GCC Capital Markets Watch - H2 2020

Top 3 GCC IPOs in 2020 by proceeds

Top 3 GCC sectors for 2020 IPOs

Top 3 global IPOs in 2020 by proceeds

2020 initiatives

During the year, initiatives were taken in the Kingdom of Saudi Arabia and United Arab Emirates to facilitate equity capital market activities on their respective stock exchanges:

- Tadawul launched its first Derivative Market in Q3 to gain access to a broader spectrum of local and international investors.

- Saudi Arabia’s Capital Market Authority approved the direct listing of Saudi White Cement Company on the Nomu Parallel Market, enabling Tadawul to become the first GCC exchange to allow direct listings, i.e. listings of shares without an offering, with the advantage of less time, cost and effort for entrants.

- Nasdaq Dubai launched a Growth Market aimed at small and medium-sized companies. It has more relaxed requirements compared to the main board, providing more flexible options to raise capital through IPO.

- Nasdaq Dubai also signed a cooperation agreement with Hong Kong SAR based Zhongtai Financial International and Beijing Tian Tai Law Firm to encourage and support Chinese companies to list on the exchange.

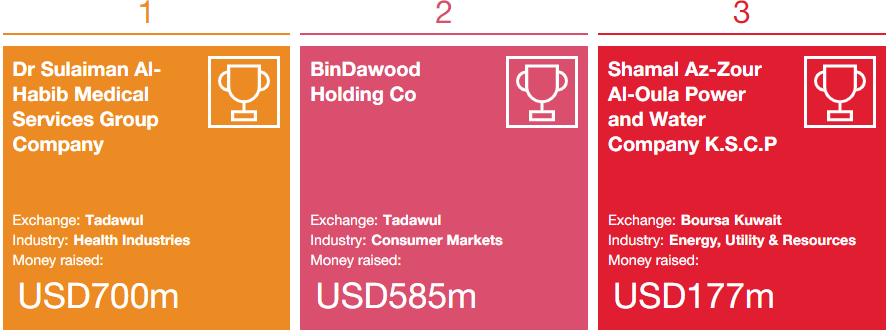

It is encouraging to see some GCC IPO activities after a pause in Q2. In the past, Q3s had typically been the quiet quarter. Q3 2020, however, had benefited from the buildup of a backlog over Q2 2020 driven by global disruptions, resulting in 3 IPOs across two GCC countries, raising USD325m compared to USD93m in Q3 2019, an increase of 249%. Two of these IPOs were on the Boursa Kuwait: Boursa Kuwait Securities Company (K.P.S.C.) raised USD32m whilst Shamal Az-Zour Al-Oula Power and Water Company (K.S.C.P) raised USD177m. The third IPO was listed on Tadawul in the Kingdom of Saudi Arabia: Amlak International for Real Estate Finance Co. raised USD116m.

During Q3, 2020 there was also a takeover by Oman Arab Bank of Alizz Islamic Bank, which resulted in a delisting of the target and a relisting of the enlarged group on Oman's Muscat Securities Market.

Q4 2020 experienced only 1 IPO on Tadawul with proceeds of USD585m compared to 4 IPOs with proceeds of USD26bn across multiple GCC stock markets in Q4 2019, including the USD25.6bn IPO of Saudi Aramco. Excluding the impact of the IPO of Saudi Aramco, the proceeds raised in Q4 2020 were in line with the prior year.

In UAE, Abu Dhabi Securities Exchange’s Second Market - Parallel was a popular choice during H2 with four listings raising proceeds totalling USD90m. The Second Market - Parallel allows investors to trade securities of private companies.

As GCC economies are dependent on oil revenue, as expected, reduction in oil price prompted sovereign treasurers to inject funds into the local economies through debt financing resulting in 6 sovereign issuances in the second half of the year from the Kingdom of Saudi Arabia, the Emirate of Abu Dhabi, the Emirate of Dubai, the Emirate of Sharjah, the Kingdom of Bahrain and the Sultanate of Oman. The Kingdom of Saudi Arabia issued USD10bn worth of sukuks and the Emirate of Abu Dhabi issued a bond worth USD5bn. The Department of Finance (DOF) representing the Government of Dubai, listed a 10-year Islamic Sukuk worth USD1bn at a coupon rate of 2.76% and thirty-year government bonds of USD1bn at coupon rate of 4%.

This period also witnessed some sizable corporate issuances including the USD1.5bn sukuk by DP World in July 2020. This represents the largest outstanding emerging markets US dollar corporate subordinated hybrid, the largest hybrid Sukuk offering, and is DP World’s inaugural perpetual issuance. DP World's debt listings now total over USD10bn on Nasdaq Dubai. In addition, China Construction Bank listed two green bonds on Nasdaq Dubai totalling USD1.2bn to support its efforts to combat climate change. Dubai Islamic Bank issued a USD1bn Additional Tier 1 (“AT1”) Sukuk on Nasdaq Dubai at a yield of 4.625%, the lowest yield ever for a bank on an AT1 sukuk.

GCC equity markets performance by cumulative total return since 1 January 2019

Source: Eikon (Thomson Reuter), PwC Analysis

Share price performance of 2018, 2019 & 2020 GCC IPOs* by sector, relative to the respective all share index, from the IPO date to 31 December 2020

Source: Eikon (Thomson Reuter), PwC Analysis

* The IPOs of Integrated Holding Co KCSC, National Building and Marketing, Al Nefaie Umm Alqura REIT, Al Moammar Information System Company and Sprinkle Holding BSC have been excluded due to insufficient data.

** The increase in the Financial Services sector is mainly contributed by an increase of 997% in the share price of Boursa Kuwait Securities Company (K.P.S.C.). If Boursa Kuwait Securities Company (K.P.S.C.) is excluded, the increase would be 11%.

Global IPO performance in H2 2020

Top 3 IPOS in H2 2020 by proceeds

- Exchange

- NYSE

- Pricing date

- 22 July 2020

- Money raised

- USD4.0bn

- Exchange

- HKEX

- Pricing date

- 1 Dec 2020

- Money raised

- USD4.0bn

- Exchange

- NYSE

- Pricing date

- 15 Sept 2020

- Money raised

- USD3.9bn

H2 2020 saw a significant increase in IPO activity across all regions as compared to H1 2020, with 1,009 IPOs raising USD251.3bn in the half year (H1 2020: 406 IPOs; USD80bn).The increase in the IPOs is partially attributable to SPAC IPOs that raised USD38.2bn in Q4 2020 alone.

Global further offering (FO) activity also increased by 16.9% in H2 to USD395.8bn when compared to H1 2020 (USD338.5bn). The healthcare sector was the most active sector in 2020 with 911 transactions raising USD120.5bn.

Vaccination programs around the world should underpin a global economic recovery in 2021. This will build from a position where equity markets have been benefiting from an extended period of low interest rates, low inflation and government stimulus, particularly in Europe and the US. However, the timing of the expected positive impact on economies, corporate earnings and capital markets will depend on the progress of vaccination programs across the globe.

With strong momentum building in H2 2020, there is a very substantial pipeline of companies looking to IPO in 2021 in favourable conditions. However, the implications of the change in the US political leadership, Brexit and, more generally, unprecedented government borrowing in response to recent global events add to the uncertainties.

Global IPO activity

Top countries by % of total IPO proceeds raised in 2020

Liquidity is key - debt vs equity funding

Many central banks have lowered interest rates to record lows to restart economies, which may make debt funding an attractive option for some companies. However, management should also consider how their credit ratings might have changed due to recent economic pressures on their businesses which could offset the cost reduction offered by such central banks initiatives.

With the recent approval of a number of vaccines by countries globally and the World Health Organisation and the rollout of vaccination programs worldwide, equity funding could once again be a feasible option in the near future.

Be super ready

Liquidity understandably is limited in the market during the current uncertain times and companies which are interested in seeking financing from the market should get themselves ready, so that they will be able to capture the available liquidity before it is taken, in the ever narrowing market window. This requires having a supportable financial track record that complies with regulatory requirements and recent credit rating, culminating in having a prospectus and investor presentation on standby.

Today determines tomorrow

Companies interested in equity funding in the longer term shouldn’t sit idle either. With potential down time because of reduced operating activities, management could make use of the precious time in preparing for a future IPO. Because of the regulatory requirements, which vary depending on your chosen market, it typically takes 6-12 months for a private company to get ready for an IPO – a process which involves looking at how your business has performed over the last 3 years, its outlook and its corporate governance.

Equity story

Ensuring all the regulatory requirements are met is a given in all IPOs. One key aspect to also consider in an IPO is the equity story - a company’s appeal to potential investors. In the post COVID-19 era, equity story will need to be stronger than ever. Executives need to ensure the company has a solid track record and a future-proof strategy that will resonate with its target investors. Some of the major themes apparent in equity transactions globally in 2020 include a strong balance sheet, efficient capital structure and environmental, social and governance (ESG) premium.

How PwC can help you

At PwC, we understand that good preparation is essential to a successful IPO and debt issuance. We have experience in a wide range of international, regional and domestic IPOs and debt issuances, and can provide expert guidance from initial planning, through to execution and beyond.

IPO and debt preparation

Our IPO and debt Readiness Assessment is an early stage diagnostic review of the critical areas needed for a successful issuance. We highlight where current processes, procedures, structures and practices fall short of the requirements for a company whose securities are to be publicly traded and provide recommendations on how to address these gaps. In the current environment, it is equally important to address emerging risks that may have accounting and financial reporting implications in most companies, including, among others, impairment of assets, changes to lease terms, and government support. Our assessment can be tailored to include these aspects as well as broader areas such as business continuity and contingency planning.

IPO and debt execution

We work with issuers and their advisors to provide IPO and debt advisory and assurance services. This may include working capital reporting, financial due diligence, financial positions and prospects procedures assessment, assistance with MD&A drafting in relation to a prospectus, comfort letters and project management.

Contact us

Haitham Aljabry

Finance & Accounting Consulting, Partner, PwC Middle East

Tel: +966 54 732 2225