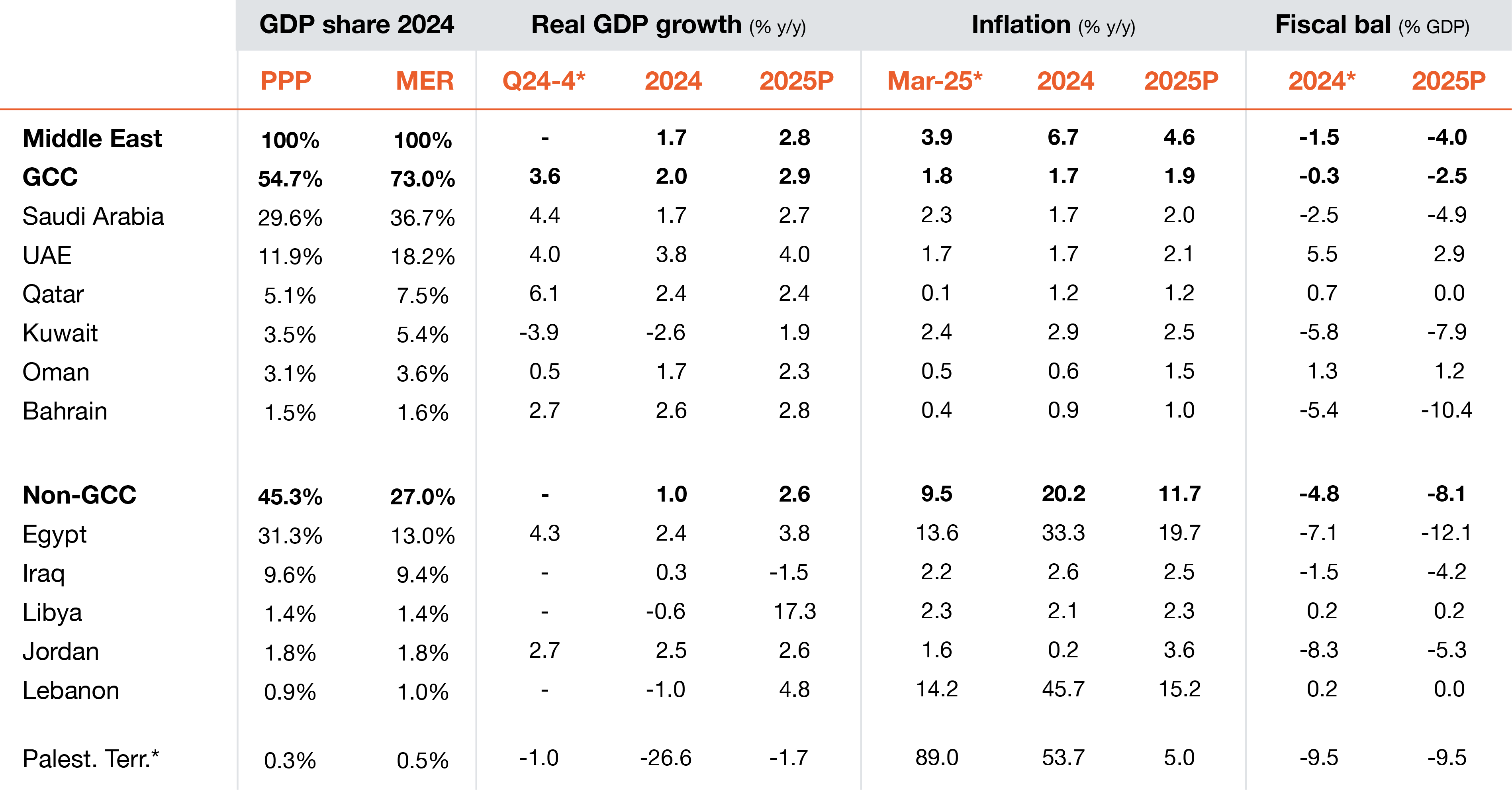

Data and projections

Sources: PwC analysis, National statistical authorities, IMF estimates and forecasts (WEO, Apr 2025; Kuwait Article IV) and for Lebanon and Palestine, World Bank (Apr 2025). *GDP: UAE Q3; Inflation: Dec (Libya, UAE), Feb (UAE, Iraq); Fiscal balance: Kuwait (IMF Article IV).

Chart of the quarter

Data centre investments boom

Data centres, once seen primarily as infrastructure for cloud computing and website hosting, have now become central to powering AI models - driving a projected 165% increase in demand globally by 2030.35

The Middle East is rapidly emerging as a data centre powerhouse, with regional capacity expected to triple, from 1GW in 2025 to 3.3GW over the next five years.36 This growth is driven by a surge in cloud computing and AI, an increasing demand for digital infrastructure, substantial investments by both global hyperscalers and regional players and supportive regulatory initiatives, for example, Saudi Arabia’s regulations requiring local storage of personal and financial data.

Additionally, the region’s strategic location offers high-speed connectivity across Europe, Africa, and Asia, making it a hub for processing digital services from neighbouring markets with limited infrastructure. It also benefits from a supportive business environment, with access to land, talent and low-cost energy. In addition, strong public and private capital drives rapid regional data centre investment.

The Gulf Data Centre Association reports that the region had 648MW of installed data centre capacity in 2024,37 primarily concentrated in Saudi Arabia and the UAE. New facilities currently under construction are set to boost capacity by more than 50%, bringing the total to nearly 1GW. Many additional projects are also in the planning phase. This will raise per capita capacity across the GCC to about 15W/capita next year, doubling the current global average of about 7W/capita based on 55GW of global supply.

Power availability and consumption are critical considerations and as AI adoption accelerates, ensuring a reliable, scalable power supply becomes essential. In response, governments in the region are adopting more integrated planning approaches, aligning data centre development with energy infrastructure to meet growing demand. In this context, the Middle East’s investment in renewables—solar, wind, and green hydrogen – can offer a strategic advantage by supporting both sustainability goals and long-term cost efficiency.

Source: Gulf Data Centre Association

References

[35] Goldmansachs.com ‘AI to drive 165 increase in data center power demand by 2030’

[36] https://www.pwc.com/m1/en/media-centre/articles/unlocking-the-data-centre-opportunity-in-the-middle-east.html

[37] Gulf Data Centre Association Market Reports – various survey reports

Contact us

Richard Boxshall

Global Economics Leader and Middle East Chief Economist, PwC Middle East

Tel: +971 (0)4 304 3100

Carlos Garcia

Partner, ME Customs and International Trade lead, Tax & Legal Services, PwC Middle East