The significance of an ESG strategy consists in prioritising a sustainable entrepreneurship concept within strategic planning and planning by top company executives. We will help your company set sustainable goals and create a strategy to reach them.

Corporate Sustainability Reporting Directive (CSRD)

In the EU, non-financial reporting is based on the Non-Financial Reporting Directive 2014/95/EU (NFRD). This directive has been transposed by Member States into their national legislation. Although national transpositions may vary, the directive's minimum requirements remain consistent.

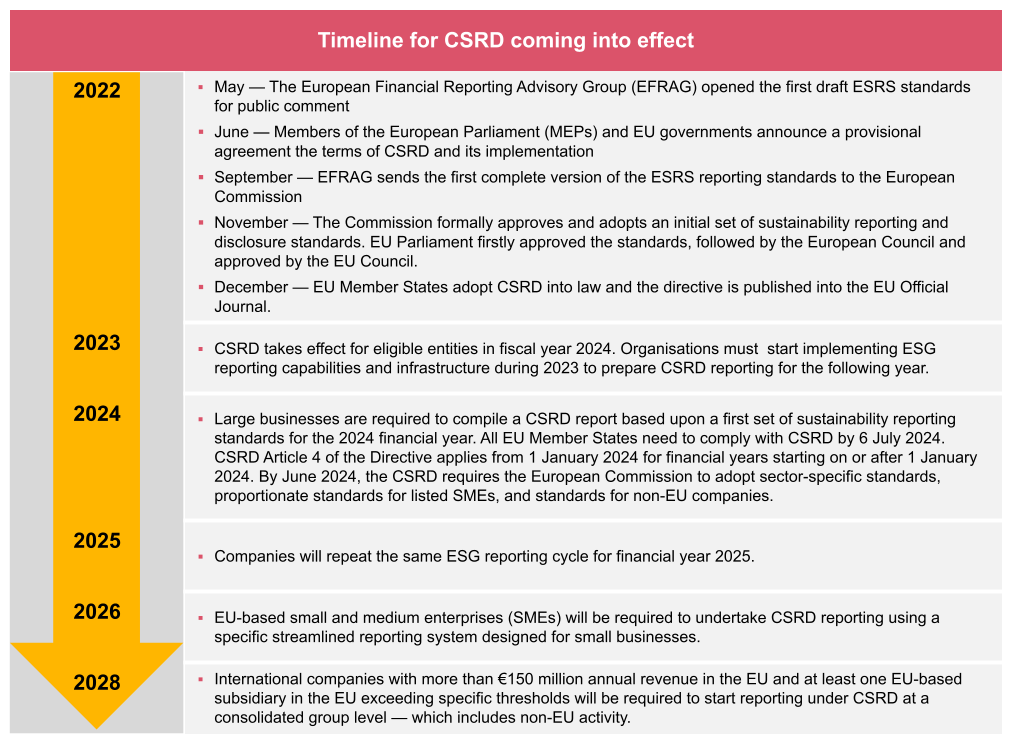

Recognizing the shortcomings in the existing rules on disclosure of non-financial information - NFRD has not met the expectations of providing investors with coherent, sufficient and comparable information - the European Commission has proposed amending the rules by a new directive. The EU Corporate Sustainability Reporting Directive (CSRD) was published in December 2022 and in some cases will come into effect in the 2024 fiscal year. The new regulations mandate more comprehensive reporting obligations and expand the range of companies that fall under its purview. All large companies must report on sustainability issues, including environmental, social, human rights, and governance factors. Who will be covered by the directive?

- Large companies = companies meeting at least 2 of the 3 following criteria:

- 250 employees

- EUR 25 million balance sheet

- EUR 50 million net turnover

- All companies, including SMEs; exact schedule varies by size

- Non-EU companies with a net turnover of EUR 150 million in the EU and at least one subsidiary or branch in the EU

The main features of the CSRD are:

- Mandatory inclusion of sustainability information in management reports

- Mandatory external assurance

- Introducing mandatory reporting standards – European Sustainability Reporting Standards (ESRS)

- Subsidiaries may be exempt from reporting if covered by a consolidated report meeting the CSRD requirements

- Mandatory digital tagging of reports for automated machine reading

When will the rules be applicable?

- Starting from January 1, 2024: companies already subject to mandatory non-financial reporting (NFRD);

- Starting from January 1, 2025: all large companies (as defined above);

- Starting from January 1, 2026: listed SMEs, small and non-complex credit institutions, and captive insurance undertakings.

- Starting from January 1, 2028: non-EU companies with substantial operations in the EU (turnover of over EUR150 million in the EU).

How PwC can help

< Back

< Back

[+] Read More

< Back

< Back

[+] Read More

< Back

< Back

[+] Read More

The Corporate Sustainability Reporting Directive (CSRD) is an EU regulation that entered into force on January 5, 2023. It requires companies to make extensive, detailed disclosures about sustainability performance and related strategic implications. Disclosures are prescribed by the European Sustainability Reporting Standards (ESRS).

The ESRS are reporting standards for sustainability within the EU that cover a multitude of environmental, social, and governance (ESG) topics — including climate change, biodiversity, human rights, etc. The primary purpose of ESRS is to enable a simple and logical structure of sustainability information. The standards are an integral part of the CSRD and there are a comprehensive set of 12 ESRS in operation, with more in the pipeline.

Companies now subject to the EU’s Non-Financial Reporting Directive must follow the Directive for fiscal years starting on or after January 1 2024 (filing reports in FY2025). Other listed companies, along with unlisted companies meeting certain size thresholds, will get more time.

Smart business for brighter future

Sustainability and social responsibility is not just about ticking items off the checklist of obligations set out by the law or by a parent company. The right sustainable entrepreneurship strategy takes into consideration how to stay relevant for your customers even in the future, and thus how to get a head start over your competition. Your ESG transformation should be mainly motivated by the desire to do things in another way and by your commitment towards people and the planet as a whole. Our colleagues from the ESG teams strive to find solutions and technologies ensuring the safety of this world for themselves as well as for their children’s generation.

1:30

Our moment

{{filterContent.facetedTitle}}

{{contentList.dataService.numberHits}} {{contentList.dataService.numberHits == 1 ? 'result' : 'results'}}

{{contentList.loadingText}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

{{contentList.loadingText}}