The costs and effects of carbon are a growing global concern. Large emitters now are faced with the challenge of how to price carbon and account for its impact.

Emissions trading systems: The opportunities ahead

The European Union’s Emissions Trading System (EU ETS) was a pioneering programme when it launched in 2005, the first in the world to attempt to introduce a compulsory carbon market to reduce emissions in high-intensity carbon-emitting industries.

Companies participating in the EU ETS already account for 40% of greenhouse gas emissions in Europe, and the European Commission has proposed expanding emissions trading to other sectors, including road transport and shipping. Given the importance of the EU ETS—it has led to a reduction of 35% in emissions—and history, other countries are looking to it to learn from its experiences.

In the 16 years since the EU ETS launched, however, no international financial reporting standard has been agreed to address specifically how carbon allowances should be accounted for in financial statements. This lack of standardisation makes it hard for businesses to present themselves to the market, and for the market to understand the financial consequences of emissions and the related credits on companies’ balance sheets.

This was the single biggest criticism of the system by the respondents to a survey prepared by PwC on behalf of the International Emissions Trading Association (IETA) in 2007 and to our latest joint survey, conducted from September 2020 to January 2021.

Survey key findings

The survey includes responses from 25 companies participating in the EU ETS, in industries including oil and gas, cement, steel, chemicals and aviation. We asked questions on how emission allowances are accounted for and how their use impacts their accounting treatment. The results demonstrate the different approaches to accounting for carbon allowances that are used today and may provide valuable insights for other emissions trading schemes. Both the survey and findings are predominantly based on the International Financial Reporting Standards (IFRS).

Too many different reporting methods

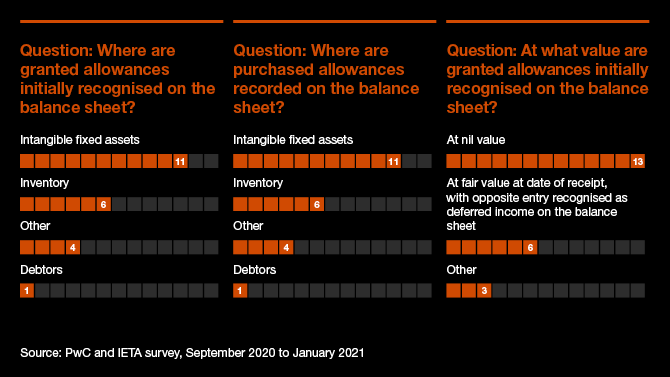

Among the 25 respondents, four different ways were used to account for granted and purchased allowances and three different ways to value granted allowances.

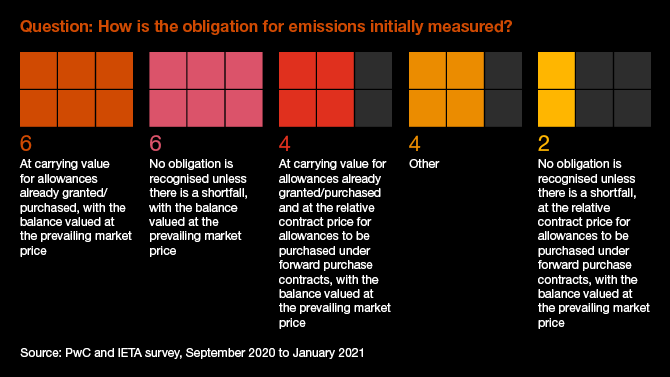

Companies used five different ways to measure the allowance.

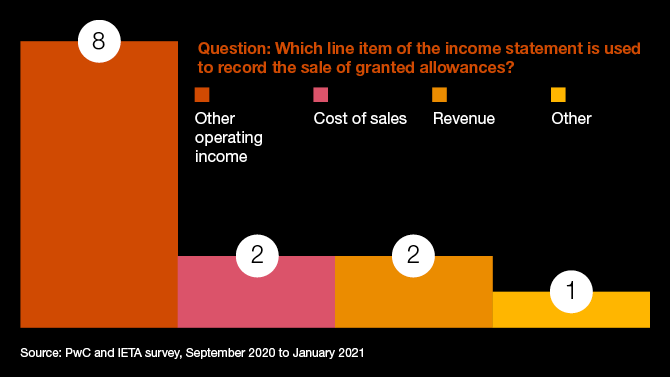

And entered them on four different lines on the income statement.

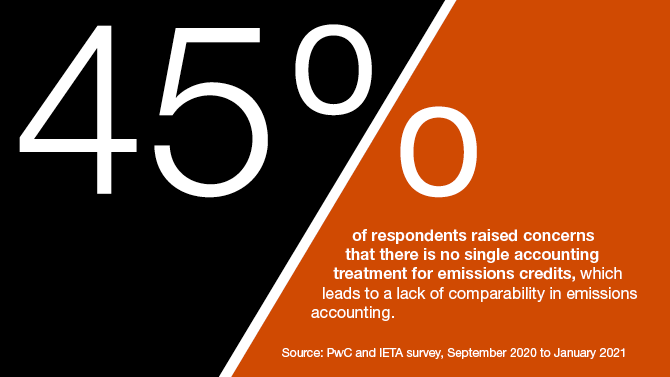

These different reporting methods are causing nearly half of respondents to be concerned about the lack of standardised reporting and its effects.

Setting a standard for carbon accounting

The survey results in 2021 align with the conclusions reached in our survey conducted in 2007, showing that little progress has been made on establishing standardised accounting principles for carbon emissions. Given the evolution of the carbon market in the past 14 years, the increase in prices and the increase in the scope of the EU ETS, we would argue that this continues to be an area that would benefit from common accounting treatment.

Standardisation of accounting for carbon allowances would allow business leaders to show investors and consumers more clearly the cost of their emissions and the impact of their efforts to reduce emissions.

The global community needs to come together to give emissions trading systems, like the EU ETS, a firm foundation on which to help companies make and meet their carbon reduction targets.

Read the full Emissions trading system report

Contact us

Global Energy, Utilities and Resources Assurance Leader, PwC Middle East

Tel: +966 54 766 4151