A PwC and Mergermarket study of 600 global senior corporate executives has found that only 61%* of buyers believe their last acquisition created value. However, acquirers that prioritise value creation from the onset of the deal outperform their industry benchmark by 14% on average 24 months after completion, while divestors that prioritise value creation can outperform industry peers by 6% for the same period.

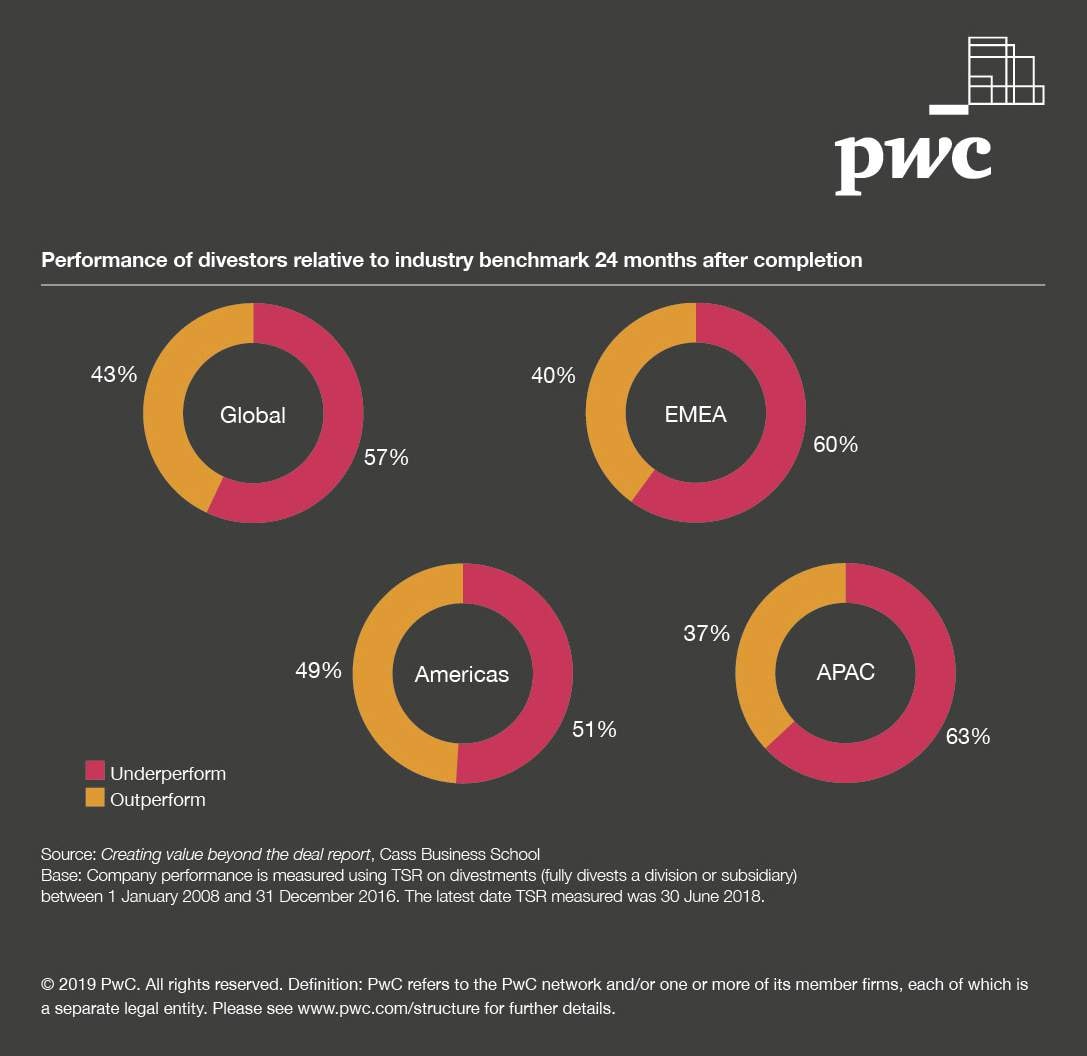

Although value creation strategies are becoming vital to long-term success, the study shows that 53% of acquirers are underperforming their industry peers, on average, over the 24 months following completion of their last deal based on total shareholder return (TSR). Similarly, 57% of divestors are underperforming their industry peers, on average, over the 24 months following completion of their last deal based on TSR.

Despite these figures indicating that many deals fail to realise the value that they intended to generate, those deals that prioritise value creation can generate a significant amount of value. So what exactly are the factors responsible for creating value in deals?

The Creating value beyond the deal report explores how corporations – both on the buyer and seller side - approach value creation throughout a deal. Using industry data, interviews with senior corporate executives, and academic support from the Cass Business School, the research team analysed eight years of transaction data to determine what made them so successful.

Malcolm Lloyd, Global Deals Leader, PwC comments: “As dealmakers are coming under increasing pressure to deliver more value from their M&A activity, companies that establish rigorous criteria for value creation early on in the buying or selling process are best positioned to maximise the returns from the transaction.”

Three main considerations emerged from the research:

- Stay true to the strategic intent: Organisations should approach deals as part of a clear strategic vision and align deal activity to the long-term objectives for the business. 86% of buyers surveyed who say their latest acquisition created significant value also say it was part of a broader portfolio review rather than opportunistic.

- Be clear on all the elements of a comprehensive value creation plan – it should be a blueprint, not a checklist. Ensure a thorough and effective process for conducting the deal with the necessary diligence and rigour in the value creation planning process across all areas of the business. Consider how each of these support the business model, synergy delivery, operating model and technology plans. For acquisitions with significant value lost relative to purchase price: 79% didn’t have an integration strategy in place at signing, 70% didn’t have a synergy plan in place at signing, and 63% didn’t have a technology plan in place at signing.

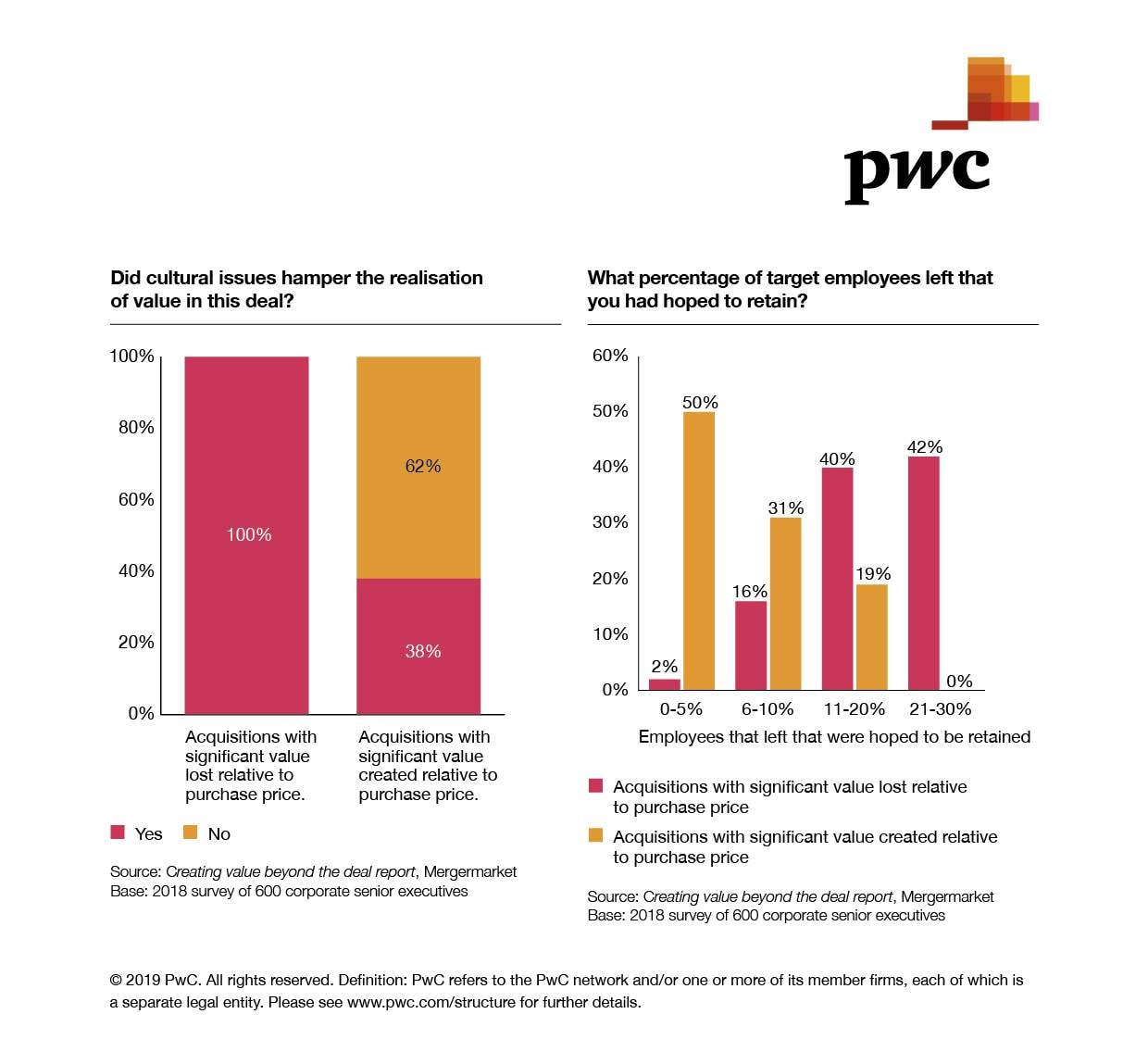

- Put culture at the heart of the deal: Talent management and human capital affect how businesses are able to deliver value pre- and post-deal. 82% of companies who say significant value was destroyed in their latest acquisition lost more than 10% of employees following the transaction.

The conversations with corporate executives show that companies that genuinely prioritise value creation early on – rather than assume it will happen as a natural consequence of the actions they take as the transaction proceeds – have a better track record of maximising value in a deal.

"It was interesting to see that only 34% of acquirers say value creation was a priority on Day One (deal closing) in their latest deal, though 66% said it should have been a priority,” says Malcolm Lloyd. “This highlights the need to continually evaluate and refine the way value creation is approached within organisations.”

John West, Managing Editor, EMEA, Mergermarket, comments: “This fascinating research shows just how often value is left on the table following M&A – and how frequently dealmakers don’t even realise it. Drafting value creation plans cannot just be a box to tick to get the deal over the line. There needs to be execution post-close.”

Dr Valeriya Vitkova, Cass Business School, comments: “Too often in the past phrases like ‘strategic fit’ and ‘cultural match’ have dominated justifications given for acquisitions, without any ‘hard’ evidence provided for these claims. The analysis presented in this report provides excellent insights into what really matters in deals and perhaps as importantly, what doesn’t matter.”

You can download the report on www.pwc.com/deals-report

Ends.

Notes for the editors.

- The report – Creating value beyond the deal: What if you took a different perspective to your M&A? - can be accessed via: www.pwc.com/deals-report

- There are two main components of the survey findings: a public company perspective (both buyer and seller sides) and a private equity (PE) perspective. The private equity perspective will launch at a later date in 2019.

- The report, with support from Mergermarket and Cass Business School, analyses industry data for the top global deals from 8 years of transaction data and includes interviews of 600 Global senior corporate executives, 100 Global PE Executives, and over 30 PwC Deals Leaders.

- Acquisitions are defined as change-of-control transactions where the company buys control of another company.

- Divestments are defined as change-of-control transactions where the company fully divests a division or subsidiary.

- Across both acquisitions and divestments, Total Shareholder Return is calculated over the period from one month prior to announcement to 12 months post completion. The research team required firms to have valid return data 12 months after deal completion so as to be able to calculate the Total Shareholder Return.

- The following restrictions were applied to construct the final sample of transactions: deals are completed; company market value as of the month prior to deal announcement is at least €100 million; and transaction value is at least €50 million and a minimum of 10% ration of transaction size to MV.

- Please visit www.pwc.com/deals-report for more information.

*This was obtained by asking 600 global corporate executives “How much value has this deal created for the underlying business relative to the purchase price?”

- Significant value lost relative to purchase price: 7%

- Moderate value lost relative to purchase price: 17%

- Little/no value created relative to purchase price: 15%

- Moderate value created relative to purchase price: 40%

- Significant value created relative to purchase price: 21%

About PwC

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 152 countries with over 327,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

© 2019 PwC. All rights reserved. Definition: PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

Media

Images

Creating Value Beyond the Deal report cover

Industry benchmarks for divestors by geographic region - Creative Value Beyond the Deal report

Talent retention and culture - Creating Value Beyond the Deal report