Emerging Trends in Real Estate® Europe is a joint survey by PwC and the Urban Land Institute. Now in its 17th edition the survey provides an outlook on real estate throughout Europe for 2020 and the near-term.

Emerging Trends in Real Estate®: Europe 2020

Climate of change

Survey respondents remain resolute in their belief in real estate as an attractive investment asset class despite strong political and economic headwinds, according to the Emerging Trends in Real Estate, Europe 2020 survey.

Despite political uncertainty and rising construction costs, PwC still foresees an active European real estate market in 2020. Investors are drawing a significant amount of comfort from the central banks’ decision to maintain or cut interest rates – a notable change in direction from last year’s report and probably the biggest factor supporting the general levels of optimism that emerged from this years interviews.

With interest rates set to stay lower for longer and bond yields in many European countries in negative territory, PwC assesses that real estate income will retain its broad appeal to investors. Equity and debt are also expected to remain plentiful for most real estate sectors, the notable exception likely being retail which is still struggling in the face of online competition.

With a number of real estate sectors undergoing significant structural change, many interviewees regard investing in housing and hotels as a sound, defensive strategy at this point in the cycle, supported by long-term urbanisation and demographic trends.

As the Emerging Trends Europe survey has highlighted over the past few years, these sectors are at the forefront of the industry’s transformation into becoming a service industry. There is a recognition that the industry sector that funds, builds and operates the spaces in which we live, work and play, is starting to embrace complexity and respond to its role as part of society’s infrastructure.

Survey results suggest the industry believes that the enhanced complexity and operational risk that comes from embracing the ultimate end-user and their evolving demands is one worth taking to achieve target returns. The latest survey and interviews suggest a blurring of sector boundaries as part of a bigger investment picture in which mixed-use assets, improved transport connectivity, greater use of technology and smart mobility solutions are all seen as integral to the economic growth of Europe’s cities and the investment potential of its real estate.

Key findings

Many survey respondents believe returns – as well as market liquidity – can improve if they take account of the bigger urbanisation and demographic trends and attempt to invest through the cycle.

To that end, the boundaries between traditional and alternative real estate are being blurred. The significance of alternative real estate is not simply the capital it attracts but the way it has helped advance the idea of property as a service, and turn practitioners into. At the same time a blurring of the boundaries between real estate and real assets – especially transport infrastructure – is encouraging investors to examine more closely how their buildings will be used and how cities may develop.

For many of the industry leaders canvassed for Emerging Trends Europe, the opportunities extend beyond large-scale public infrastructure. Many respondents believe that they need to factor in the harder-to-define solutions and cultural changes that are already “transforming urban mobility”. They also acknowledge that, further out, long-term investment needs to reflect the adoption of electric and autonomous vehicles.

There is also an expectation amongst respondents that smart mobility, like big ticket infrastructure, can be a catalyst for urban regeneration.

More than two thirds of survey respondents – a higher proportion than last year – cite increasing construction costs as having the biggest impact on their business in 2020. Interviewees across Europe point to labour and material costs combining for 5-7 percent inflation per annum in this sector.

This is a dilemma for investors, who can see that the post-financial crisis over-supply has disappeared, much stock needs modernising and sourcing suitable standing core assets is as expensive as ever. With constraints on the development pipeline, however, there is little sign of a new oversupply emerging.

A lack of affordable housing has been highlighted by Emerging Trends Europe as a serious problem in many European cities for years, and there is no end in sight. 61 percent of survey respondents are concerned about housing affordability in 2020 – up from last year – and half of respondents believe the problem will worsen over the next five years.

With the supply/demand imbalance acknowledged as long-term, the industry has responded by deploying increasing amounts of capital into various forms of rental housing.

Berlin, for example, has introduced a rent freeze for five years, which has already hit sentiment.

Though much more wary of the regulatory pitfalls than before, experienced residential investors still inherently believe the long-term supply/ demand dynamics make housing relatively secure and a solid investment.

Climate change is seen by respondents as having the biggest impact on real estate over the next 30 years, but it is clear that some industry leaders are already rising to the challenge.

Almost half of survey respondents say climate change has become a greater risk within their portfolio, and 73 percent expect that risk to become greater over the next five years.

Interviews suggest the growing public outcry over the effects of climate change is influencing sentiment in the industry. Public pressure is translating into a general tightening of environmental, social and corporate governance requirements among institutional investors.

Nearly two thirds of survey respondents have increased the use of technology in their operational businesses over the past year. Nearly 90 percent indicate it will likely carry on trending upwards over the next five years.

The survey reveals two main ways respondents are harnessing technology – a third of respondents are buying products from third party suppliers, while a quarter are investing or partnering with startup proptech firms.

Two thirds of respondents may be technology users, but they are not actually investing in technology despite the perceived improvements it can bring to real estate. Some believe their scale of operation is too small to warrant investment. Others are put off by the confusing array of proptech start-ups out there.

Political Risk

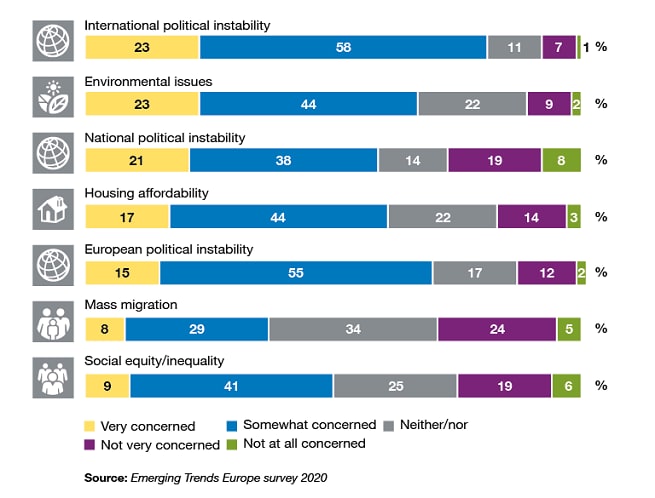

When it comes to social/political issues in 2020, international and European political instability are rated key concerns by 81 percent and 70 percent of survey respondents respectively. Nearly 60 percent are concerned about national politics – a sharp rise from last year.

The political backdrop to investment has been on the minds of Europe’s property leaders for years. The difference now is that political issues are acting as a drag on economic and real estate performance as well as business confidence.

Public policy on housing shortages across Europe is one such example. Industry concerns over housing affordability are rising, but the interviews also reveal widespread frustration at state and local authorities imposing rent controls as a way of dealing with housing affordability. In the eyes of many interviewees this is counter-productive, adding political risk to residential investment while not adding more housing which is mostly needed.

Interest rate boost

Some of the political and economic uncertainty clouding European real estate has been offset for some survey respondents by central banks’ move to maintain or cut base rates – a big boost for investment, albeit not yet for the underlying economy. “It is hard to express strongly enough what an extraordinary turnaround that has been. The cycle feels like it is going to go longer. Nothing seems to be overheating,” says a global investment manager.

Nearly three quarters of respondents expect short-term interest rates to stay the same or reduce in 2020, while the majority believe inflation will hold steady. In the eyes of most interviewees this monetary environment has reinforced real estate’s attraction relative to bonds and equities. As one private equity player says, “There’s not a significant enough slowdown in growth to really undermine the fundamental value proposition that real estate provides, given a negative interest rate environment.”

Leading logistics

The other side of the investment strategy is industrial / logistics, which continues to be of high interest for both investment and development reasons, driven by the continuing increase in online retail sales. There is still seen to be lots of room for growth in European e-commerce, where online sales penetration is lower than the UK, but catching up.

For last-mile logistics in particular, supply cannot keep up with demand, because in urban locations the sector is competing with other high-value uses, such as residential. Some investors think that pricing for existing industrial assets is too high. But few are avoiding the sector altogether. Instead, they are looking to build: industrial and logistics offer the best prospects for development, according to respondents.

But just as residential and industrial / logistics retain their consistently high Emerging Trends Europe rankings, retail remains at the bottom of the rankings in terms of both investment and development prospects.

Getting smart about mobility

Well-connected buildings and places have always been the most valuable, but as the mobility revolution takes hold, owners will have to think smartly about how their assets provide the best and most desired outcomes for the community – whether that be workers, residents, tourists and passers-by.

This is an emerging trend for the real estate industry, and one that will require a change of mindset to factor in the growing complexity of transport solutions into investment decision making.

These mobility trends have the potential to change which buildings and districts are seen as most valuable by real estate investors and developers. It is also likely to reinforce the attraction of mixed-use development, while challenging established principles around urban planning models.

| 2020 | 2019 | |

| 1 | Paris | Lisbon |

| 2 | Berlin | Berlin |

| 3 | Frankfurt | Dublin |

| 4 | London | Madrid |

| 5 | Madrid | Frankfurt |

| 6 | Amsterdam | Amsterdam |

| 7 | Munich | Hamburg |

| 8 | Hamburg | Helsinki |

| 9 | Barcelona | Vienna |

| 10 | Lisbon | Munich |

City rankings - Paris takes the lead

Emerging Trends in Real Estate, Europe 2020 has ranked the real estate markets in major European cities according to their overall investment and development prospects.

As we head into 2020, there is opportunity and caution driving Europe’s real estate industry with a focus on cities that offer liquidity and connectivity.

This year's top pick is Paris, noted by survey respondents as the most desirable market given its ability to attract capital of all kinds from around the world.

The 10 European cities expected to fare best in 2020 by survey respondents are a mix of larger, tried and tested markets, with German cities still dominating the top spots.

Contact us

UK and EMEA Real Estate Industry Leader, Partner, PwC United Kingdom

Tel: +44-7710-344-040