As we publish the latest Middle East findings from our 2021 Global Consumer Insights Survey, it is clear that as a result of extensive vaccination programmes consumer confidence is rising across the region. In fact, 58% of Middle East consumers confirmed that they have become more optimistic about the economy.

Despite this confidence, the results show that the economic and social consequences of the health crisis have impacted consumer behaviour and that those changes are here to stay. In this rapidly evolving market landscape, Middle East retailers must rethink their business models to ensure they are meeting their customers’ changed expectations and do so quickly.

Our survey charts the shift in consumer attitudes after a period of upheaval and provides guidance about how retailers can seize the opportunities ahead.

| For the 2021 Global Consumer Insights Survey, we adopted a ‘pulse’ approach and fielded two surveys, one in November 2020 (‘Pulse 1’) and the other in March 2021 (‘Pulse 2’), in order to remain attuned to changes in the worldwide landscape and connected to the behaviours of the global consumer. |

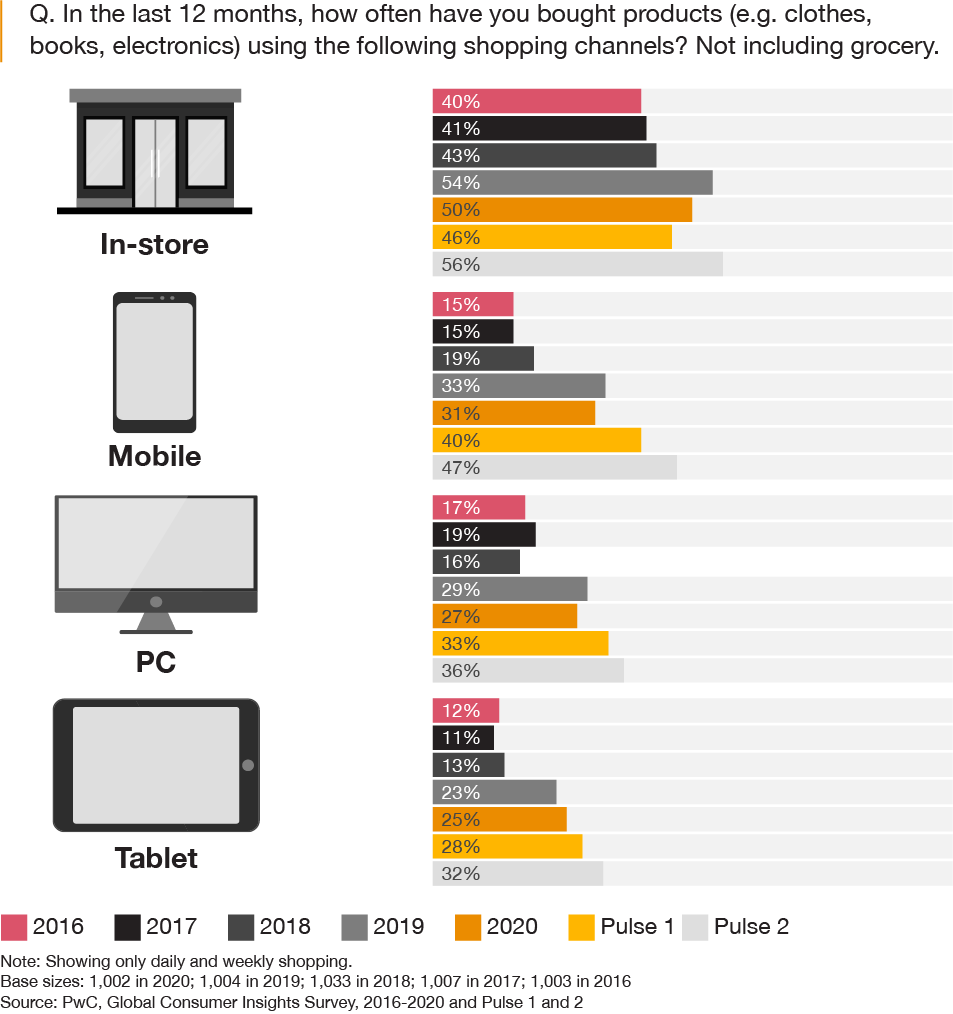

47% of Middle East consumers frequently use their smartphones for purchases

In our 2020 Global Consumer Insights Survey, fielded before the outbreak of the health crisis, 31% of Middle East respondents said they were shopping via their mobile phone on a daily or weekly basis.

Our latest data shows that mobile is now the main online channel and that there has been a significant shift to digital across the Middle East – 67% of regional consumers believe they have become more digital between October 2020 and March 2021, compared to 51% of global consumers, particularly in Egypt where 72% of consumers confirmed that.

As a result of the health crisis, we have also seen an increase in the number of people going online for groceries – in our 2020 Global Consumer Insights Survey just 6% of consumers said they purchase groceries exclusively online while in our Pulse 2 survey the same was confirmed by 18% of respondents.

Like for global shoppers, a major consideration for Middle East consumers shopping online continues to be fast and reliable delivery. As a result, we’re seeing more retailers, from luxury sites to grocery stores, offer same-day delivery.

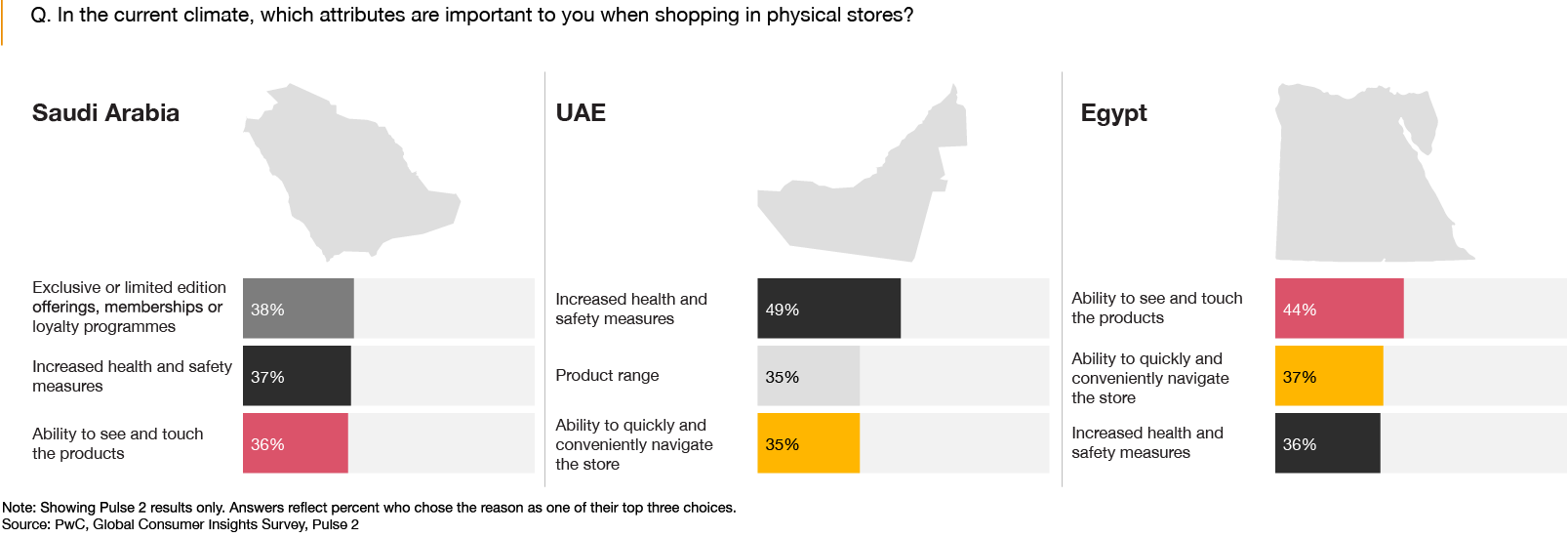

56% of Middle East consumers prefer visiting physical stores

The results suggest that in-store shopping will remain important to Middle East consumers for many reasons. Shopping malls and physical stores are places to inspect the products in person, explore special offers, and also spend time with friends and family.

Not surprisingly, consumers who shop in-store consider increased health and safety as one of the most important attributes for a physical store ‒ 40% of regional consumers ranked it as their top concern. Key safety measures that consumers expect from a store include mandatory face masks (44%), social distancing (43%), hand sanitisation stations (32%) and reduced capacity (31%).

Given these worries, retailers will need to maintain rigorous health and safety regimes in the coming months while leveraging technologies, such as virtual reality tools, to attract customers by enriching their in-store experience.

57% of Middle East consumers have been more price oriented during the pandemic

Despite widespread vaccination programmes and increasing consumer confidence across the region, shoppers remain more price conscious than before the pandemic – 66% said they have been focused on saving, compared to 54% of global consumers.

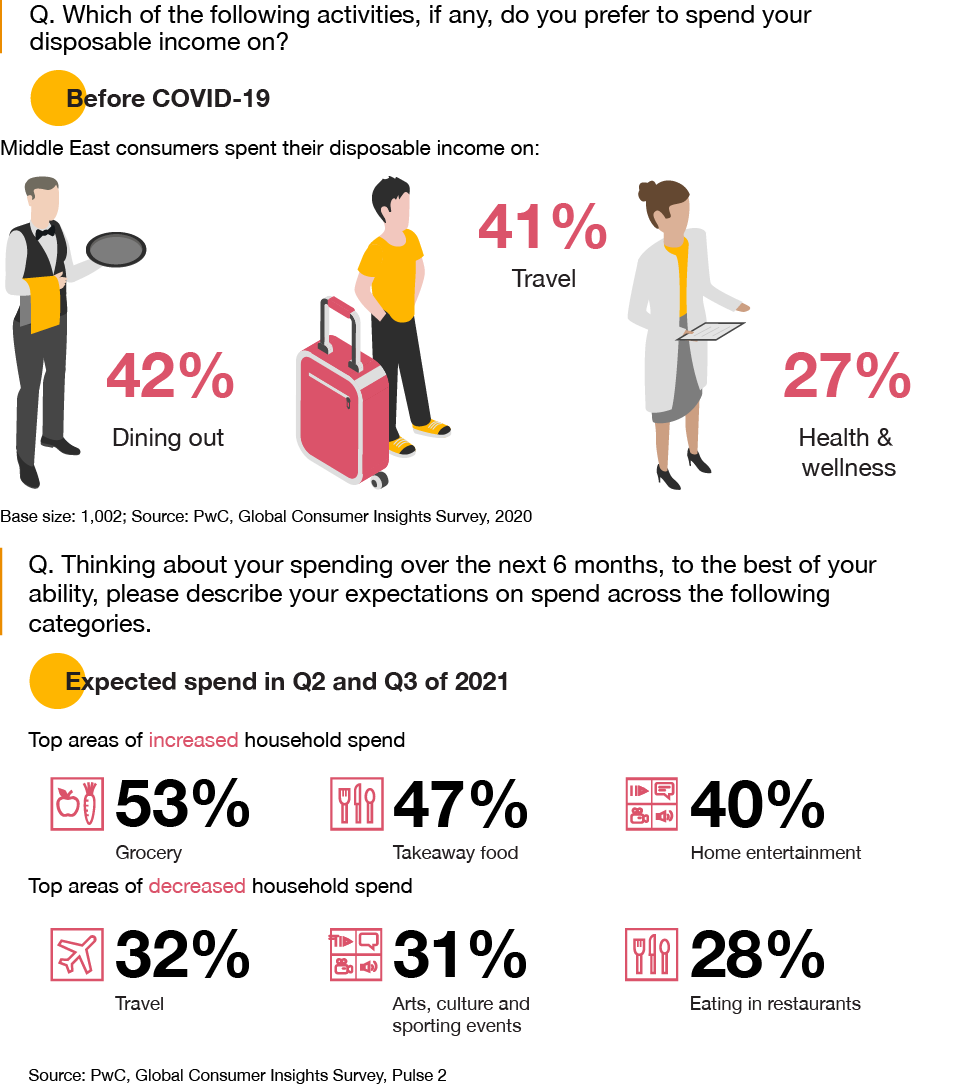

When consumers do spend money, they are more likely to spend it differently than before the pandemic. In our 2020 Global Consumer Insights Survey, Middle East consumers were spending their disposable income on eating out at restaurants (42%), on travel (41%) and health and wellness (27%). In our latest findings we see that, in Q2 and Q3 of 2021, 53% of regional consumers are expecting to spend more on groceries, 47% on takeaway food and 40% on home entertainment.

This is perhaps not surprising given that five out of 10 consumers said that they are mostly working, dining, consuming entertainment, working out and interacting with friends and family at home.

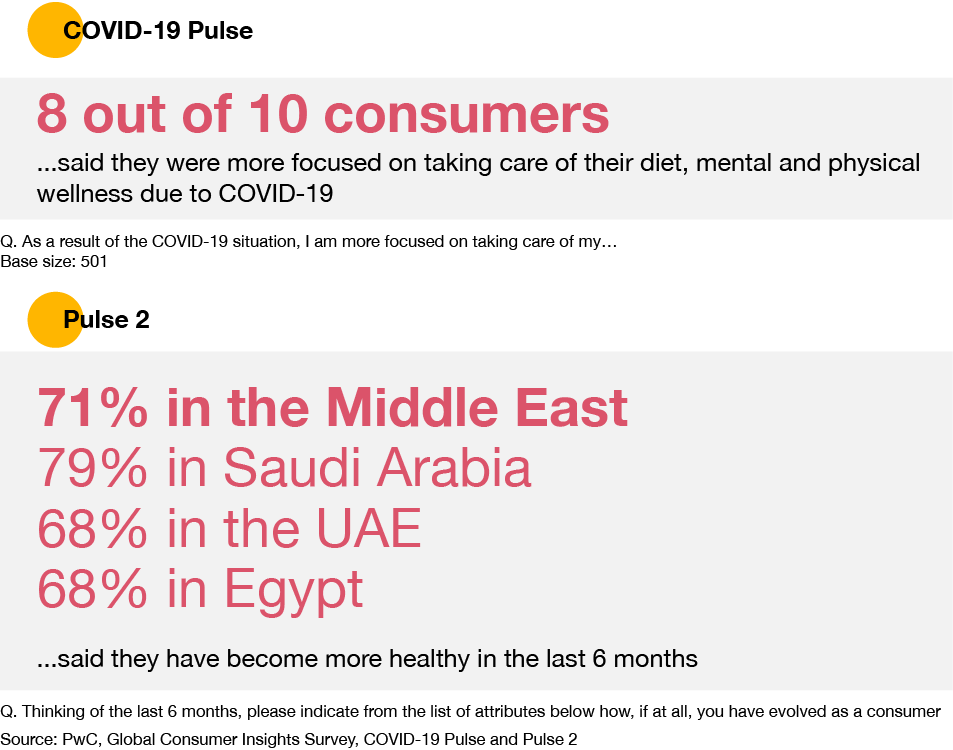

71% of Middle East consumers have become more healthy during the pandemic

As with their counterparts globally, the health crisis has dramatically increased awareness of health and wellness among Middle East consumers. In the 2020 Global Consumer Insights Survey, more than half (58%) of respondents said they were making time each week to improve their health and general wellness and adopt a better diet. This rising health consciousness is reflected in our Pulse 2 results, particularly in Saudi Arabia where 79% of consumers said they have become more healthy.

When shopping for groceries, 41% of respondents say that they are willing to pay more for healthier options. Surprisingly, men are more likely to pay for healthy grocery options than women – 45% vs. 41%. Responding to this demand, food retailers in the region are increasing their range of healthy or diet products.

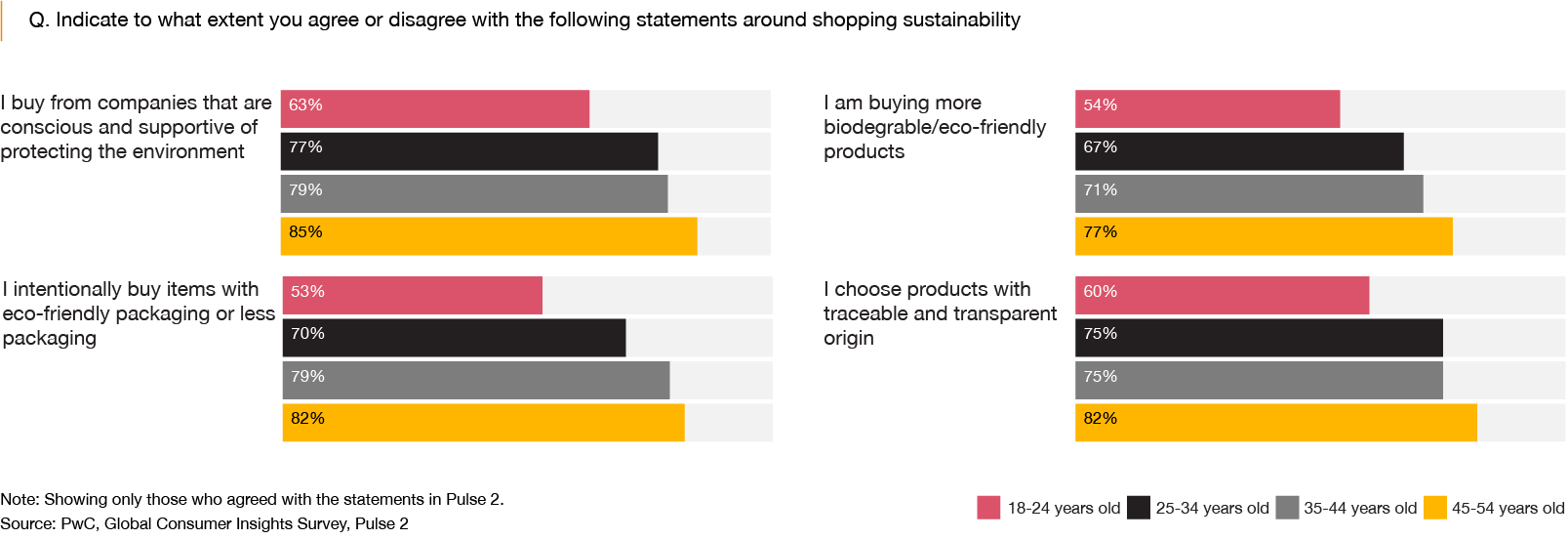

65% of Middle East consumers have become more eco-friendly during the pandemic

The health crisis has reinforced the growing awareness of Middle East consumers about social and environmental sustainability. Overall, seven out of 10 Middle East shoppers say that they engage in sustainable behaviours, with respondents from the region consistently outscoring the global survey participants on a range of questions in this area.

It is interesting to note that this environmental consciousness has seen an uptick from our Pulse 1 survey – at the time six out of 10 consumers agreed with our sustainability statements – and that younger, Generation Z, consumers are less likely to agree with those statements. In fact, the older the shopper the more likely they are to care about sustainability.

Consumers who are not prioritising sustainability, believe there is a lack of sustainable options (39%), that the quality of those products is inconsistent (36%) or that they are priced too high (35%).

With social and environmental sustainability more in focus than ever before, retailers need to rethink how they approach these considerations and ensure they are committed to environmental, social and governance (ESG) factors before governments start regulating them.

Facing the future

A rapidly evolving consumer landscape will require equally fast, focused action by retailers

As the pandemic subsides and they prepare for the future, retailers across the region will need to be fast and agile to capture business from a rising generation of youthful, socially aware consumers who are digital natives. They can do this by gaining actionable insights into their operations, keeping their businesses robust and becoming more sustainable.

Here we highlight some key measures for retailers at each stage of their transformation.

Repair

- Using new AI-enabled technologies to improve efficiency in supply and distribution chains disrupted by the health crisis

- Real-time data collection about offline and in-store consumer behaviour and purchases to driver actionable insights

- Employee communication, engagement and empowerment

- Consumer communication and engagement to further build trust

Rethink

- Channel strategies as more consumers purchase via mobile and other devices

- The concept of the physical store and, in particular, the in-store experience, utilising technology to attract customers while maintaining rigorous health and safety standards

- Brand and portfolio propositions that are aligned to evolving consumer behaviour

- ESG, health and wellness as major business priorities that require an actionable mission statement

Reconfigure

- Sales and marketing channels to capture growing mobile phone shopping

- Marketing strategies, in an environment where many consumers will continue to work from home

- HR management, ensuring the health and wellness of employees and consumers is a business priority

The speed of the shift in consumer sentiment reflected by our findings is a reminder that retailers cannot afford to adopt a wait-and-see strategy as the region’s shoppers emerge from a period of lockdown, economic uncertainty and emotional stress. A new, digitised market is taking shape, which already looks increasingly different from the region’s pre-pandemic consumer landscape.

“Digitalisation and sustainability are firmly at the top of consumers’ agendas. To prepare for the future, retailers across the region will need to be fast and agile to capture business from a rising generation of youthful, socially aware consumers who are digitally savvy.”

Explore the data from the Global Consumer Insights Survey 2021

Browse and compare our survey data by country or category.

About the survey

The regional respondents were from the UAE, Saudi Arabia and Egypt, at least 18 years old and were required to have shopped online at least once in the previous year.

The Middle East base size for Pulse 1 is 513 and 515 for Pulse 2. Where we’ve included data from previous surveys, the base sizes are listed below the graph.

Contact us