Five GCC economic themes to watch in 2026

Trade, supply chains, AI, skills and fiscal resilience will define the GCC’s economic trajectory, anchoring long-term, sustainable growth

As the GCC enters 2026, economic policy is increasingly focused on strengthening resilience across trade and investment, supply chains, technology adoption, labour markets and public finances. These priorities frame the forces shaping the region’s economic outlook for the year ahead.

The past year saw continued progress on diversification and structural reform. Governments advanced trade negotiations, expanded investment in AI and digital infrastructure and pushed ahead with sector-level reforms in logistics, manufacturing and energy. At the same time, external conditions became more challenging, with a softer oil price outlook, tighter global financial conditions and heightened geopolitical competition across trade, technology and supply chains.

Entering 2026, these dynamics are sharpening the focus on resilience rather than expansion alone. Governments are expected to broaden trade and investment relationships, secure access to critical minerals and industrial inputs, and accelerate AI adoption in priority sectors as infrastructure constraints ease. Fiscal policy is adjusting to lower hydrocarbon revenues through expenditure prioritisation, asset monetisation, liability management and efforts to strengthen non-oil revenue frameworks.

Collectively, these developments suggest that 2026 will build on the momentum of 2025, and deepening economic resilience and diversification through five defining themes.

1. Building broader and more diverse trade bridges

As geopolitical tensions continue and US–China relations remain strained, global trade dynamics are evolving. The US has taken a more transactional approach to trade and industrial policy, prompting economies that depend on free trade to reassess their strategies. For the GCC, this reinforces the need to broaden trading relationships, secure access to growth markets and strengthen resilience in an increasingly fragmented global system.

GCC countries are expected to expand their network of partners in 2026, building on the momentum established in 2025. Negotiations advanced with China, New Zealand, the EU, Mercosur and Japan, while talks with the UK have moved into final drafting and could reach conclusion in 2026.1 Engagements with Malaysia and Vietnam, as well as a joint feasibility process with the Association of Southeast Asian Nations (ASEAN), signal a continued push toward a more diverse and balanced portfolio of economic ties.2

Participation in emerging trade corridors is also likely to increase. The ASEAN-GCC-China Summit in 2025 highlighted the region’s growing role in the Asian economic landscape. Further progress on the India–Middle East–Europe Economic Corridor (IMEC) is anticipated as Europe seeks new partners and the GCC looks to leverage its geographic position in east-west trade.3

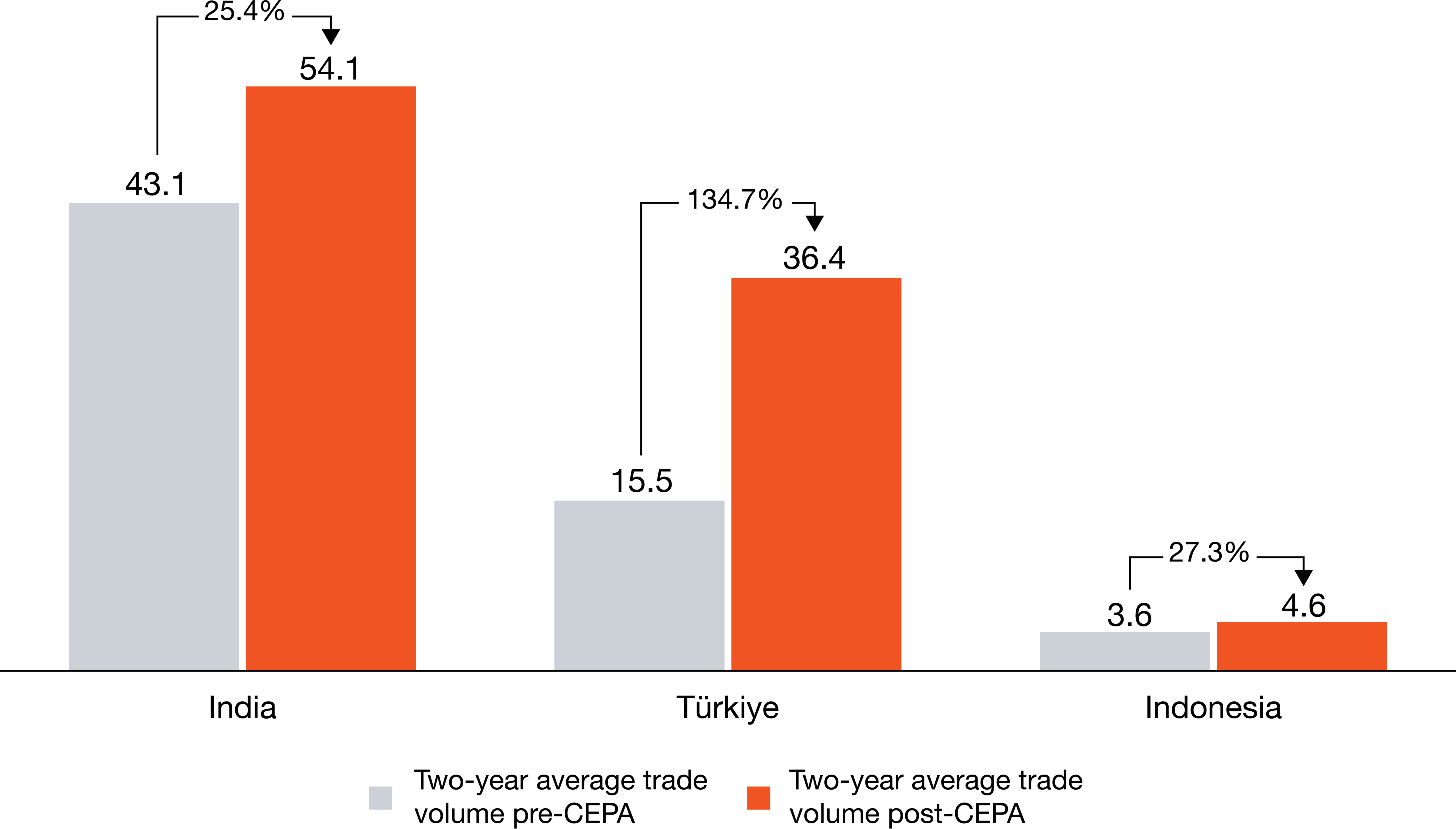

Bilateral agreements are expanding in parallel. The UAE broadened its Comprehensive Economic Partnership Agreement (CEPA) programme to more than two dozen partners across Asia, Africa and Europe. Reported increases in trade flows, including double-digit growth with India, Turkiye and Indonesia (see Figure1), have encouraged other GCC economies to pursue similar approaches.4 Oman’s agreement with India is nearing completion, and Qatar has indicated interest in advancing its own bilateral arrangements.56

Figure 1: UAE bilateral trade with select activated CEPA partners (USD Bn)

Source: Trade Map, UNCTAD

Note: excludes 2020, annual data

This trajectory is expected to accelerate in 2026. CEPAs allow countries to align trade policy with domestic economic priorities and support deeper cooperation in fields such as digital trade, IP protection, green standards and harmonised rules of origin. These elements create the basis for more integrated and sophisticated partnerships.

Commercial diplomacy also gained pace in 2025. High-profile engagements resulted in major investment commitments from Qatar, the UAE and Saudi Arabia toward US projects and procurement programmes.7 These arrangements will also help GCC countries enter countries with low-product market fit, such as in Africa, where Saudi Arabia pledged US$41bn in investments and trade.8

Governments across the GCC are also likely to use integrated trade and investment packages more actively as part of “commercially-focused” diplomacy as they compete for capital, technology, and market access. Investment-linked partnerships are set to become a more routine feature of international economic engagement.

Taken together, these shifts reinforce the region’s trajectory toward becoming a central hub for east–west and south–south trade.

2. Securing critical minerals supply chains

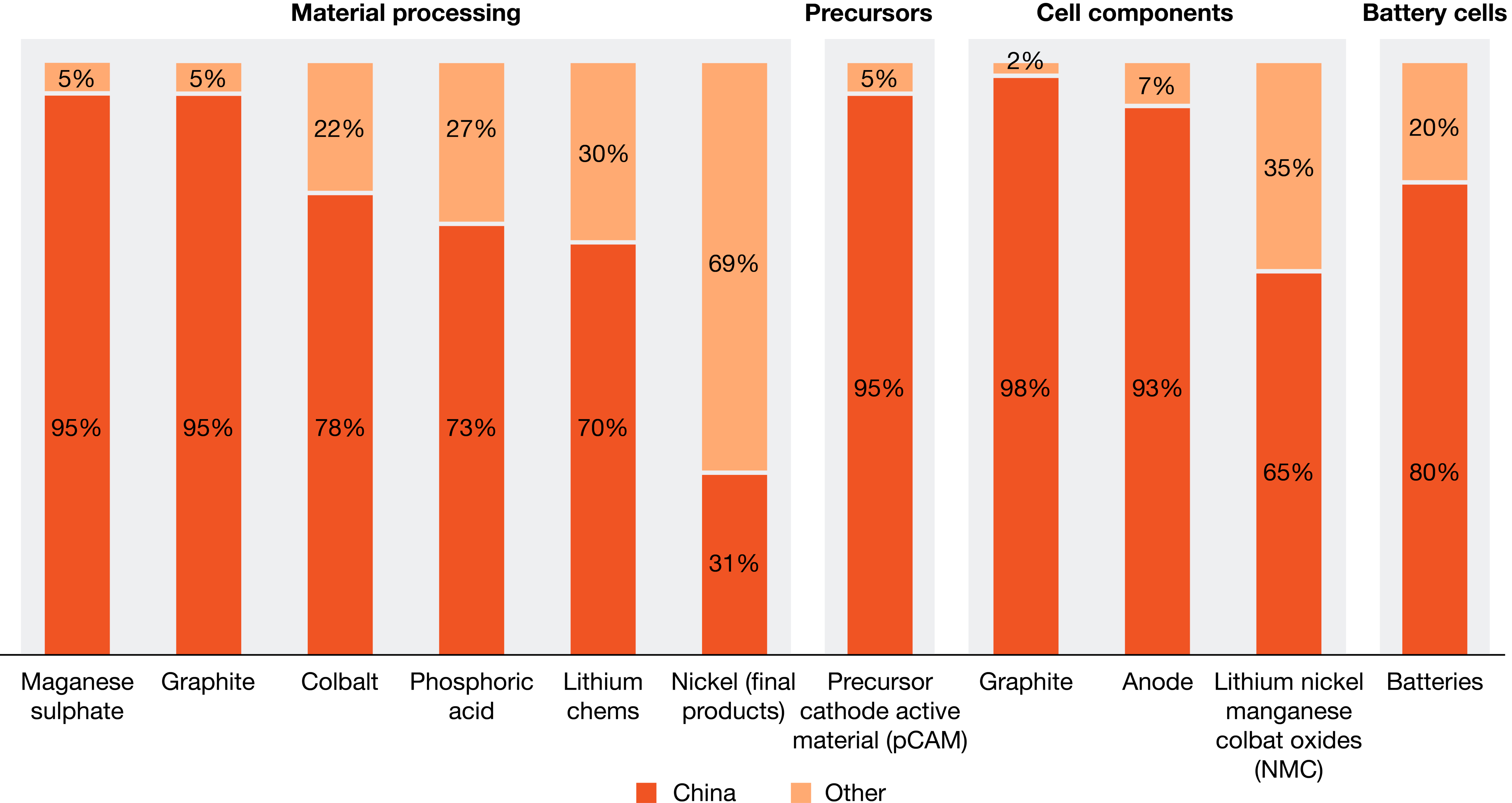

Global demand for critical minerals continues to rise as energy transitions and advanced manufacturing accelerate. These materials, essential for batteries, semiconductors, and renewable technologies, place new pressure on supply chains that are already concentrated and vulnerable to geopolitical shifts (see Figure 2). Processing capacity for several key minerals remains dominated by China, particularly in rare earths processing and refining, prompting governments and industries worldwide to seek more resilient and diversified sources of supply.

Figure 2: Global midstream and downstream battery supply chain, 2024

Source: IAE

For the GCC, securing access to these materials is becoming a strategic priority as the region advances its industrial and manufacturing ambitions. Saudi Arabia is positioning itself as the region’s anchor for mining and critical minerals. Ma’aden, the Kingdom’s flagship mining company, is central to this effort. It has expanded its portfolio to include phosphate, aluminium, copper and emerging critical minerals, supported by long-term investment commitments and partnerships with global players. Its aluminium and bauxite joint venture with Alcoa, along with its exploration investments with Ivanhoe Electric, indicate a sustained effort to strengthen both upstream resources and midstream processing.9 These steps support national objectives to develop mining into a major economic pillar by 2035.

Private and state-linked investment vehicles are forming partnerships in Africa and Asia to secure upstream access to critical minerals. Examples include ADQ’s joint venture with Orion Resource Partners aims to build an investment platform, while QIA’s partnership with Ivanhoe Mines in southern Africa focuses on financing, acquisition opportunities, and potential downstream development.10

The region is also taking early steps to localise parts of the critical minerals value chain, moving beyond upstream access toward midstream processing and refining. Saudi Arabia has begun prioritising the development of commercial-scale processing zones for battery metals and rare earth elements, supported by incentives under the Kingdom’s mining investment law and industrial financing programmes. Ma’aden has outlined plans to explore refining capabilities for select critical minerals, to explore opportunities to establish a fully integrated, end-to-end rare earth supply chain in the Kingdom.11 In parallel, the UAE is advancing similar ambitions, with Abu Dhabi attracting early-stage investment interest in battery metals processing and value-added metals manufacturing linked to its industrial strategy. These efforts indicate a longer-term trend in which the GCC seeks not only to secure raw mineral supply, but also to build the refining and conversion capacity needed to participate more meaningfully in global critical mineral value chains.

By 2026, the region is expected to deepen upstream partnerships with African producers, expand early-stage domestic processing capacity, and enhance logistics capabilities to handle strategic materials. These developments point to a larger role for the GCC as an emerging connector between African mineral supply and global industrial demand.

3. Turning AI ambition into action

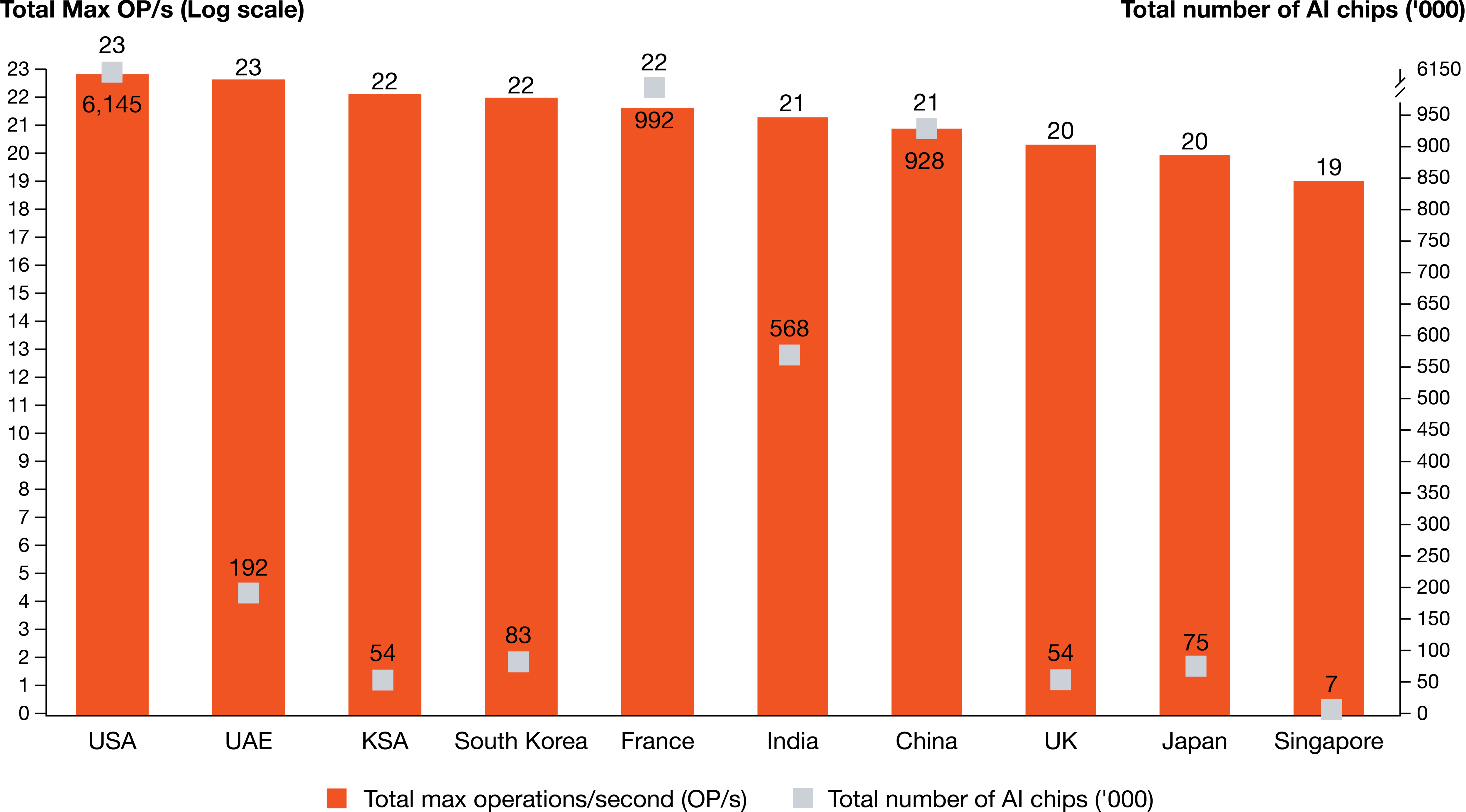

In 2025, global competition for compute power, skilled talent, and secure data environments intensified. These pressures exposed a regional compute bottleneck, with limited access to advanced graphic processing units (GPUs), critical for accelerating AI model training and insufficient sovereign cloud capacity for large-scale model training.12

Governments responded to this challenge with significant investments to expand computing capacity and partnerships to secure advanced chips. Efforts in the UAE and Saudi Arabia have paid off, as both countries now rank among the world’s leading countries for planned and active GPU clusters (see Figure 3), with substantial new capacity expected to come online in 2026. In the UAE, the first phase of Stargate UAE is expected to commence operations, supported by additional expansions from Khazna Data Centres that will provide larger GPU clusters and higher-density cloud regions.13 Saudi Arabia will advance the next stage of its national AI programme as HUMAIN begins constructing new data centre capacity and integrates NVIDIA’s Blackwell GPUs - the company’s most advanced chipset recently cleared for export by the US Department of Commerce.14 Qatar has launched Qai, a QIA company to develop and operate AI infrastructure domestically and abroad.15 Together, these developments will reduce reliance on overseas hosting and enable organisations to run high-compute workloads on in-country, government-approved AI infrastructure.

Figure 3: AI chips and computing power by country, based on active or planned GPU clusters as of 2025

Source: Epoch AI

With infrastructure gaps narrowing, 2026 is likely to see a shift from government-led to company-level investments. More predictable access to compute and domestic hosting options will make larger commercial rollouts feasible. Companies in the financial services, logistics, energy, transport, and retail sectors are expected to move from pilots to operational deployment, adopting sector-specific models, automation platforms , and AI-enabled customer services.

Regulatory clarity will be another catalyst in 2026. The current regulatory environment facilitates faster deployment, data-centre projects typically reach operations in approximately 18–24 months, versus around 36–72 months in the US where permitting and grid constraints can add multi-year delays.16 Looking ahead, Governments are expected to introduce more specific rules on how AI systems are built and assessed. These include clearer expectations around where training data comes from, how organisations classify and manage model risk, and the level of independent testing required for sensitive use cases such as finance or healthcare. Regulators are also likely to introduce structured processes for reporting incidents, resolving user complaints linked to automated decisions , and conducting periodic internal reviews of high-impact models. These measures will give companies a more predictable compliance environment and help unlock adoption in regulated sectors.

Data sovereignty will increasingly shape how governments and companies manage AI deployment. As regional cloud capacity matures, several GCC states are expected to expand localisation requirements for sensitive datasets and mandate that certain workloads - such as government services, health records, and financial data - run on domestic infrastructure. This will drive investment in national data lakes, secure training environments, and trusted data platforms, enabling AI development without cross-border data transfers.

Taken together, these trends indicate that 2026 will AI ambition to broad-based implementation, accelerating productivity gains and strengthening its competitiveness in the global AI landscape.

4. Managing workforce transitions in an AI-enabled economy

Across the GCC, productivity growth, as measured by total factor productivity (TFP), has weakened over the past decade (see Figure 4). TFP measures the impact on output from improvements in technology, management practices and workforce capabilities that allow economies to produce more, rather than simply adding more workers or capital. This contrasts with continued gains in advanced markets, and reflects the slower diffusion of new technologies, limited process innovation and skills gaps in fast-growing sectors. The scale of the AI shift gives the region an opportunity to reverse this trend through widespread AI adoption, raising efficiency gains and productivity growth.

Figure 4: Average annual change in total factor productivity (2015 – 2025)

Source: The Conference Board

As AI adoption accelerates, labour market policy is shifting from job creation to managing workforce transitions. Automation, generative tools and data-driven systems are expected to reshape roles across financial services, logistics, customer service, and government. In 2026, governments and employers will focus on equipping workers for emerging occupations rather than preserving legacy roles, particularly in sectors where AI-enabled productivity gains are expected to be most visible.

Short, modular training programmes will scale significantly. Micro credentials are likely to become a more formal part of national qualification systems, with greater standardisation and alignment to employer needs. Programmes in data analytics, cybersecurity, digital operations, and AI-assisted business processes will expand. This will be supported by partnerships between governments, major employers, and global technology firms – mirroring initiatives such as Saudi Arabia’s SDAIA Academy’s accelerated courses in data analytics, cybersecurity, and applied machine learning with partners such as Microsoft and IBM17 and Dubai Future Foundation’s One Million AI Prompters initiative.18

Workplace-based learning will grow in parallel. Firms are expected to adopt more apprenticeship-style pathways and structured on-the-job training to build practical digital capabilities. These programmes will support translation roles, i.e. employees who can integrate AI tools into workflows, redesign processes, and ensure safe and effective use in day-to-day operations.

Governments are likely to introduce targeted incentives for career transitions. These may include stipends for mid-career transitions, bridge programmes that help nationals move into higher value private sector roles, and pathways for expatriate professionals shifting into digital occupations. The emphasis will be on developing skills that support competitiveness rather than protecting existing job structures.

Public–private talent platforms will become more sophisticated. These platforms will integrate real-time labour market data, training outcomes, and employer demand to match workers with reskilling opportunities and new jobs. Early examples, such as Qatar’s Ouqoul platform that uses AI to generate consistent job descriptions and the UAE’s Emirati Smart Human Resource Platform19 will evolve into more data-rich tools in 2026 that guide national workforce planning and help direct reskilling investment.

New categories of work will expand, including AI model operators, quality reviewers, and risk and compliance specialists. These roles will be central to scaling AI safely across regulated sectors.

Together, these shifts suggest that 2026 will mark a decisive move toward active workforce-transition management, ensuring that AI-driven productivity gains translate into inclusive and sustainable growth.

5. Strengthening fiscal resilience in a lower oil price environment

Forecasters globally are predicting oil prices to average around US$55–60 per barrel in 2026, regional oil-producing economies will face tighter fiscal conditions, heightening the need for resilience.20 Lower hydrocarbon receipts will make expenditure discipline, revenue diversification, and private investment mobilisation more urgent, especially as large-scale national transformation programmes continue.

Privatisation and public-private partnerships (PPPs) will see renewed focus, with governments preparing to bring more assets to market and monetise state-owned enterprises in logistics, utilities, water and waste management, and non-strategic energy services. Saudi Arabia is set to advance transactions involving airports and desalination assets, while the UAE will likely continue monetising select DEWA- and AD Ports-linked assets.21 These initiatives aim to redirect public funds to higher-impact investments and attract private capital to transport and utilities.

Across the region, gross government debt relative to GDP largely remains below the average for advanced economies (see Figure 5). Countries are expected to increase borrowing, including sukuk and sustainability-linked bonds, to finance deficits and fund strategic investment. Recent credit rating upgrades for Saudi Arabia, Oman, and Kuwait will support market access. At the same time, public-private partnerships will remain key for delivering capital projects while limiting direct pressure on government balance sheets.

Figure 5: General gross government debt (% of GDP)

Source: IMF

Spending prioritisation and subsidy reforms will guide budgets. Governments will shift more expenditure towards projects with strong economic impact, such as digital infrastructure, logistics, industrial development, and energy transition, while reducing outlays in lower return areas. Energy and utility subsidies currently comprise a significant share of expenditure, and 2026 may see broader pricing reforms across utilities, with targeted support for lower income households.

Revenue diversification will progress. Some new tax measures may be introduced; however, governments will likely strengthen corporate tax and VAT frameworks, improve compliance, and expand the digital and cross-border transaction base.22 The UAE and Kuwait, having introduced domestic minimum top-up taxes, should begin generating more stable non-oil revenue.23

Overall, 2026 is set to be a pivotal year for fiscal rebalancing in the GCC. Success will hinge on mobilising private investment, proactive liability management, and prioritising capital spending for long-term economic diversification.

Region sets its sights on long-term value creation

The GCC enters 2026 with a clear agenda: deepen global economic integration, build the foundations of new industries, and strengthen resilience in a more uncertain global environment. Progress across trade, supply chains, technology, workforce transitions, and fiscal policy shows a region positioning itself for long-term resilience and competitiveness rather than short-term adjustment. The extent to which governments and businesses can execute these priorities – mobilising capital, accelerating capability building, and sustaining reform momentum – will determine how effectively the GCC converts today’s opportunities into durable economic gains.

To find out more, keep an eye out for our upcoming Middle East Economy Watch where we examine the latest economic developments across the region in more detail, as well as our shorter Economy Matters blogs and Economy Bites podcast series.

Authors:

- Jing Teow

Contributors:

- Noa Sreden

- Nikhil Judge

- Alaa Abdelaziz