Middle East shoppers have retained many of the habits and attitudes that were embedded during the global health crisis. They favour retailers who provide efficient delivery, both in-store and online, while they are willing to pay more for locally made products.

At the same time, the region’s consumers are increasingly choosy and agile. Middle East retailers are dealing with higher costs and supply chain issues, and their challenge is to retain the loyalty of digitally savvy shoppers who can - and often do - switch easily between channels, outlets or brands. Part of the solution is to recognise that Middle East consumer choices are increasingly influenced by environmental, social and governance (ESG) factors.

44% of shoppers in the region report that the health crisis has encouraged them to buy from local retailers.

While 60% say they are shopping to some/great extent from outlets with an efficient delivery or collection service. Cost and convenience are not the only factors driving this trend.

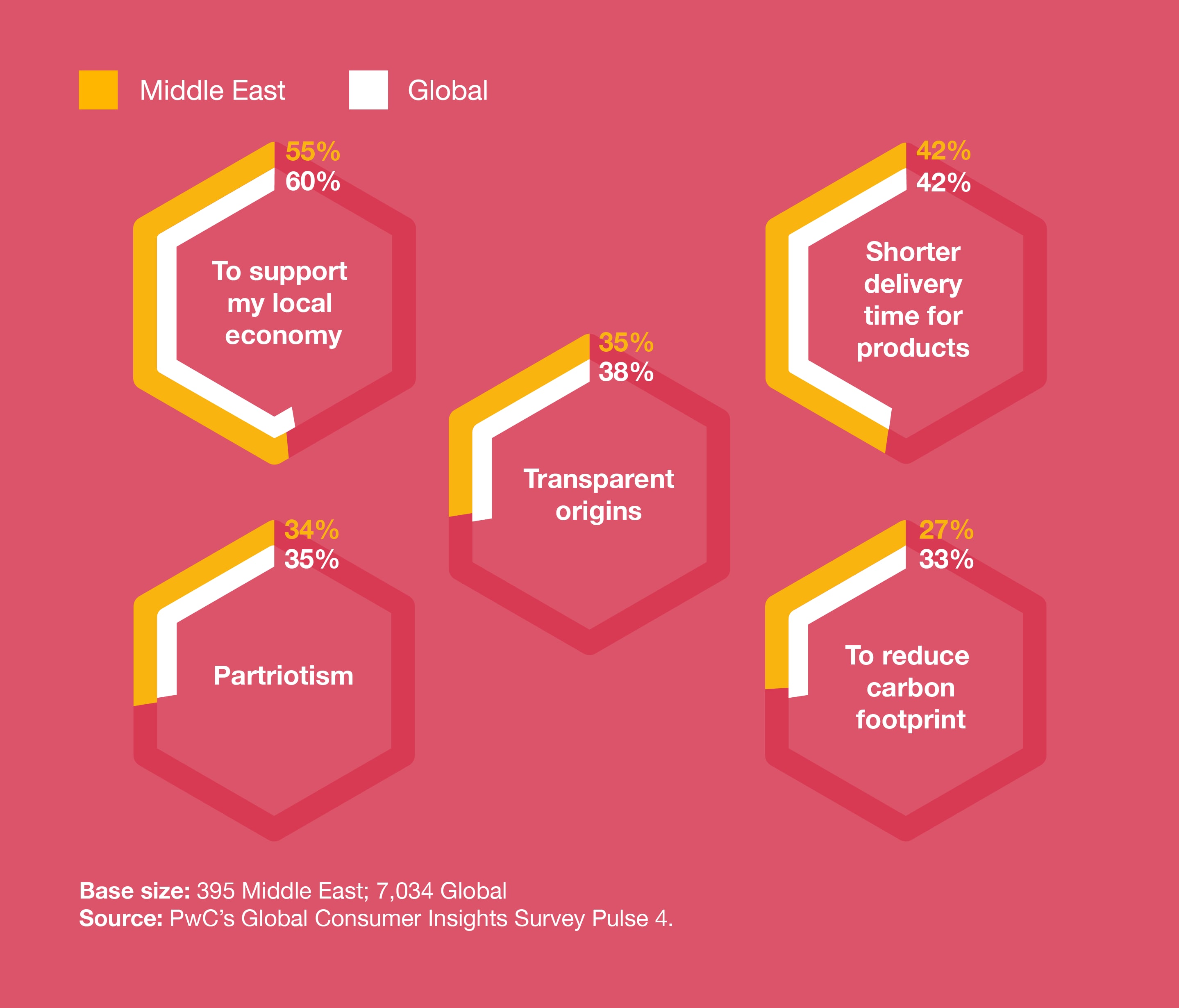

In line with the global survey, 83% of regional respondents are willing, in varying degrees, to pay more than the average price for a purchase that is made or sourced locally, such as produce from a farmer’s market, and 80% will pay more for a product with a traceable or transparent origin. Local economic support and patriotism are other reasons why Middle East shoppers are more inclined to pay a higher price for locally sourced or produced goods.

Consumer’s willingness to pay more to a great extent for locally sourced products

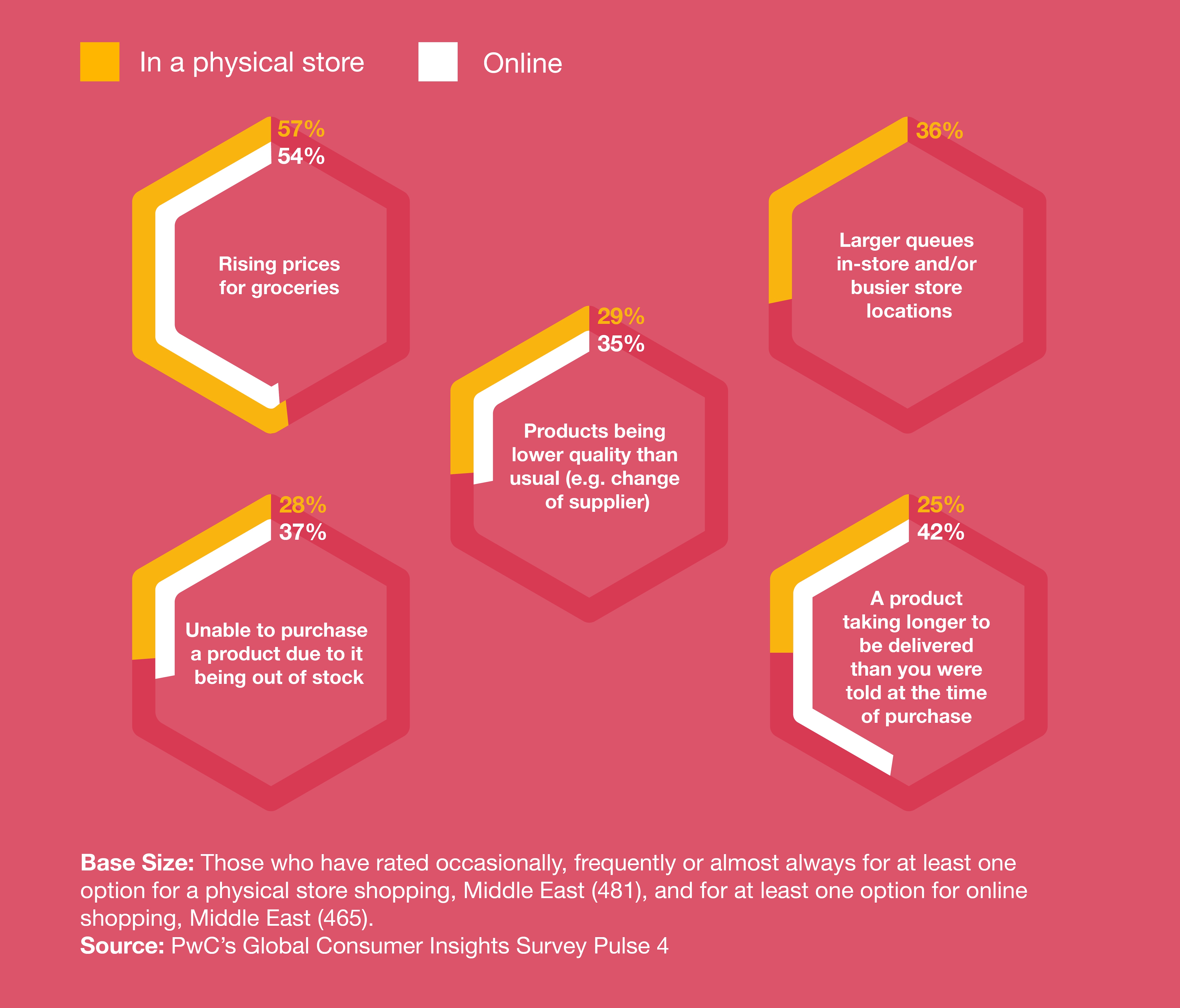

Rising prices and delayed deliveries remain a familiar experience for shoppers throughout the region.

To take one example, 48% of Middle East consumers say grocery prices at physical stores have almost always or frequently increased since their last visit during the previous three months. 57% say the increasing cost of daily food purchases is one of the top three issues affecting their physical shopping experience, followed by larger queues and busier stores (36%) and lower quality products (29%).

The same concerns are evident with online shopping, where 43% of Middle East consumers report that grocery prices have risen almost always or frequently in recent months, in line with the global survey average. Rising prices for online grocery purchases was cited as the most significant “top three” issue undermining their online shopping experience, followed by delays in product delivery (42%) and a product being out of stock (37%).

Which of these issues is having the greatest impact on you? Ranked 1 to 3

Middle East consumers are spreading their wings to a far greater degree than the global survey average.

When they consider their spending decisions over the next six months, Middle East consumers continue to reflect the increased sense of freedom. For example, 39% expect to spend more on travel. In parallel to the growing appeal of travel, the health crisis has also reinforced the trend towards pursuing more leisure and recreation activities at home. For instance, 33% of Middle East consumers say they are still planning to increase their expenditure on home entertainment in the next six months, despite the threat from the health crisis subsiding. Similarly, 36% expect to spend more on takeaway food. Meanwhile, the proportion of respondents who think they will spend more in restaurants has declined slightly from 43% in Pulse 3, when fear of catching the health crisis was higher, to 36% in Pulse 4.

Yet, Middle East consumers remain weighed down by familiar everyday financial worries that afflict the rest of the global survey – notably the spectre of inflation. 49% (vs 47% globally) of Middle East respondents expect to spend more on groceries during the next six months, a proportion that has barely changed since the first the health crisis wave in 2020.

Q: Thinking about your spending over the next 6 months, to the best of your ability, please describe your expectations on spending across the following categories. (% increase in spend)?

Q: In the last 6 months, which of the following activities have you participated in via virtual reality?

One development worth noting is the emergence of a minority (17% vs 16% globally) of early adopters who say they have used a virtual reality headset in the last six months – for example, to watch a movie or TV show or to play an online game. We expect this proportion to grow over the next year, given how younger Middle East consumers are increasingly connecting with the latest virtual reality (VR) and augmented reality (AR) technologies, including most notably the metaverse.

The region’s shoppers are often ahead of the rest of the global survey when considering ESG factors before buying a product or service.

31% say they would always recommend a company or brand with a good environmental record to others, compared with 18% globally, and 27% trust a company or brand more for the same reason, almost double the survey average.

The same gap between Middle East consumers and their global counterparts is evident when considering the social factors influencing their shopping behaviour. 30% of the regional survey would always recommend a socially responsible company or brand, compared with 20% globally, and 31% (vs 19% globally) would always trust the same company or brand more.

Influence of company consideration of ESG on Consumer Behaviour

The protection of personal data remains the most important reason for trusting a brand according to 63% of Middle East consumers,

but the brand is trusted more if it offers new, enjoyable and innovative products and services. Regional consumers are increasingly protective of their personal data, constraining the ability of retailers to use data analytics to find out more about their individual needs and shopping habits. Meanwhile, 51% of Middle East respondents are open to sharing their data in exchange for a better, personalised customer experience, and 54% are prepared to share their data provided if it is not shared with or sold to third parties. There is little difference between the proportion of Middle East shoppers who trust a brand more if it always meets their expectations (58%) and the overall survey average (53%).

Q: Thinking about a brand that consumers regularly buy products/services from, they trust the brand to a great extent if it.

“Certain consumer habits have been permanently reshaped by the health crisis, however, some pre-the health crisis trends are emerging to influence consumers’ shopping decisions. Our latest findings explore that despite the Middle East shoppers’ price-sensitivity, they don’t mind paying more if the products are from recycled, sustainable or eco-friendly materials.”

Consumer attitudes and behaviour across the Middle East have been shaped by the health crisis disruption of the past two years, but some pre-the health crisis trends are also still shaping their decisions. Current attempts by Middle East retailers to resolve supply chain challenges are building on their pre-the health crisis efforts to leverage new technologies to deliver products more rapidly and efficiently. Meanwhile, shoppers are rightly worried about price rises.

The health crisis has undoubtedly permanently reshaped consumer behaviour, driven by younger, digital-first and socially aware shoppers. Trust matters to this rising generation. Yet brand loyalty for them is inspired by much more than good quality, affordable prices and reliable service. ESG considerations are also critical to their purchasing decisions – an insight which retailers should not overlook as the Middle East’s consumer market enters a new post-the health crisis era.

About the survey

The Pulse 4 Middle East findings for PwC’s latest global consumer insights survey include responses from 507 consumers in Egypt, Saudi Arabia and the UAE, split evenly between men and women. 75% of the sample are in the 18-41 age group, reflecting the region’s young demographic profile, and around 70% are in employment. 46% say they have a hybrid working pattern and can be based in any location, indicating that the rise of remote working during the health crisis is here to stay.

This report references the Middle East findings of the following surveys:

Where we’ve included data from previous surveys, the base sizes are listed below the graph.

Contact us

Partner, Deals Strategy & Operations, Consumer Markets; Culture, Media & Entertainment, PwC Middle East

Tel: +971 56 682 0528