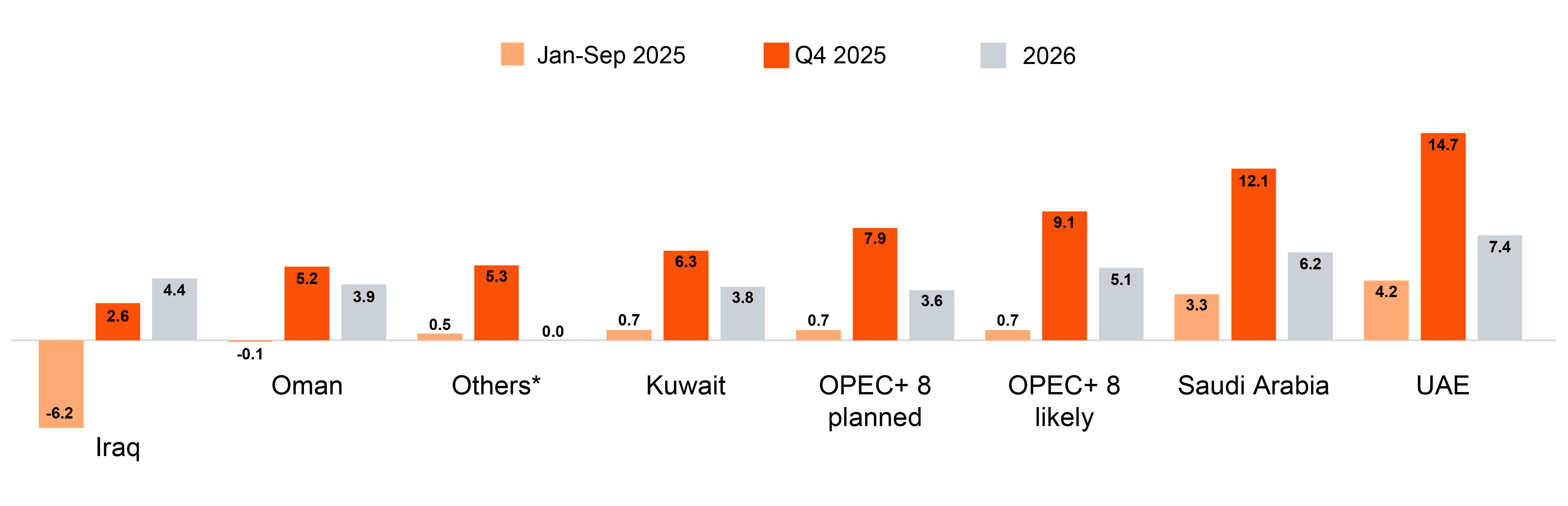

The increased production by OPEC+ is one of several factors weighing on oil prices, along with strong production growth by non-OPEC+ countries in the Americas and growing concerns about weaker global demand. The IEA forecasts a nearly 4m b/d of excess supply in 2026.6 That said, there are geopolitical risks to supply, particularly expanded sanctions on Russia, as well as a potential recovery in industrial demand if trade uncertainty abates, which could temper oversupply concerns.7

On 17 October, the spot price for Brent crude dropped to US$60 for the first time since 2020. This compares with an average of US$71 for the first nine months of the year and $81 in 2024. Against this backdrop of softening prices and market uncertainty, OPEC+ has decided to pause further production increases in early 2026, delaying the restoration of the remaining 1.3m b/d of cuts until market conditions warrant a reassessment.

The latest IMF forecasts are for fiscal deficits in 2026 – 3.7% of GDP for Saudi Arabia and 9.9% of GDP for Bahrain, assuming oil would be at US$66 per barrel, with surpluses for the UAE, Qatar and Oman. Kuwait is the outlier – its fiscal year begins in April and the IMF only sporadically publishes central government forecasts, but World Bank forecasts point to a deficit of 4.5% of GDP in 2026/27. Overall, GCC fiscal balance forecasts are projected to remain broadly similar to 2025, with higher output expected to partly offset weaker prices. However, if oil remains lower for longer, fiscal positions across the region are likely to come under renewed pressure, testing the resilience of spending plans and reform commitments.

Real economic growth remains robust

Higher oil production, irrespective of prices, provides a boost to real GDP growth. The OPEC+ tapering is the main reason why the International Monetary Fund (IMF) in October revised up its growth forecasts for most of the GCC, including lifting its forecast for Saudi growth to 4.0% in 2025 and 2026.8

However, the non-oil sector is also growing strongly in most countries. In the first half of the year (H1), Abu Dhabi led the GCC with 6.4% non-oil growth, while Qatar recorded 5.3% and Saudi Arabia 4.2%. Leading indicators in the second half of the year are also looking robust; for example, Saudi Arabia’s Riyad Bank Purchasing Managers’ Index (PMI) surged to 60.2 in October 2025 – the highest level since 2014 – driven by the fastest hiring growth in 16 years,9 while the UAE’s index stood 54.2 in September.10

Growth has been broad-based. Among the four GCC countries that had reported H1 GDP at the time of writing, nearly all sectors recorded positive performance, with only a few exceptions, such as communications in Qatar. In most cases, sectors expanded by at least 3% and several posted double-digit gains, such as hospitality in Oman which grew by 12.3%, while retail and wholesale trade in Qatar rose by 11.6%.

In addition to country and sector-specific drivers, several common elements facilitated growth across the GCC. The easing of US interest rates stimulated credit growth, while low inflation, averaging only 1.5% across the region in the first seven months of the year helped sustain demand. Excluding rent increases in a few hotspots, particularly Riyadh and Dubai, consumer prices across much of the region were nearly flat.

Elsewhere in the Middle East, performance was more mixed. Egypt’s economy grew by 4.9% y/y in H1 (calendar year), marking its best six-month performance since 2021. Reforms implemented since 2024, including currency depreciation, have boosted competitiveness and investment. This was despite the war in Gaza, which continued to hurt Suez Canal traffic and tourism. If the ceasefire negotiated in October can be sustained, then that should provide a boost not only to Palestine, but also to Egypt, Jordan and Lebanon.

Why it matters

While oil continues to play a central role in the GCC’s economic landscape, diversification efforts are clearly gaining momentum. The region’s non-oil sectors are proving increasingly dynamic and resilient, supported by investment, reform and expanding trade ties. Although the oil market remains inherently difficult to forecast – and a prolonged period of lower prices could weigh on fiscal positions – robust non-oil activity is helping to sustain growth and confidence across much of the GCC. Steady production levels may further cushion short-term pressures, while markets such as Dubai are demonstrating how diversification can meaningfully reduce exposure to oil cycles and underpin long-term economic stability.