You may already know about the new EU Foreign Subsidies Regulation (FSR) if you’re thinking about an M&A transaction or making a public procurement bid in the EU. And you likely also know it relates to non-EU subsidies that could give you an advantage. But you may not know just how broad its remit can be.

Did you know for example that the FSR’s scope can include:

- Transactions as part of internal restructuring exercises - it’s not only external M&A that may be relevant. While some transactions automatically trigger reporting obligations, other EU activity can lead to redressive measures or result in a reporting request from the European Commission.

- A wide range of incentives and benefits that you receive from non-EU governments/ local authorities that could provide an unfair advantage in the EU market against EU companies. These could be related to growth, exports, sustainability.

- A look-back period - It is not just current funding that is affected. You need to look back across the corporate group, and potentially more widely, for at least three years and longer in some cases.

All of this makes it more complex than it can first seem.

We are already seeing activity on this in the EU. Only 100 days into the FSR notification period which started on 12 October, the European Commission had participated in 53 pre-notification discussions with 14 progressing to a full reporting notification obligation, and one full investigation. As this is the first time that organisations are undertaking this new filing, which goes far beyond EU Merger Regulation requirements, they are facing the difficulties of gathering the needed data and the tight timeframes.

FSR can have both a significant compliance impact, and failure to comply could also lead to delayed or quashed deals and/or significant penalties. Businesses operating in the EU must prepare for major changes in reporting and competition regulation - not just in terms of FSR but in other areas such as the Directives on Corporate Sustainability Reporting, Minimum Taxation and Public Country-by-Country Reporting. These will not only impact businesses broader governance and compliance/reporting structure, but also their data, processes and controls. The same can be said for increasing global compliance obligations too.

So how should you prepare to ensure your data, people, processes and systems are ready for EU FSR and ‘connected’ to your compliance & reporting processes?

- 1. Assess early the impact of these rules

- 2. Identify risks based on your existing structure and plans

- 3. Gather necessary historical data

- 4. Design governance & oversight

- 5. Design your compliance & reporting function

1. Assess early the impact of these rules

Determining whether a company is in-scope and the level of notification needed is complex. It affects competition issues and the ability to enter or grow within the EU.

2. Identify risks based on your existing structure and plans

Determining whether incentives and other financial contributions from non-EU governmental bodies could be relevant subsidies will be vital. Understanding the exclusions and thresholds is key. And this is not easy, you may need specialist input from Competition Law and State Aid specialists.

3. Gather necessary historical data

Businesses need to notify/ report governmental contributions typically within the prior 3 years on a ‘line by line’ basis. But you will need a flexible process and strategy to gather the data sets required for reporting ꟷ particularly given that the data will be cross functional, i.e. drawn from Tax, Legal, Business Development, Finance, Procurement, Supply Chain, and M&A teams.

4. Design governance & oversight

Businesses need structures, risk management and policies that allow directors to provide oversight and demonstrate compliance with statutory competition requirements. So, you may need a system for identifying, tracking and reporting potential M&A transactions, large public tenders or other EU activity that may be caught by the rules, so that you stay on the front foot.

5. Design your compliance & reporting function

Worldwide financial contribution reporting data points, processes, and controls need to be designed and embedded within the business. Penalties for incorrect or under reporting can be significant. Think about the interaction and potential synergies between FSR reporting and Pillar Two, ESG and wider finance and tax reporting ꟷ simplifying and connecting your reporting processes.

Whilst that feels a lot to do… we have teams of Competition Law, State Aid, Regulatory, Data and Connected Tax Compliance specialists who can help you at each step of the way. Whether it is advice you need to get up and running in the areas above, or a managed services provider to take EU FSR monitoring and compliance reporting off your hands, we are here to help. Please visit our EU FSR website to find out more.

Don’t let being unprepared for these rules block a business and time-critical transaction or prevent you from accelerating the growth of your business. Staying one step ahead of these rules is essential.

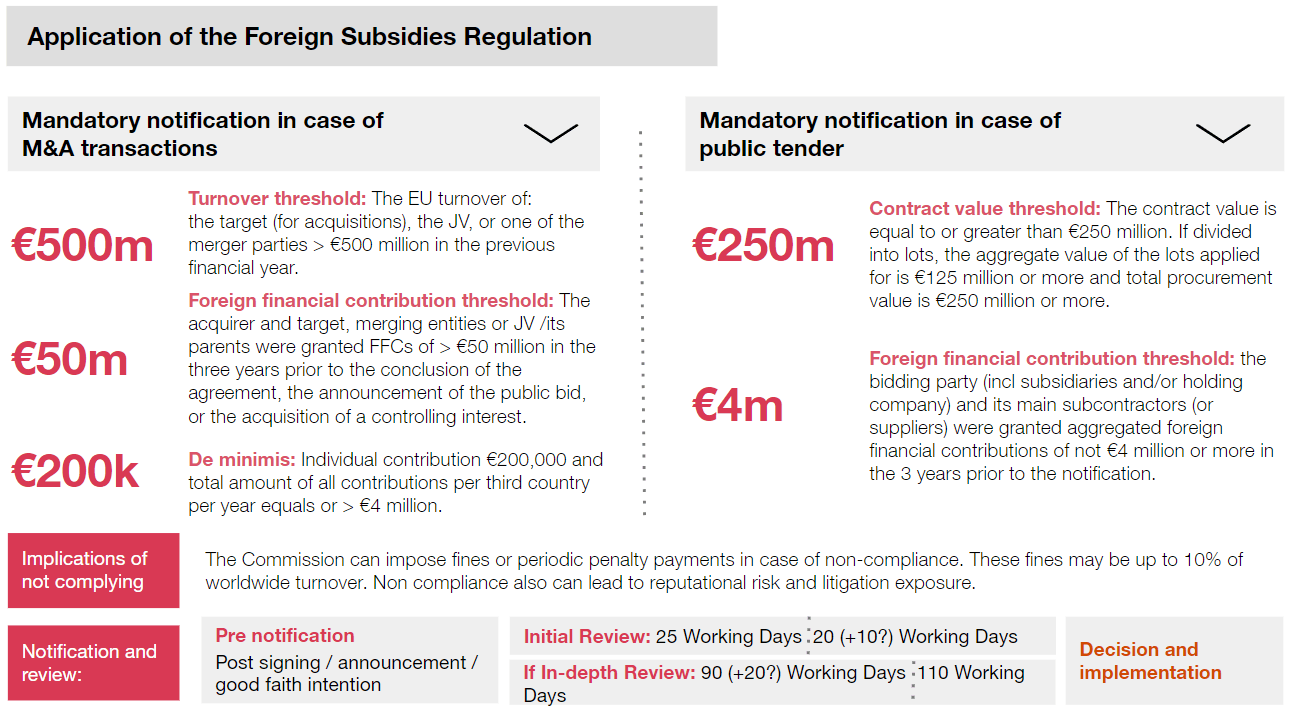

The application of the FSR

The reporting process hinges around the matters set out in the table below. Note the distinction between ‘foreign financial contributions’ (FFCs), which need to be reported, and those FFCs that the Commission decides are ‘subsidies’ that distort competition and may result in action. You cannot decide which FFCs are distortive, only the Commission can do that. So you need to have data on all FFCs, which may, for instance, include guarantees; exclusive rights without proper remuneration; grants, financial assistance (loans, financing, and repayable advances; risk capital instruments; equity intervention; and debt write-offs) and many tax advantages.

Contact us

Deputy Global Tax Policy Leader, EMEA Tax Policy Leader, PwC Netherlands

Tel: +31 88 792 3611