As you move from assessing your readiness to the planning and preparation phase, you’ll need to answer important questions related to financial information and your track record:

Are audited financial statements of your company available based on the listing requirements?

Does your company report under accounting standards for private enterprises (ASPE) and require conversion to international financial reporting standards (IFRS) or generally accepted accounting principles (US GAAP)?

- Do your financial statements include all relevant public company disclosures?

- Have there been any restatements of financial statements previously issued? Do you need to adjust historical financial information?

- Is your information robust and comparable?

- Are the historical financial statements consistent under both IFRS and US GAAP?

- Do you need to look at early adoption of new accounting standards?

- Do you need more recent audited or reviewed financial information to meet eligibility criteria?

Have you made significant acquisitions or disposals in the past years? Do you plan to disclose any prospective or pro forma financial information?

Featured - 2 items

Common accounting issues for companies looking to go public:

Calculating earnings per share (EPS): An IPO often includes a number of transactions that affect the calculation of EPS.

Understanding transaction costs: Complexities arise in relation to the split between capitalization to equity and expensing through the profit-and-loss statement based on the type of cost and transaction (listing new or existing shares or a business combination).

Identifying segments: Identifying the entity’s chief operating decision maker and operating units is essential to determining the reportable segments that are publicly disclosed.

New and existing employee share-based payment arrangements: Know the accounting implications and expected earnings impacts from employee share arrangements. These may change or be cancelled as a result of a change-of-control clause triggered by a proposed IPO.

Share capital: Regardless of the structure of the IPO, it’s possible the type and number of shares or the value of share capital will change.

Other important steps in IPO planning and preparation

- Appoint advisors

- Assess key management

- Project management

- Review compensation and incentive plans

- Early-stage marketing

- Tax and legal structuring

- Determine board composition

- Review internal controls

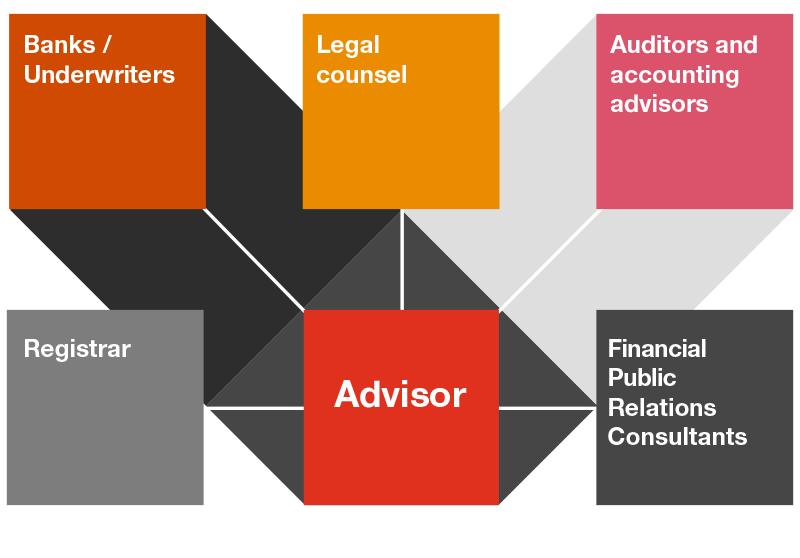

Appoint advisors

Who do you trust to work with you? Key professional advisors include banks/underwriters, legal counsel, auditors and accounting advisors, registrars and financial public relations. Consider whether you need interim resources to support your key management during the IPO process.

Who are the key professional advisors?

Assess key management

Your management team is pivotal to the entire offering process and critical in making the strategic decision to go public. The team evaluates the company’s readiness, monitors the process and makes key decisions.

Your management team will also come under close scrutiny as you take the company public, as investors will want to ensure their funds are well invested. The team will need to be a cohesive unit that shares a long-term vision and demonstrates to prospective investors its depth of experience, expertise, commitment and integrity.

Management’s experience in taking a company public is a definite asset. Investors look for executives with a successful track record in building companies and the ability to deliver shareholder value. You’ll have an opportunity to communicate your track record via the prospectus and roadshows, but you’ll also gain credibility by having key members of your team in place for some time.

Project management

Project management is key to keeping the IPO on track and ensuring the process runs as smoothly and efficiently as possible.

Review compensation and incentive plans

You’ll also need to determine your remuneration structure for senior executives and management, ensuring it’s the right fit for the listed environment.

Early-stage marketing

Which investors should you target and what will they want to know about you? Prepare the early-look presentation with your advisors and determine the type of feedback you’ll need from these meetings. You should do this well ahead of the formal IPO process.

Tax and legal structuring

Like any significant transaction, going public has tax implications. Tax planning before the IPO will give a company and its shareholders the best opportunity to maximize the advantages and minimize the disadvantages of being a public company.

Have you identified the legal entity to be floated? What legal entity/structure reorganization will you need to undertake? Where will your holding company be located?

Other tax matters include:

Dividends: A public company must first pay non-eligible dividends, which have a lower tax credit. A Canadian-controlled private corporation (CCPC) may need to pay these dividends before the IPO.

Capital dividends: Once a private company goes public, it can’t pay tax-free capital dividends to its shareholders. The capital dividend account should be accessed as part of planning the IPO.

Returning capital: Private company shareholders may receive their investment without tax implications. A public company’s return of capital to shareholders will only be tax-free in limited circumstances.

Changes in tax rates: Becoming a public company means ineligibility as a CCPC. This means a higher tax rate for business income, reduced tax credits on qualifying scientific research and development expenses and a loss of refundable tax on investment income.

Estate and retirement planning: It’s possible to reorganize shareholdings to allow family members to participate in the company’s growth after the IPO. Once the company is public, its shares will qualify for registered retirement savings plans, tax-free savings accounts and other tax-deferred options that aren’t available to private companies.

Changes in tax reporting: Upon IPO and an acquisition of control, various rules requiring the realization and expiration of losses will apply. The statute of limitations for tax audits increases to five years and you must pay income taxes within two months of the taxation year end.

Taxation on the IPO: Fees directly related to the issuance of shares are generally deductible over five years. Other fees in the period of the IPO may be deductible at 5% a year. Shareholders can access their lifetime capital gains exemption on qualified shares.

Stock options: Since there’s a market for public company shares, employees with options will be able to realize the benefit from their investment more easily. The taxation of stock options differs in some respects between a public and private company.

Determine board composition

A strong board is an invaluable asset. Your directors will enhance shareholder value by bringing experience and specialized expertise, business contacts and an objective perspective to your company. They’ll also act as an important sounding board for you and your management team on key strategic decisions. What are some of the issues related to the board that you should think about?

Independent board of directors: Ideally, you want an independent board of directors with a broad range of expertise. The right mix and credentials will speak volumes about your company. That being said, attracting the right people is easier said than done. Due to legal exposure, it can be a tough sell to attract the best board members. Securities laws hold directors responsible for “full, true and plain disclosure of all material facts” relating to the issuing of securities. Board members can be held liable for the information (or lack thereof) in the prospectus. Although insurance can help protect directors against some liabilities, it’s expensive and doesn’t cover all potential scenarios.

Audit committee: The purpose of an audit committee is to provide oversight of the external auditor. This involves giving recommendations on the nomination and compensation of the external auditor, approving all non-audit services and performing a review of financial statements, management discussion and analysis (MD&A) and annual and interim earnings press releases. Canadian requirements are less prescriptive than the equivalent US provisions. Audit committee members under Canadian requirements generally must be financially literate. Under the US regime, all members must be financially literate and at least one member must be a financial expert.

Nominating committee: This committee leads the process for board appointments, evaluates the board and its committees and makes recommendations.

Remuneration committee: This committee is responsible for setting remuneration for all executive directors and the chair, including pension rights and any compensation payments.

Review internal controls

If filing on the TSX or the NEO, the chief executive and chief financial officers will need to certify that the financial statements are materially accurate and there hasn’t been a material change in the control environment.

Annual and interim filings require quarterly certification relating to internal controls. You must demonstrate the company has:

designed internal controls over financial reporting (ICFR), disclosure controls and procedures (DC&P) and a control framework; disclosed (in the MD&A), if necessary, material weaknesses relating to design and effectiveness; reported (in the MD&A) changes in the ICFR; evaluated the effectiveness of the ICFR and DC&P; received annual certification relating to internal controls.

After an IPO, there’s an option to file a special certification form that gives you a reprieve from the internal control certification for the financial period following the IPO date. This, in effect, gives you one quarter of reprieve from the internal control certification requirements (for example, if the IPO is in the third quarter, the first full certificate including internal controls will be required for the fourth quarter).

More IPO stages

Related services

Contact us