Non-oil sector leads growth in 2023

Private sector growth accelerates

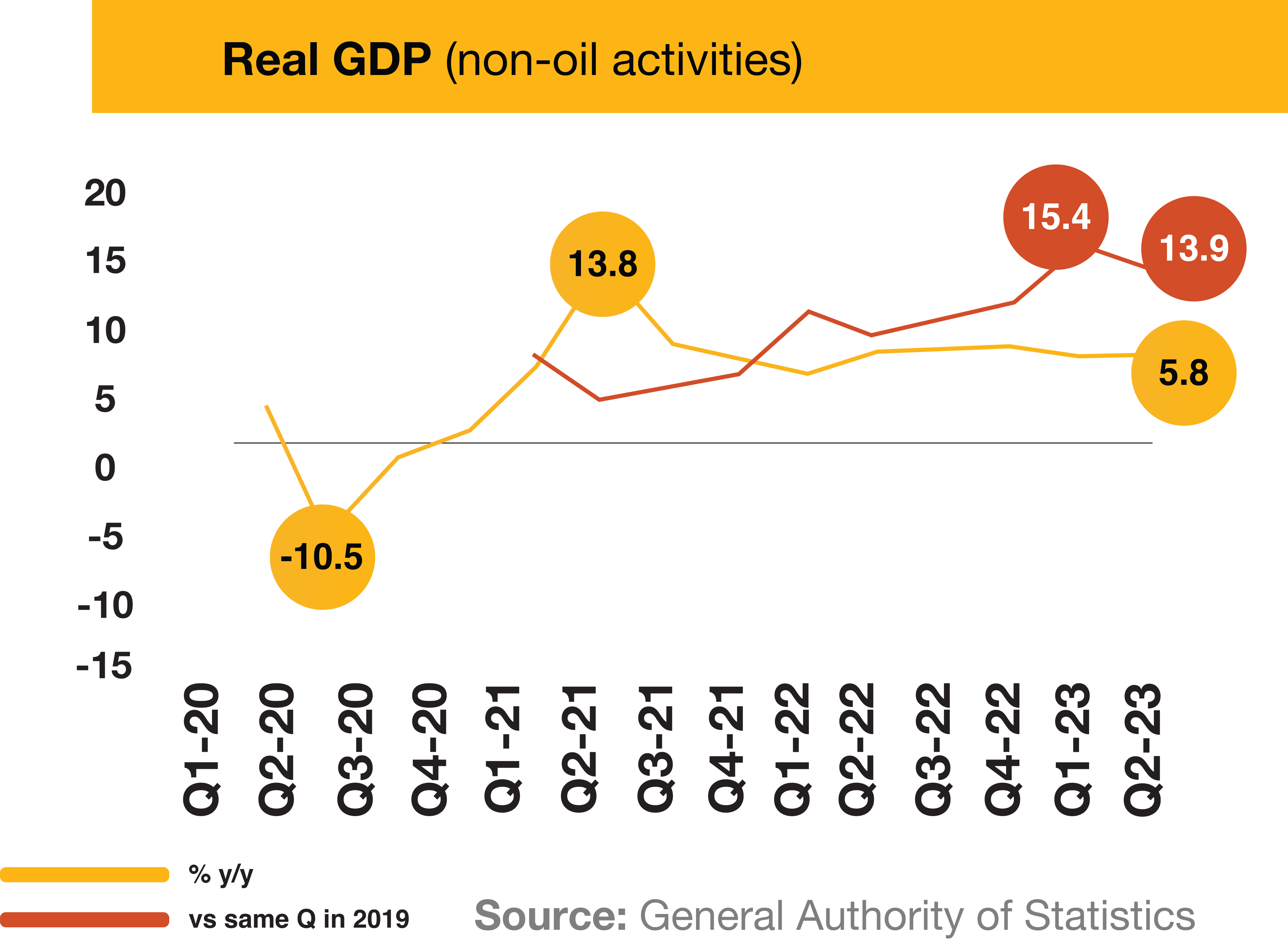

Non-oil private sector growth accelerated to 5.8% y/y in Q2 2023 and stood 13.9% higher than in 2019. By contrast, the non-oil government sector growth slowed to 3.8% y/y, while the oil sector contracted by -4.3% y/y as a result of production cuts.

The major sectors that had grown well beyond their pre-COVID-19 levels as of Q2 included trade and hospitality (up 25% vs 2019), thanks in part to the rebound in religious tourism with a strong demand for Umrah (the Hajj will contribute to Q3 GDP), manufacturing (17%, excluding oil refining) and finance and business services (up 16%). Utilities, agriculture and government services were the only sectors that slightly lagged their 2019 levels.

The strength of Saudi Arabia’s post-COVID-19 recovery substantially exceeds other Gulf states. In Q1-23, Bahrain was the next best-performing nation-state in the region with GDP 6.3% higher than in 2019, but less than half the Saudi growth over this period.

The Purchasing Managers Index (PMI) registered 56.6 in August, which indicates non-oil economic expansion. This was less than the extremely strong average reading of 59.1 in H1 2023 but was still strong by historic standards and ahead of PMIs elsewhere in the region.

KSA bears the burden of OPEC+ cuts

Crude oil production reached a peak of 11.0m barrels a day (b/d) in Q3 2022, a level that had only ever been exceeded in November 2018 and April 2020 (11.1m and 12.0m b/d respectively, according to official figures). This proved to be the high point of the OPEC+ tapering process.

Since then, the Kingdom has implemented three rounds of production cuts in response to declining oil prices amidst concerns about the strength of the global economy. The first round came into force in November 2022, which reduced the Kingdom’s quotas by -4.8%. As other producers are already producing below their allotted quotas, the cuts therefore fell more heavily on KSA and other states with genuine spare capacity. The second round of cuts, beginning in May 2023, saw a further -4.8% cut by KSA, this time as part of what were described as “voluntary” cuts by a group of eight OPEC+ countries, including the UAE, Kuwait and Oman. The final round, which began in July, was a unilateral move by Saudi Arabia to cut an additional 1m b/d (10% of the total), bringing output down below 9m b/d for the first time in two years.

The additional cut was originally slated for only one month but has now been extended until the end of the year. Moving into 2024, both the additional cuts and the May cuts are set to expire, which would see production rebounding by 1.5m b/d in January to 10.5m b/d. Of course, OPEC+ and Saudi Arabia itself can choose to shift production up and down relative to these plans, with just a month’s notice, depending on the assessment of supply-demand dynamics in the market.

So far this year, Western economies and oil demand have been stronger than anticipated but the Chinese recovery, following the end of its zero COVID-19 policy, has been slower than expected. Meanwhile, supply growth from non-OPEC+ countries, including Iran and the US, has been quite strong and some of the previously underperforming OPEC+ members such as Nigeria have seen a recovery in output.

At the time of writing, the production cuts did seem to have contributed to a partial recovery in oil prices, with Brent crude reaching $92 in mid-September, the most in nearly a year, although oil market dynamics can shift quickly.

At the same time as controlling its current output, Saudi Arabia continues to invest in expanding its capacity. There are different estimates of the Kingdom’s current Maximum Sustainable Capacity (MSC), defined as a level that could be reached within three months and sustained for an extended period. The International Energy Agency estimates that it is 12.25m b/d, which is in line with government figures (12.0m for Aramco fields plus 0.25m for Saudi Arabia’s share of the Saudi-Kuwaiti divided zone fields).

Aramco is investing to boost its MSC by 1m b/d on a net basis, which takes into account the decline in production in more mature fields. This will come onstream in phases, reaching 12.3m in 2025, with new output from the Damman, Marjan and Berri fields, 12.7m in 2026 with the Zuluf expansion, and the full 13m in 2027 as the Safaniyah expansion is completed.

It remains to be seen how close actual production will come to the MSC, as this level has never been seriously tested and the Kingdom typically chooses to keep a substantial buffer in reserve. The most recent long-term forecasts from the IMF, in its 2022 Article IV report, which did not anticipate the 3 recent rounds of cuts, saw output rising gradually to just 11.4m b/d in 2027, which would imply that close to 2m b/d would remain in reserve.

Continued commitment to government investments

Performance dividend partly offsets lower oil exports

The surge in oil prices in 2022, as a result of the war in Ukraine, boosted oil revenue by 52% y/y and led to the first annual surplus since 2013, at 2.5% of GDP. Of course, that was an unusual year and oil revenue will be weaker in 2023 given both lower prices and production. Oil revenue was down by -17% y/y in the first half, during which there was a fiscal deficit of 0.4% of GDP. On current plans, production will be -12% lower in the second half of the year than in the first half, although oil prices have been a little higher so far in H2 and this looks likely to continue.

Although oil export revenue for 2023 as a whole will be substantially lower than in 2022, fiscal revenue will get a boost from the new Aramco performance dividend which will be paid quarterly starting in September, redistributing most of Aramco’s free cash flow built up during 2022. This will boost the government’s quarterly dividend receipts by about a third and lift 2023 fiscal revenue by about 1.5% of GDP and 2024 revenue by twice that amount.

Non-oil revenue remains buoyant

The diversification of the budget into non-oil revenue sources has been one of the most significant trends in recent years. Non-oil revenue was 32% of the total in 2022, despite high oil prices, up from just 8% a decade before. In H1 2023 non-oil revenue growth picked up again to 11% including a 66% surge in revenues from income tax (on foreign companies) to nearly the SAR24bn budgeted for the full year. There have been no changes in tax rates, as the increased revenue reflects stronger corporate profits. Taxes on goods and services, which include VAT and comprise the bulk of taxation, saw a more modest increase of 4%.

Expenditure growth is likely to continue in line with Vision 2030 goals

Although the pandemic imposed additional burdens on the government, the period of lower oil prices in 2020-21 also added to the impetus for greater control of expenditure. This built on plans that were already in place before the pandemic to bring down spending to balance the budget: The three-year projections in the 2020 budget aimed to cut spending by -3% a year and targeted total spending that was -15% less in 2020-22 than had been envisaged in the 2019 budget. Although spending on goods and services rose sharply due to pandemic costs in 2020 and 2021, spending restraint was visible in other key lines of expenditure including compensation of employees, subsidies, social benefits and capex, all of which were less than in 2019. It therefore seemed as if progress was being made on the expenditure side of the fiscal balance plan even amidst the pandemic.

However, the trend in spending has shifted over the last year and has deviated significantly from the fiscal balance plan. Whereas spending in 2020-21 was nearly flat and only 5% above the budgeted levels (which were set before COVID-19), in 2022 it rose by 12% y/y and was 22% above budget. The 2023 budget made clear that this was not just a one-off deviation, revising up the spending envelopes for 2023-24 by 18% compared with the projections that were included in the 2022 budget, although it did budget that spending would be slightly less than in 2022. However, there was no sign of a reduction in the first half of 2023, when expenditure was up by 18% y/y. Moreover, the Pre-Budget Statement, released in September 2023, estimates that 2023 spending will come in about 13% over budget and it also hiked projections for spending levels in 2024-25 by a similar amount. Whereas the 2023 budget had project surpluses in 2023-25, the new government projects see deficits averaging 2% of GDP through to 2026.

This uptick in expenditure could be seen as a familiar pro-cyclical response to higher oil prices. However, this is not the full story as the spending growth is partly due to inflation and partly due to an acceleration of efforts on Vision 2030 realisation programmes. The projections of declining expenditure that had previously been plotted out since 2019 were based on modest forecasts for nominal economic growth. However, non-oil GDP has been expanding rapidly and this is expected to continue, while strong medium-term oil prices will underpin oil GDP (barring the drop this year due to temporary production cuts). As a result of the rising GDP, spending is projected to decline in relative terms to average only 29% of GDP in 2024-26, which is not particularly high by historical standards, when expenditure averaged 35% of GDP over the last decade.

Despite the increase in expenditure, the Kingdom has received positive actions from rating agencies, who closely watch fiscal trends. In fact, the Kingdom received positive actions from all three rating agencies in 2023, with Standard & Poor’s upgrading to A, Fitch to A+ and Moody’s, which had maintained an A1 rating (equivalent to A+) since 2016, assigning a positive outlook that indicates the potential for an upgrade back to a double A rating. However, if oil prices were to weaken materially in the medium term then some of the higher spending could prove difficult to reverse and therefore would be cause for concern.

Vision 2030 - On track at the half-way mark

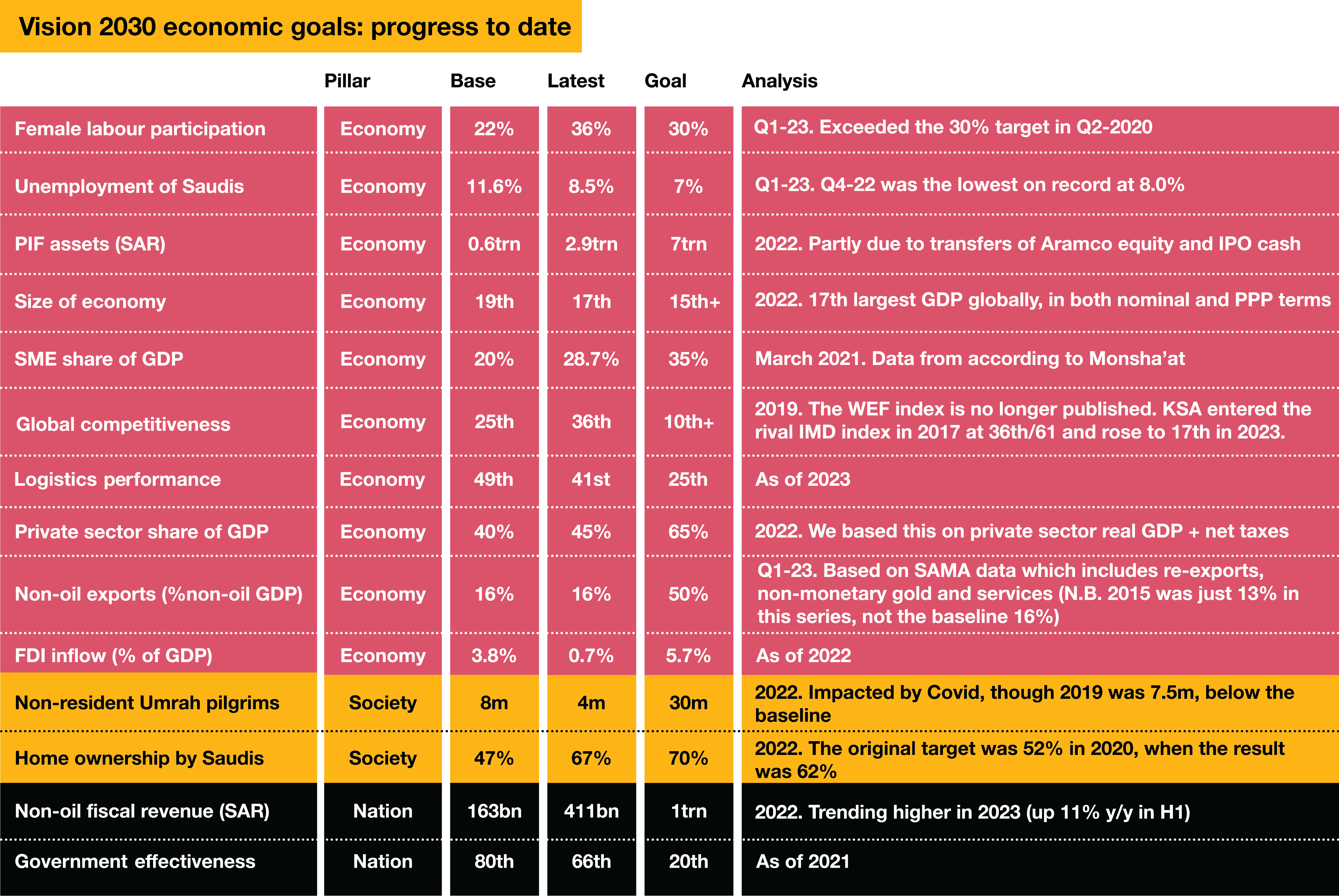

2023 is the half-way mark between the launch of Vision 2030 in 2016 and its target year. It is therefore a good time to try and take stock of performance relative to the ambitious goals of the development strategy. Given the breadth and scale of Vision 2030, a full assessment would require very lengthy analysis. We have limited our assessment to the economic aspects of the vision, specifically those that were quantified in the original Vision document. The 14 economic goals we assessed are shown in the table below and we discuss which have exceeded expectations, which are on track and which require more work to achieve their 2030 targets. We also include a brief review of progress on giga projects, which has become central to Vision 2030.

Areas of outstanding performance

It is significant that one of the 14 targets has already been far exceeded, that of female labour force participation amongst Saudi nationals. The baseline level, which generally means around 2015 or the most recent figure that was available when the Vision was drafted, was only 22%, one of the lowest in the world. The 2030 goal of 30% was already surpassed in 2020 and by Q2 2023 it had risen further to 35%. This has been supported by social liberalisation, including permitting women to drive in 2018, and alongside Saudisation policies, there's been a proactive shift among nationals to embrace a broader spectrum of roles, including customer-facing retail and service positions. The boost to household incomes from working women has contributed to rising consumption and supported broader economic growth. It is significant that even with the influx of Saudi women into the labour force, unemployment has also been declining, hitting 8.0% in Q4 2022, the lowest on record, down from the baseline of 11.6% and well on the way towards the 2030 target of 7% (it was only slightly higher at 8.3% in the latest reading, for Q2 2023).

Another area of strong performance is the expansion of home ownership. This stood at just 47% in the baseline but had risen to 67% by 2022. This is higher than the US and France (excluding expatriates). This is the result of a range of initiatives to boost the supply of affordable homes, such as a tax on undeveloped urban land, and improved access to financing options, such as through the Saudi Real Estate Refinance Company, a PIF subsidiary launched in 2017 similar to the US’s Freddie Mac. The 2030 target of 70% is nearly achieved (to be precise, the Vision 2030 document only published the 2020 target of 52%, which was far exceeded, although the 2030 target appears to have existed internally).

Non-oil fiscal revenue has reached two and a half times the baseline by 2022 and is on track to rise further in 2023. The major driver of this increase is VAT, introduced in 2018 at 5%, which tripled to 15% in 2020. This is still relatively modest by international standards but it is unlikely to increase further and, indeed, the government has indicated that it could be reduced at some point. Other revenue has come as a result of growth in the economy, boosting existing tax revenues, as well as several smaller measures such as the expat levy, the tax on idle land and excise duties on tobacco and sugary drinks. There is no obvious new source of tax revenue that could match the surge that came from VAT, unless personal income tax (which Oman is contemplating) becomes politically feasible. Instead, achieving the ambitious target of SAR1trn non-oil revenue (more than average annual oil revenue achieved since the start of Vision 2030), and equivalent to another increase of 2.5 times on the 2022 level, would probably require a surge in investment dividends.

That ties in neatly with a fifth area of strong progress, growing the size of the Public Investment Fund (PIF). The transformation of the sovereign wealth fund from a sleepy holding company to an aggressive international deal maker and manager of giga projects is one of the biggest changes in the Kingdom since the start of Vision 2030. The idea of increasing its assets more than 10-fold from the baseline seemed like quite an extreme target, but by the end of 2022 it had already increased by nearly 5-fold to SAR2.9 trn. This is partly a result of the transfer of state assets, including a 4% stake in Aramco in 2022 and proceeds from the sale of 1.7% in the 2019 IPO. A further 4% has been transferred in 2023. However, it is also the result of an increase in valuation in its Saudi corporate holdings, with the Tadawul being one of the strongest performing global markets recently, as well as some savvy foreign investments such as Lucid Group. If PIF could reach SAR7trn by 2030 and pay a 5% dividend into the budget then that could put the non-oil fiscal revenue goal in reach.

Vision 2030 economic goals: progress to date

Areas of good performance

Saudi GDP exceeded $1trn for the first time in 2022 and, even with lower oil exports, is expected to remain above $1trn in 2023, with the IMF forecasting growth to $1.3trn by 2028. As a result, it has risen up the rankings of global economies to 17th largest by size of GDP in 2022, at both market-exchange rates and purchasing power parity (PPP). This is halfway towards the 2030 goal of 15th.

A more pertinent measure of success is probably the expansion of small and medium enterprises (SMEs), which are the backbone of most economies and the drivers of employment. In the OECD, SMEs contribute over 50% of GDP but it is much lower in GCC states where the state and big family conglomerates dominate. The data on this topic is sporadic and probably of poor quality given sampling difficulties. The baseline figure was 21% and Monsha’at (the General Authority for SMEs) stated in early 2021 that it had risen to 28.7%; although that was during the pandemic it may not be representative of the current share. There are efforts underway to support the sector, including through the establishment of SME Bank, which has provided SAR20bn in funding since its launch in 2020 to SMEs.

The private sector’s share (including net taxes) rose from 40% in the baseline to 45% in 2022. This is solid progress but the goal of 65% by 2030 was always ambitious. One factor that might impede progress in this area is the continued expansion of the government PIF into many areas of the economy, which has launched nearly 100 subsidiary companies in areas from tourism to recycling that could crowd out the private sector.

The GCC countries closely track their performance on global indices. Vision 2030 includes targets related to the World Economic Forum’s Global Competitiveness report, the World Bank’s Logistics Performance Index and the World Bank’s Government Effectiveness indicator. Performance on the latter two show improvements, with KSA moving up eight places to 41st in logistics performance and advancing 14 spots to 66th in government effectiveness. Further progress is needed to achieve the Vision 2030 targets of 25th and 20th, respectively.

The competitiveness measure is more difficult to gauge because the report was discontinued in 2020 and changes in methodology in prior years saw Saudi Arabia decline from the baseline rank of 25th in 2016 to 36th/141 in the final report in 2019. However, since 2017 the Kingdom has been included in a similar assessment of the business environment, the IMD World Competitiveness Yearbook. It entered the index at 37th/61 and has been one of the strongest improvers in recent years, rising to 17th/64 in 2023. This indicates strong progress and a top 10 ranking could be achievable by 2030—the UAE is currently 10th and Qatar is 12th.

Areas that are working towards the target

Although non-oil exports (including re-exports, non-monetary gold and services) were only 17% of non-oil GDP in Q2 2023, only slightly above the baseline, this was partly because of the strong growth in the denominator, with non-oil GDP nearly doubling since 2015, obscuring the fact that non-oil exports have grown significantly in absolute terms. The 2030 target of 50% is nevertheless ambitious given its current performance. However, there are good prospects of increased goods exports in many areas as a result of investments in new petrochemical facilities, mining and manufacturing as well as services exports, particularly tourism.

Growth in exports also depends on an uptick in investment, particularly foreign investment. FDI totalled 0.7% of GDP in 2022 and averaged 0.9% in 2016-22. There is room for improvement as this is well below the 2030 target of 5.7% and even below the reported baseline of 3.8%. By contrast, Oman, UAE and Bahrain each averaged over 3% of GDP in FDI during that period.

The reasons for the modest FDI figures are not immediately evident, especially considering the noticeable advancements in the Saudi economy and business climate. However, leading indicators from the Ministry of Investment, such as the number of investment licences signed, coupled with the momentum from the Regional Headquarters program, mean that we can expect to see an uptick in investment levels in the near future. Key projects under development, such as the Lucid Group and Ceer electric vehicle plants in King Abdullah Economic City, should boost both FDI and non-oil exports.

Finally, religious tourism has witnessed some challenges. The number of Umrah pilgrims in 2022 was only 4m, half the baseline level. COVID-19 was of course a factor here, although there had been no significant growth in 2016-2019. However, early indications in 2023 suggest a very solid recovery in pilgrimage, for both Umrah and Hajj, which involved over 1.5m visiting pilgrims, double 2022 and back to pre-COVID-19 levels. The growth in facilities to house pilgrims and the increased frequency in flights, which will be further expanded when the launch of Riyadh Air frees up Saudi capacity to Jeddah, mean that significant growth is expected in the coming years towards the Vision 2030 target. Vision 2030 did not set targets for secular tourism, which barely existed in 2016. However, social and visa liberalisation mean that a strong tourist market has been developing in the aftermath of COVID-19, in addition to the core pilgrimage sector. Saudi Arabia is investing in many segments of the leisure and hospitality sector, ranging from hosting sporting events to conferences, both for the domestic market and to attract tourists. The Asian Winter Games will be hosted in Trojana in 2029 and Saudi Arabia has designs on hosting major global events in the future, including bidding for the 2034 FIFA World Cup.

Giga projects advance

PIF’s giga projects were largely conceived after Vision 2030 but have come to be seen as nearly synonymous with the strategy. These include the Red Sea Global (a merger of the Amaala and Red Sea tourism projects), the Qiddiya entertainment city outside Riyadh and the Diriyah Gate heritage development. These projects have made significant progress in the last few years, moving from the conceptual phase to construction. The dominant giga project, much larger than all the others combined, is NEOM. It has attracted the most interest, given its scale and unique concepts. Any lingering doubts that NEOM is serious are being extinguished as significant earthworks progress across the northwestern corner of the Kingdom. To date, the bulk of investment in NEOM has come from PIF, but private investments are expected to play a leading role as its physical infrastructure and regulatory framework matures.

Beyond Vision 2030

Midway through the Vision 2030 implementation, strong performance has been achieved against many of the economic goals, as detailed above. There is good reason to expect progress on the others during the remaining seven years and even if some of the targets might have been overly ambitious on this time scale, they may be achievable longer term.

Indeed, the true impact of the Vision will play out well beyond 2030 to be realised as the reforms and diversification achieved sets the foundation for future development. The giga projects in particular are very long-term endeavours. In 2030, the first residents of the Line are likely to be getting settled, but the real growth will happen in subsequent years, with a target of 9 million by 2045. It is likely that a new medium-term vision, maybe targeting 2050, will be developed to take the Kingdom into the next stage of its development.

Contact us

Richard Boxshall

Global Economics Leader and Middle East Chief Economist, PwC Middle East

Tel: +971 (0)4 304 3100