Global Economy Watch - Projections

Economic projections

Our economic projections table summarises our main scenario GDP and inflation projections.

November 2025

| Share of 2023 world GDP | GDP growth | Inflation | ||||||

|---|---|---|---|---|---|---|---|---|

| PPP | MER | 2025p | 2026p | 2027 - 2029p |

2025p | 2026p | 2027 - 2029p |

|

| Global (Market Exchange Rate ("MER")) | 100% | 2.6 | 2.5 | 2.6 | 2.7 | 2.5 | 2.4 | |

| Global (Purchasing Power Parity ("PPP") rate) | 100% | 3.1 | 2.9 | 3.0 | 2.7 | 2.5 | 2.4 | |

| G7 | 29.7% | 43.8% | 1.5 | 1.6 | 1.8 | 2.7 | 2.3 | 2.1 |

| E7 | 38.0% | 29.0% | 4.3 | 4.0 | 3.9 | 2.6 | 2.6 | 2.7 |

| United States | 15.0% | 25.5% | 1.9 | 2.0 | 2.2 | 2.9 | 2.6 | 2.2 |

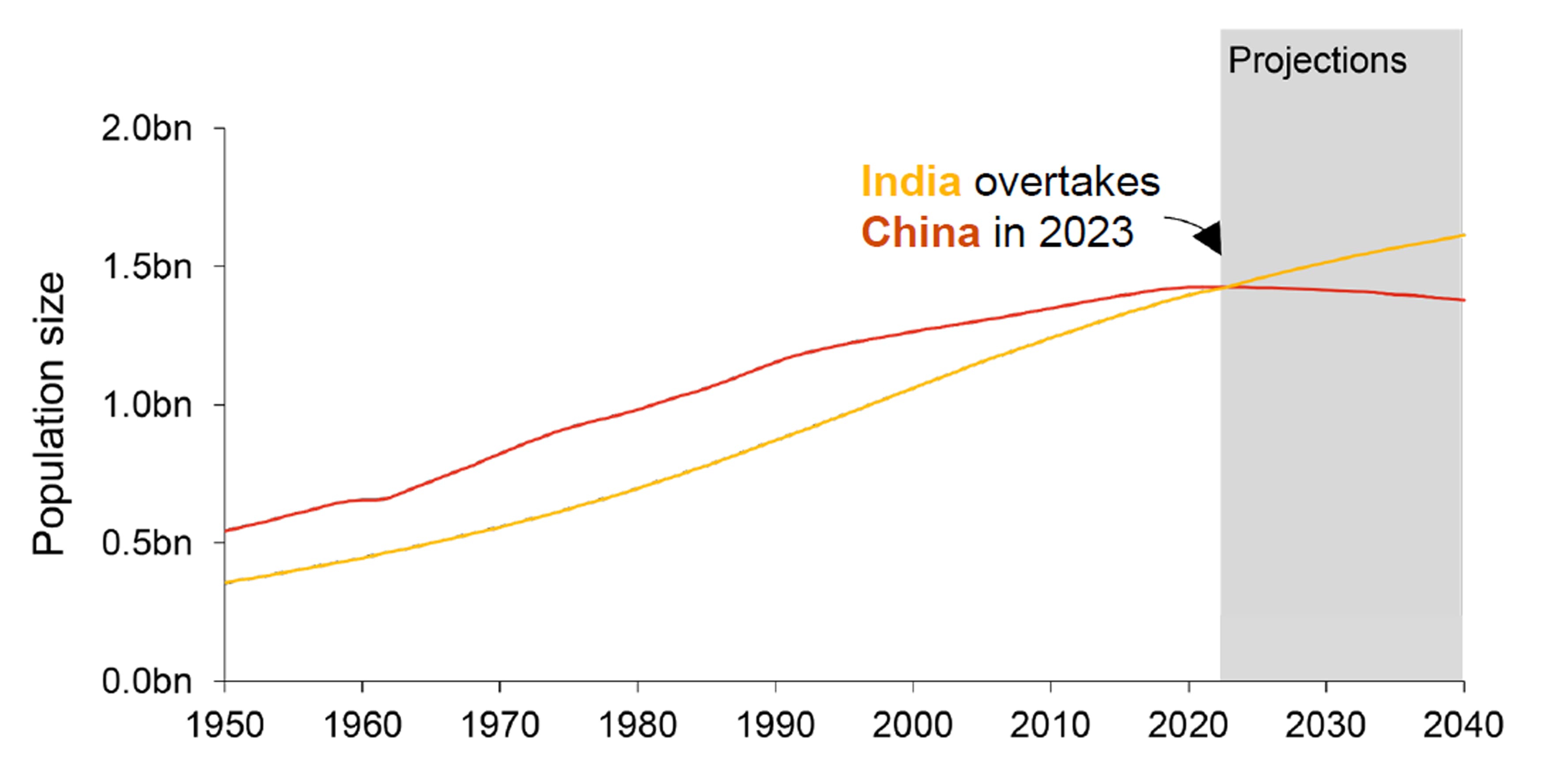

| China | 18.8% | 18.0% | 4.9 | 4.4 | 3.8 | 0.0 | 0.6 | 1.2 |

| Japan | 3.5% | 4.2% | 1.1 | 0.6 | 0.6 | 3.1 | 2.1 | 1.8 |

| United Kingdom | 2.3% | 3.1% | 1.4 | 1.2 | 1.8 | 3.4 | 2.5 | 2.0 |

| Eurozone | 10.6% | 12.3% | 1.4 | 1.2 | 1.4 | 2.0 | 1.9 | 2.0 |

| Germany | 3.3% | 4.1% | 0.2 | 1.1 | 1.5 | 2.2 | 1.9 | 2.0 |

| France | 2.3% | 2.7% | 0.8 | 0.9 | 1.3 | 1.2 | 1.6 | 1.9 |

| Italy | 1.9% | 2.1% | 0.5 | 0.8 | 0.9 | 1.6 | 1.9 | 2.0 |

| Spain | 1.4% | 1.4% | 2.9 | 2.1 | 1.7 | 2.5 | 2.1 | 2.1 |

| Netherlands | 0.8% | 1.0% | 1.5 | 1.1 | 1.4 | 3.0 | 2.3 | 2.0 |

| Ireland | 0.4% | 0.5% | 11.6 | 1.8 | 2.4 | 1.8 | 1.8 | 1.8 |

| Portugal | 0.3% | 0.3% | 1.9 | 2.2 | 2.3 | 2.2 | 2.0 | 2.0 |

| Greece | 0.2% | 0.2% | 2.0 | 2.1 | 1.8 | 2.4 | 2.2 | 2.2 |

| Poland | 1.0% | 0.7% | 3.3 | 3.2 | 3.1 | 3.9 | 2.9 | 2.6 |

| Russia | 3.5% | 2.3% | 0.8 | 1.0 | 1.7 | 8.1 | 5.5 | 4.6 |

| Türkiye | 1.7% | 0.9% | 3.4 | 3.3 | 3.2 | 35 | 25 | 22 |

| Australia | 1.0% | 1.7% | 1.6 | 2.1 | 2.4 | 2.6 | 3.0 | 2.4 |

| India | 7.6% | 3.3% | 6.6 | 6.2 | 6.7 | 2.4 | 4.0 | 4.0 |

| Indonesia | 2.3% | 1.3% | 4.9 | 5.0 | 5.0 | 1.9 | 2.8 | 2.6 |

| South Korea | 1.7% | 1.8% | 0.9 | 1.6 | 1.7 | 2.0 | 1.9 | 1.9 |

| Brazil | 2.4% | 1.9% | 2.2 | 1.6 | 2.5 | 5.0 | 3.9 | 3.2 |

| Canada | 1.4% | 2.1% | 1.2 | 1.4 | 1.8 | 2.0 | 2.1 | 2.0 |

| Mexico | 1.7% | 1.4% | 0.7 | 1.4 | 2.6 | 3.8 | 3.6 | 3.3 |

| South Africa | 0.5% | 0.4% | 1.1 | 1.4 | 1.7 | 3.3 | 3.6 | 3.1 |

| Nigeria | 0.8% | 0.5% | 3.8 | 4.1 | 4.2 | 22 | 19 | 13 |

| Saudi Arabia | 1.1% | 1.1% | 4.3 | 4.3 | 3.7 | 2.1 | 2.1 | 2.2 |

e: Estimate, p: Projection

Sources: PwC UK and global analysis, national statistical authorities, EIKON from Refinitiv, IMF, Consensus Economics, the OECD, and Fitch Solutions. Our projections are a weighted average of projections from these sources. They also incorporate inputs from select teams across the PwC network. ‘MER’ refers to market exchange rates and ‘PPP’ is purchasing power parity. All inflation projections refer to the Consumer Price Index (CPI) unless otherwise stated.

The table above form our main scenario projections and are therefore subject to considerable uncertainties. These projections do not consider the recent changes to the international trading system announced on and subsequent to 2nd April, 2025. PwC recommends that our clients look at a range of alternative scenarios particularly for economies where there may be a high degree of volatility and uncertainty.

| Current Rate (Last Change) | Expectation | Next meeting | |

| Federal Reserve | 4.00% - 4.25% (May 2025) | At least one more cut expected in the next 6 months | December 9-10 |

| European Central Bank | 2.00% (June 2025) | At least one more cut expected in the next 6 months | December 17-18 |

| Bank of England | 4.00% (August 2025) | At least one more cut expected in the next 6 months | December 18 |

Contact us

Contact us