The time has come to look at indirect costs in detail

Successful back-office optimization requires added value analyses

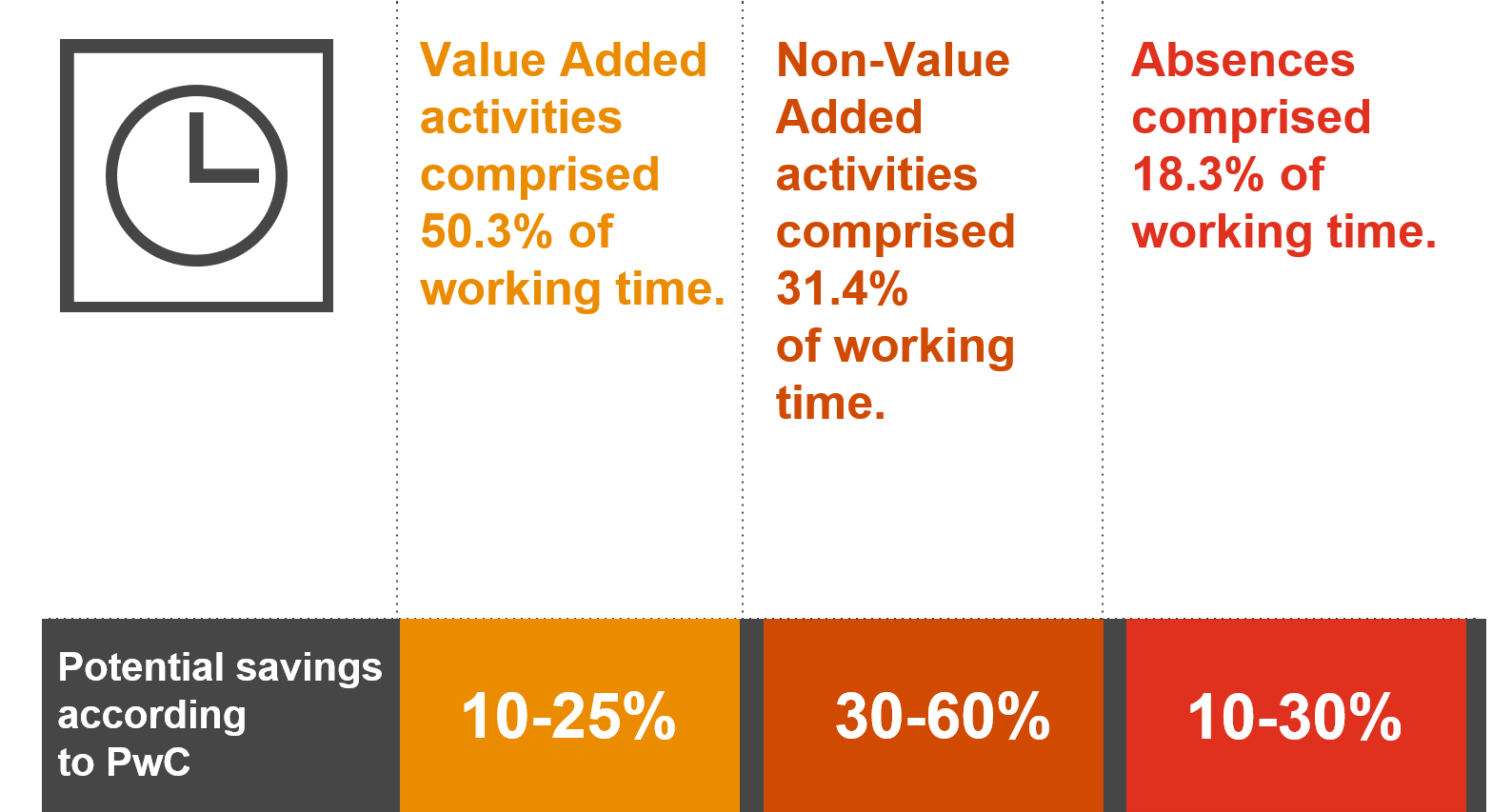

Indirect costs have increased at many organizations in recent years. Companies know that they need to optimize not only manufacturing, but also back-office processes which are not easy to measure. Our experience from transformation projects shows that it is not unusual for back office employees to spend 40% of their working time on low value-added activities. How can companies unlock the potential for increasing company profit by measures in the back office that will bring higher added value?

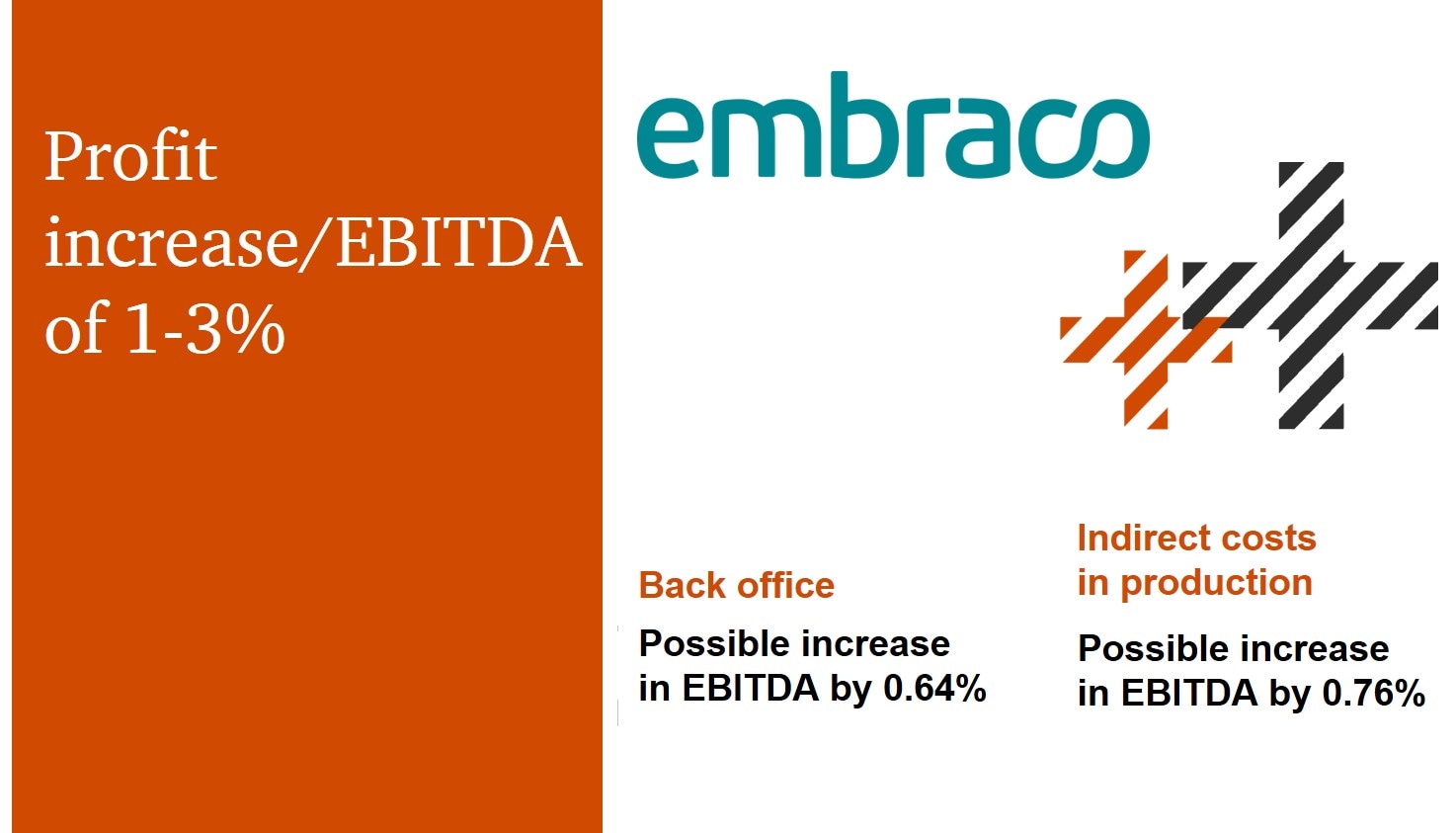

We can find reserves of 1 to 3% of EBITDA in the back office.

What have we achieved with back-office transformation projects?

We found that employees of an energy company spent 30% of their working time on activities of low value to their business;

We achieved annual savings of 20% in the back office of a production company operating in mechanical engineering;

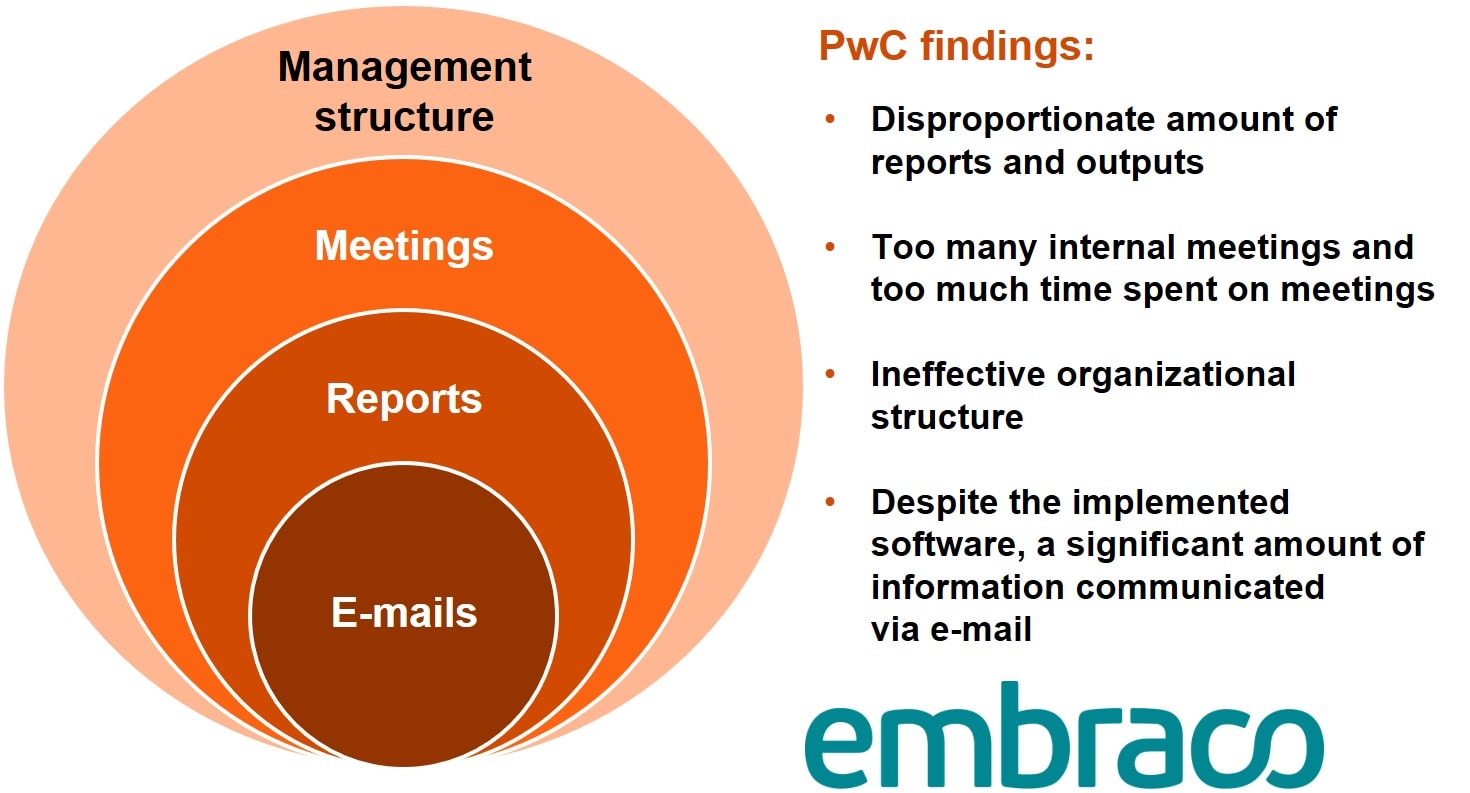

We proposed streamlining the management structure.

We increased the quality of back-office services at a construction company by eliminating duplicate activities and reducing controls;

We streamlined the meeting and reporting structure;

How to consider indirect costs at a company with more than 2,500 employees and turnover exceeding EUR 200 million

Meetings took up 32% of working time and more than 1 FTE was dedicated to reporting

How to make customer care processes at a well-established and growing company more efficient

Summary of all analysed areas

Details of the project:

2. Phase - Design (2 weeks)

- Strategic workshop with company management to determine the optimal state of processes

- Recommendations for implementation and setting priorities for the main focus

- Quantification of savings and added value

1. Phase - Analysis (4–6 weeks)

- Comparison of departments across companies and the sector;

- Management model analysis

- Analysis at activity and process level

3. Phase - Implementation – (4–8 months)

- Implementation plan

- Joint working groups and objectives

- Ongoing evaluation

- On-the-spot implementation support

- Evaluation and completion

References

Contact us