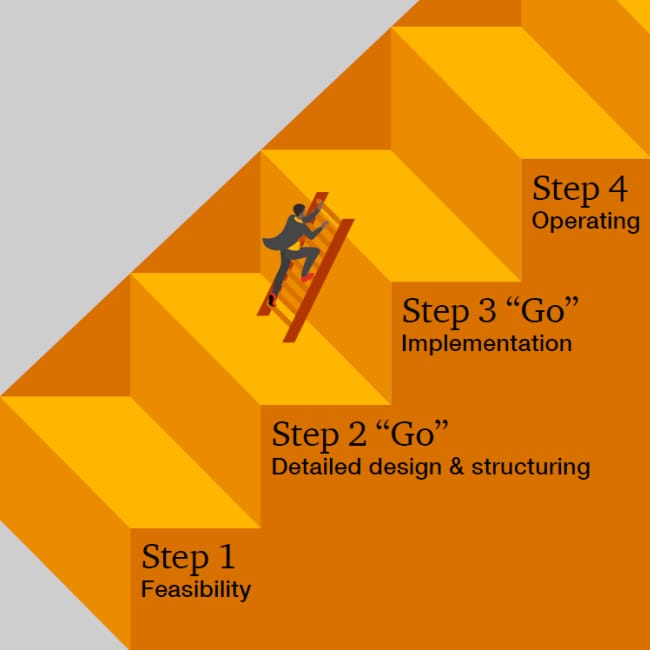

Creating a successful family office requires strategic planning and design. With decades of experience, we can prepare you for each step of the way –from assessment and visioning to work plans and implementation. However, the sheer thought of setting up a family office could be a daunting one but it doesn’t need to be. This 4 steps guide to build your family office will provide you with a comprehensive yet easy to navigate methodology that breaks down the process for an easier understanding. It is aimed at building your confidence in undertaking the process and our global network of experts are at hand to help you build it.

Start with a vision

Setting up a family office starts with defining your vision and purpose for your family and its wealth. Once we understand the purpose and needs of the family, we’ll help you build the foundations of a family office and design to ensure all components work together seamlessly. We conduct an extensive review through research and interviews with select family members to understand your past, current and future vision. These details will guide an overall plan that encompasses key areas, including operations, technology, staffing needs, advisers and governance that is truly built around you. This process will best serve your needs and make certain that your family office is future-ready and shock resilient.

Step 1 key activities

Capturing and understanding of the structure of the family, objectives, ambitions, strategy

Analysing succession goals

Assessing access to funds

Technology enablement options

Establishing governance needs

Drafting talent and staffing profiles

Tax efficiency & CRS profiling

Asset protection

Asset & wealth management

Assessing reporting and compliance needs

Conducting interviews with family advisor(s) and close circle counterparts

Costs analysis

‘Go’ or ‘no go’ business case decision meeting

Step 1 outcome

After this extensive initial assessment you will be in the position to decide if setting up a family office is the right step for you and your family. You’ll have the confidence to know your next steps and priority actions, as well as the type of structure is best suited for your family office and the costs associated.

Now that you have made the informed decision to set up your family office, it is time for design. Now you will have the clarity to envision the necessary structures to fulfill your purpose and vision, as well as protecting and growing your legacy.

Step 2 key activities

Designing legal and tax structures

Planning for Governance

Allocating funding and cost

Design core services (in-house and outsourced)

Addressing operations and technology needs

Defining staffing requirements

Budgeting

Establishing reporting requirements an

Design process flows

Ensure proper controls are in place

Identifying technology needs

select and contract vendors and support

Identify facilities

Design communication and reporting protocols

Write job descriptions

Structure reporting processes

Step 2 outcome

At the end of this important step you will have a clear and detailed roadmap towards implementation. This step will also include further jurisdictional and legal analysis as well as additional transparency of your costs and the timeline.

Now, armed with a robust overall plan, you are ready to set up your family office. This step will include the implementation of all activities, from setting up policies and procedures, legal structures, hiring staff, refining financial models to the actual office set up, including IT infrastructure and cybersecurity.

Step 3 key activities

Hire staff

Set up policies and procedures

Test systems and processes

Assess disaster/business continuity preparedness

Refine financial models

Plan communication protocols

Consider and prepare for cyber threats

Technology launch

Phased launch of services

Continued monitoring and review

Refine reporting processes

Strategic planning

Step 3 outcome

At the end of this step, you will have a fully functioning and compliant family office. All of your key service agreements will be in place with outsource providers and robust legal, digital and reporting structures. We will also put special emphasis on communication among family stakeholders and office staff. This will ensure that your initial vision, values and ambitions are clearly embedded in the decision-making process.

Now that your family office is up and running it is important that it’s functions, processes and governance are reviewed regularly against leading practice and, most importantly, your objectives. It is also time to invest in further refining and building some of the functions and your digital capabilities. This is also the time to further refine your approach to your philanthropic activities and impact investing.

Step 4 key activities

Review of compliance process and outcomes

Review and monitoring of tax and legal requirements

Ensure optimal functioning and benchmarking against leading practices

Further develop digital capabilities

Review of cybersecurity protocols

Assess results with original family goals

Ensure communication effectiveness

ESG alignment

Additional services consideration

Step 4 outcome

This last step concludes the process of setting up your family office and ensures it is built on a solid foundation. Your family office will be agile and future-ready. It will also be an opportunity to include additional solutions for tasks that may have been discovered during implementation or newly changed circumstances. This step is not the end of the road. We will be available to assess future new family office changes and to provide the latest best practices.

Based on the cumulative experiences of some of our most seasoned family office experts, here are some of the most common challenges and mistakes we have identified. We believe that in addition to our 4 steps guide succes, it is important to share the top risks and challenges that you may encounter during the process.

Too much, too fast

A lack of focus on the core mission and key priorities for the office may cause a family to implement everything at once. This could lead to rushed decisions and a disjointed approach to structuring and implementation.

Lack of structural flexibility

When defining the vision and goals for your family office, it is important to think both in near term and long-term objectives. The decisions you make today and tomorrow to nurture your family office and support future generations will prepare you for longevity and evolution. Looking to the future will provide you the ability to evolve family and external objectives, including technology, market, and regulatory changes.

The family office is not treated as a business

All too often, families do not take the step of “operationalizing” the family office. With well documented policies and procedures, you will limit the risk for errors and financial losses. Also, establishing specific KPIs will provide the family insight to how the office is performing relative to its original goals and objectives.

Inadequate focus on data security and other risk management protocols

In the past, families often assumed that their privacy was protected if the office did not carry the name of the family or publicly discuss their affiliation. That has changed. Today, the family and the family office should take the time to develop and implement policies around information protection that include sensitive, private, and confidential data handling. Paying close attention to cyber security, social media, and systems access and security are a must.

Inadequate communication and transparency with family clients

Often, the decision to start a family office rests with one, or just a few family members. As a result, decision making and communications may be highly centralized and not socialized with the broader family. Lack of wide communications will make it difficult for the office to build rapport and trust with family members. Using clear communication with the family will ensure longevity of the family office, and its ability to grow the family legacy.

Casual hiring practices

Key drivers for establishing a family office are the need for confidentiality, privacy and centralizing the “business of family” with a team of trusted staff. However, some offices do not perform even basic background or reference checks on new staff. Lack of formalized job descriptions and performance reviews can be another challenge. Creating well defined hiring processes and staff performance management practices will be critical for a professional office.

Hesitancy to leverage advisor relationships

Families often silo their advisors by aligning them to specific topics or decisions and not leveraging their expertise and awareness of leading practice in other areas. They may also isolate advisors from one another, not allowing direct communication between their selected advisors. While separation is necessary in some cases, encouraging your advisors to work as a collaborative team can often result in the best thinking and implementation for families.

{{item.text}}

{{item.text}}