Download the report

Why does working capital matter?

Businesses have continued to face a high level of disruption in the twelve months since our last Middle East Working Capital Study. The impact of the COVID-19 pandemic combined with continued oil price volatility, resurgent inflation, and continued regional fiscal reforms has made it an extremely challenging period for shareholders and executives to manage their business. These disruptions have come while longer term global megatrends have already been reshaping business.

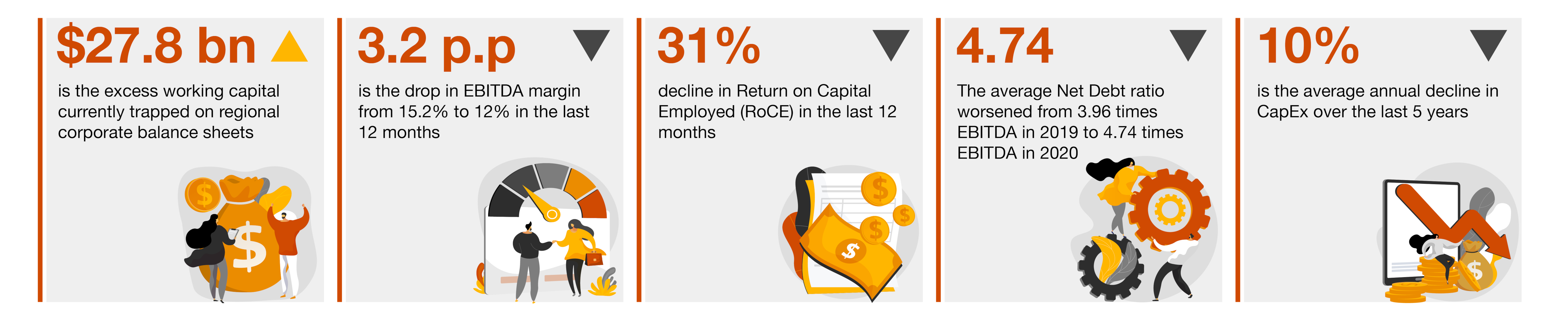

Against this background of rapid change, the importance of capital efficiency is rising. Increased competition, increased investor scrutiny and higher levels of indebtedness are all contributing to a rise in the opportunity cost of trapped capital within organisations.

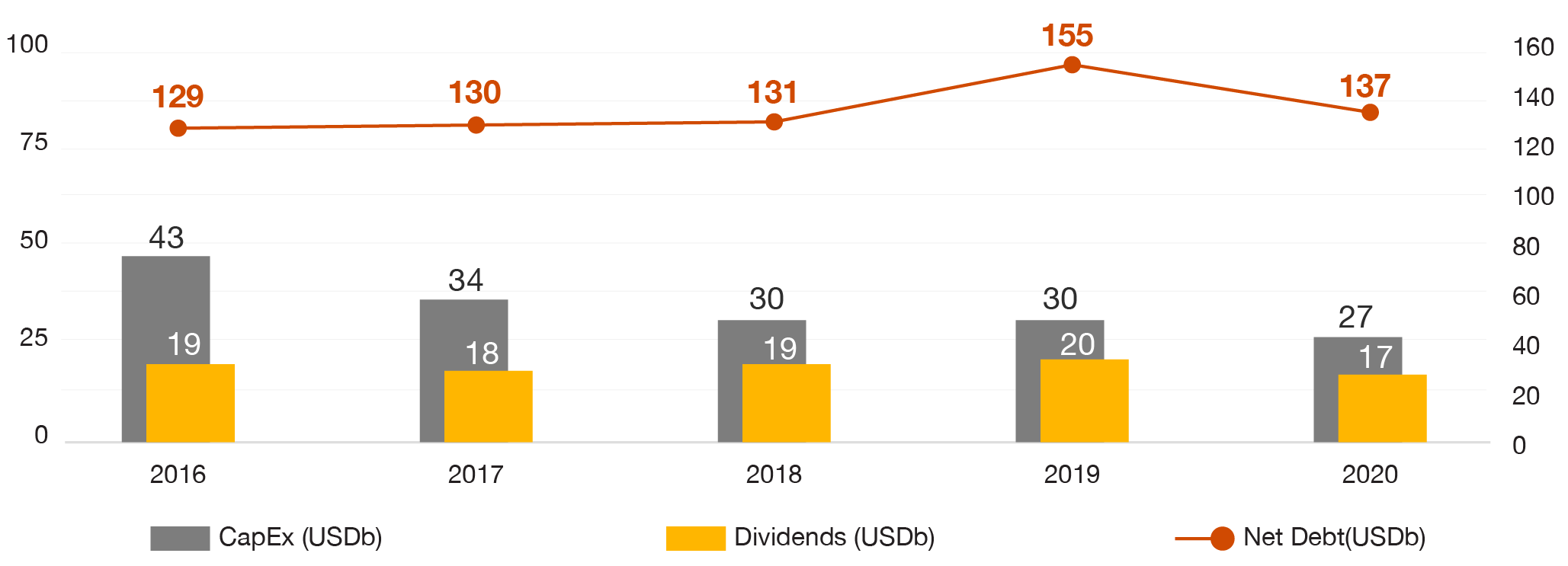

Working capital efficiency is a key metric of corporate competitiveness – and right now that metric is flashing red. Although the top line metric of Working Capital Days has stayed the same, Return on Capital Employed continued to deteriorate and the average debt leverage of companies in our survey increased. Overall, the financial efficiency of regional corporations is declining just at the moment when efficient cash management and capital efficiency is most needed.

In this study we outline how companies can act now to repair cash flows, improve competitiveness, and recover.

Latest working capital trends

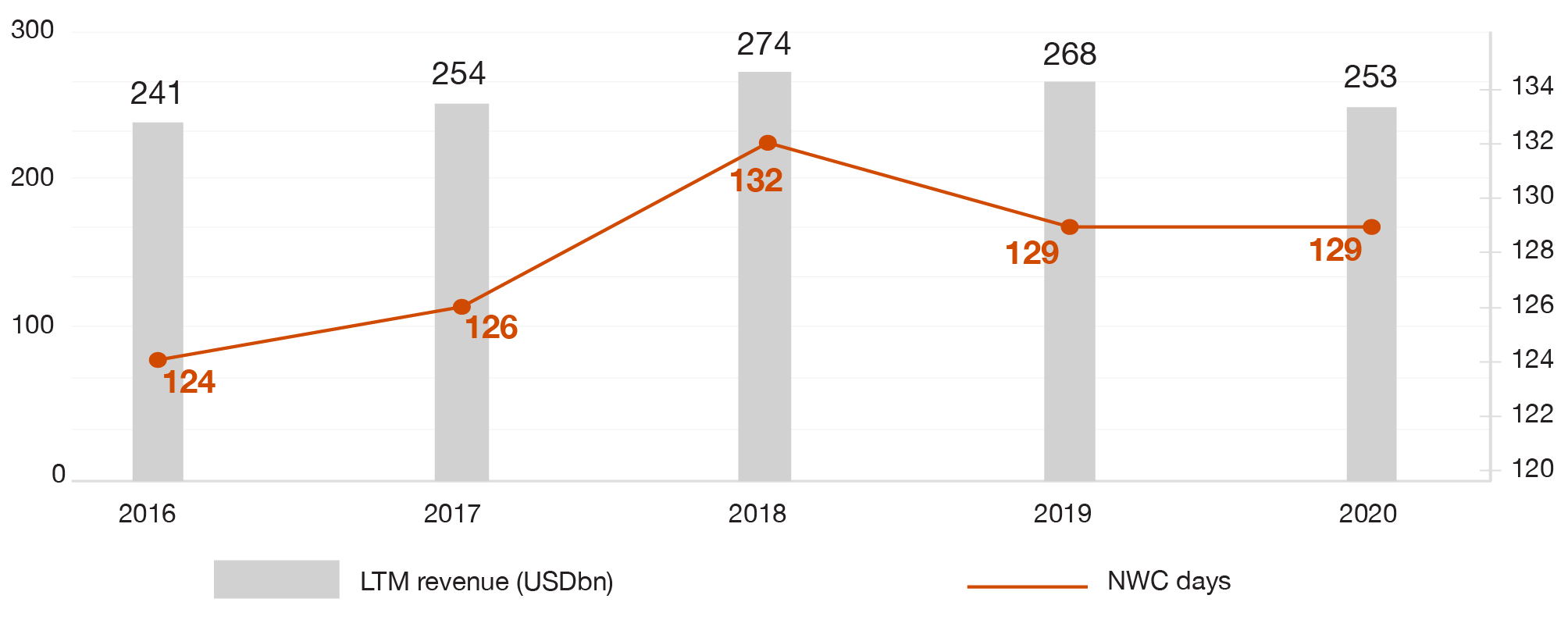

Working capital efficiency in the Middle East measured as average Net Working Capital days has remained largely stagnant in FY20.

Over the last five years, Net Working Capital days have been on a deteriorating trend, increasing by five days since 2016 (equivalent to an average 1.1% deterioration per annum) corresponding to around a cumulative $3.8 billion of additional cash tied up in the operations of companies in our study. This trend showed a mild reversal in 2019 but Net Working Capital days remained unchanged in 2020.

As activities resume to pre-COVID-19 levels, we expect to see reinvestment back into working capital and renewed short to medium term upward pressure on average working capital days. This means that those companies with a clear strategy for where to invest and how to govern their enterprise-wide working capital will be at a significant competitive advantage. Our study shows that companies that have better working capital metrics also show better performance across other KPIs.

Working capital trends

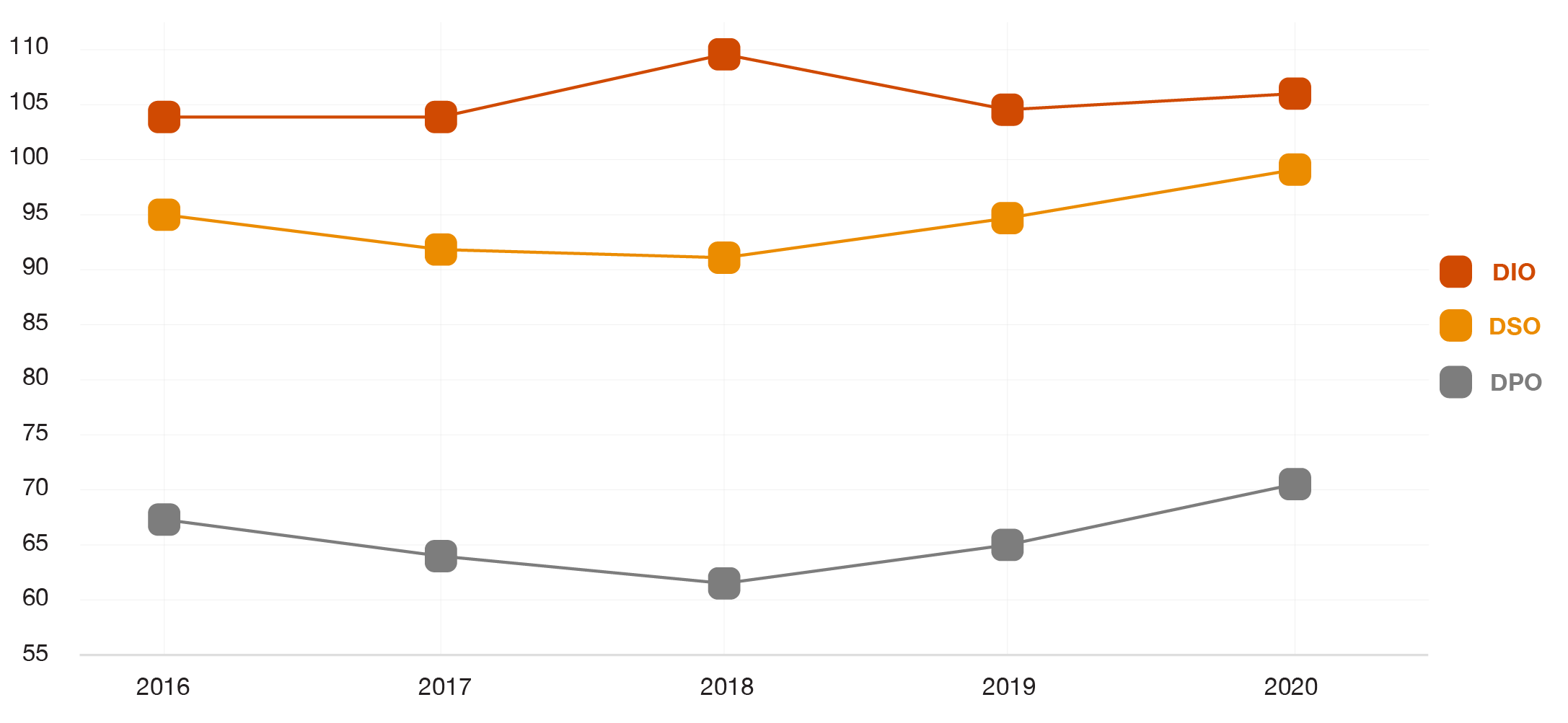

Working capital trends by cycle

The working capital performance of companies in our study has been marked by a significant increase in the days payable to creditors measured by Days Payable Outstanding (DPO). The companies in our study have increased their DPO by six days on average year-on-year. This more than offsets a slowdown in the speed with which companies collect cash from their customers measured by Days Sales Outstanding (DSO) which has increased by four days on average.

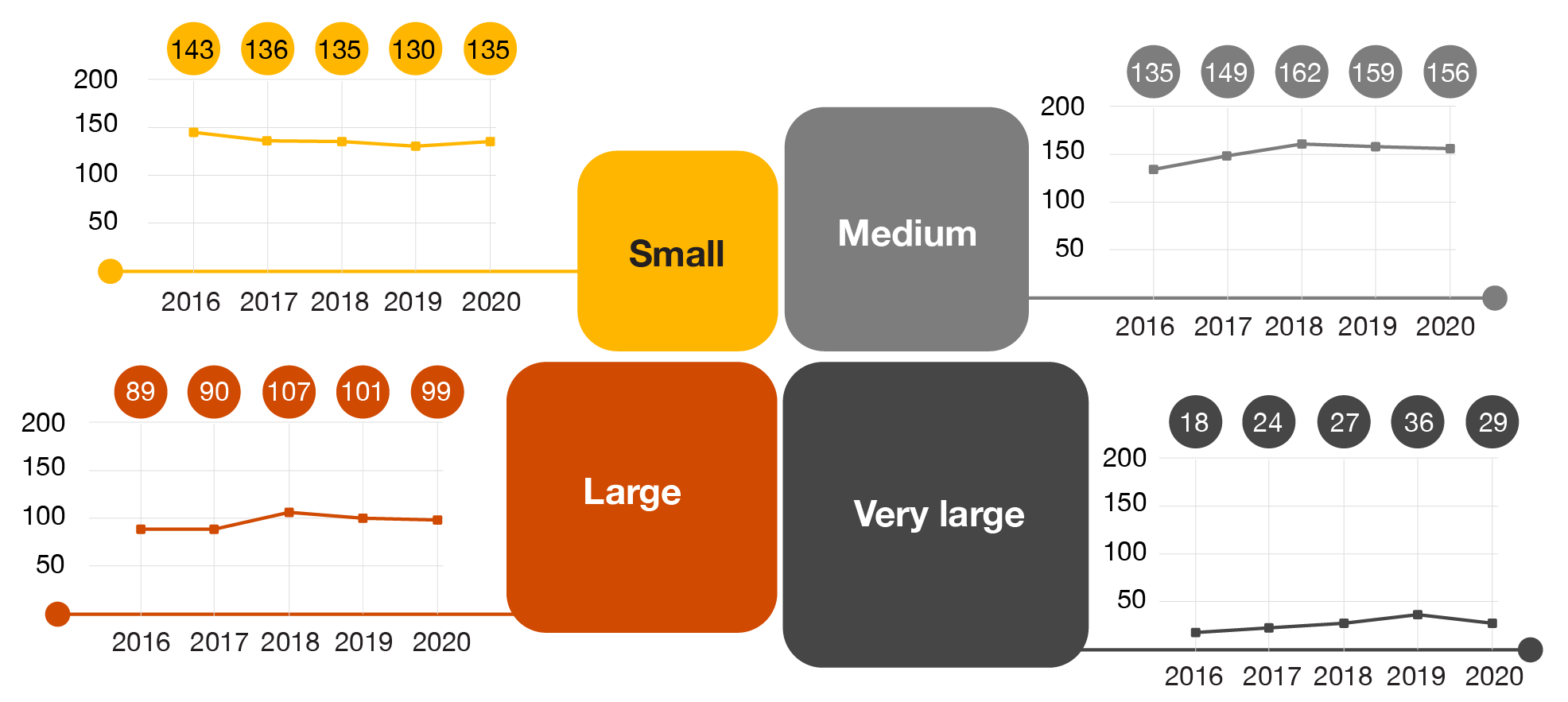

Working capital by company size

The largest companies continue to perform significantly better than smaller groups when it comes to turning cash over, repeating the findings of earlier editions of the PwC Middle East Working Capital Study. Overall, very large companies (annual revenue > USD 2 bn) are three to five times faster to convert cash than their large, medium and small counterparts and this is seen across all key performance indicators. For example, very large companies tend to hold inventory for half of the time smaller companies do as well as collecting cash 12-35% faster than their smaller peers, irrespective of sector. This is a global phenomenon: larger companies can use their buying power in the market to influence their commercial terms and have a greater ability to invest in their transformation initiatives, IT systems and provide training to their staff.

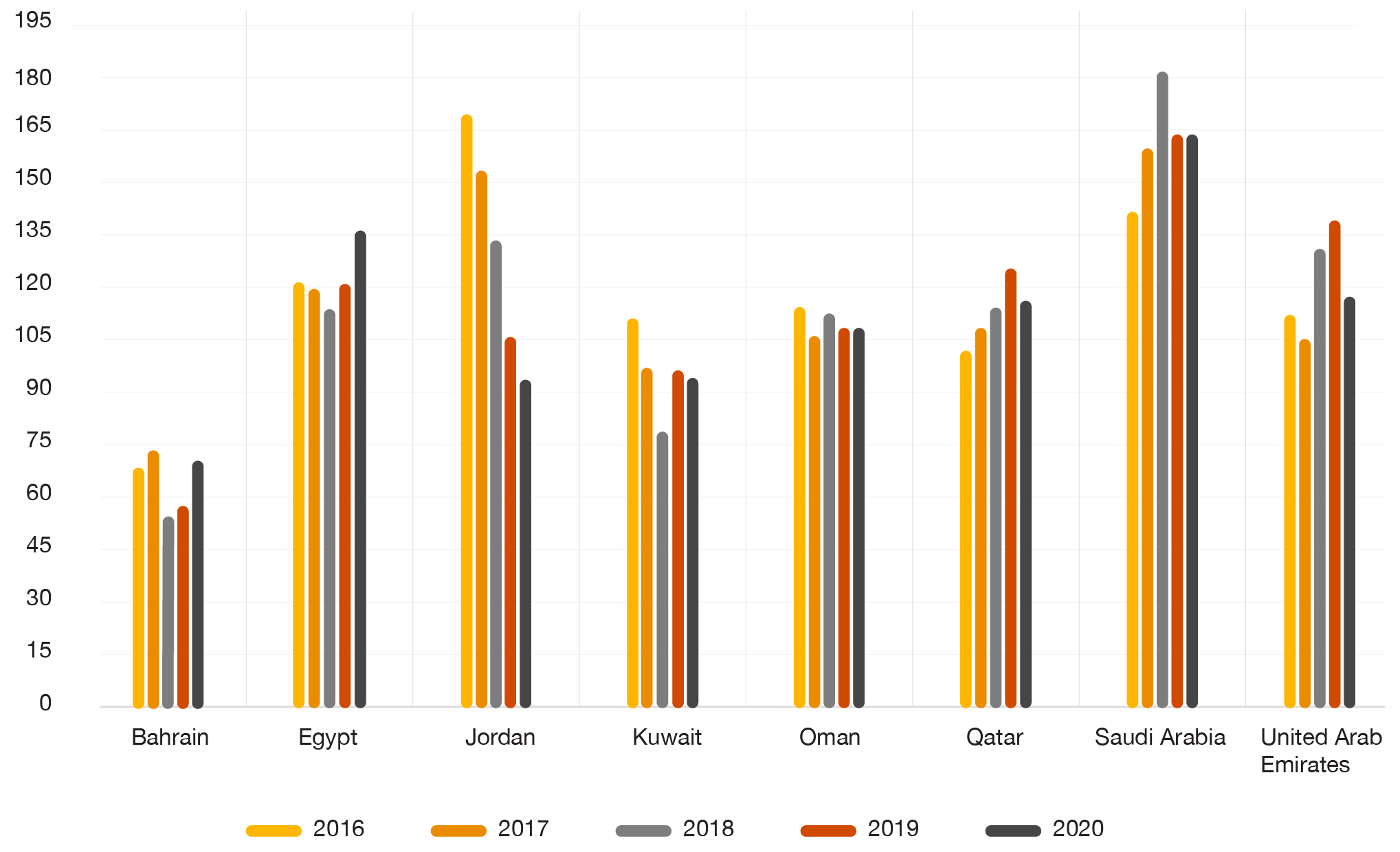

Working capital by country

Based on data from PwC’s Global Working Capital study, companies in the region have a higher level of invested working capital and have lower working capital days on average compared with global benchmarks for working capital performance. There are several factors behind this, including the evolving legal and creditor rights landscape, the widespread acceptance of longer payment terms, and a historical focus on growth and profits, rather than return on capital or liquidity.

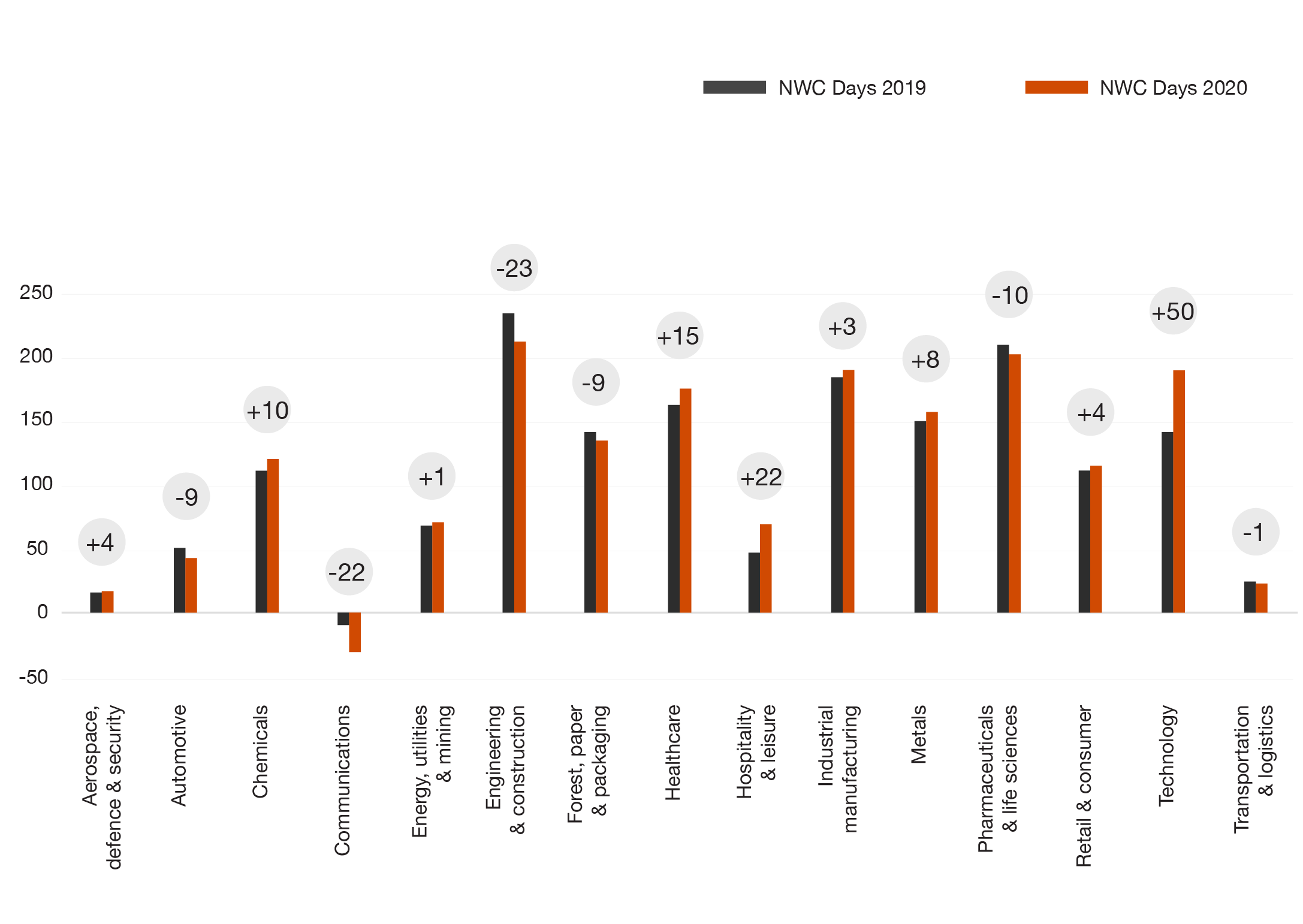

Working capital by industry

Almost half (49.5%) of the companies in our study ended 2020 with a year-on-year improvement in working capital performance measured by NWC days. Seven out of fifteen sectors had an overall improvement in working capital performance year-on-year.

Technology, while one of the better performing sectors in terms of profitability and revenue growth, has neglected its working capital performance and was the lowest performing sector in terms of year-on-year change with six of the seven companies (86%) delivering an increase in NWC days. The second worst year-on-year performance was from the Hospitality & Leisure sector which has been severely impacted by the global COVID-19 travel restrictions and lock down measures. Also, the Healthcare sector was one of the key sectors which were impacted by the COVID-19 pandemic and it has seen a significant deterioration, despite benefiting from COVID-19 testing and patient visits, the sector lost revenue from elective surgeries and other treatments.

The Engineering and Construction sector continues to have the highest average level of working capital, followed by Pharmaceuticals and Life Sciences. Both sectors are known for their lengthy supply chains, complex production and delays in finished products as well as a high number of stakeholders in the supply chain, all of which can increase the challenge of managing working capital.

The 2021 Middle East Working Capital Study shows that working capital management should be seen as a strategic priority for boards and management teams. Better working capital performance is associated with better balance sheet metrics on revenue, debt and profitability, and generates broader non-financial benefits.

Contact us

Dan Georgescu

Director, Performance and Restructuring Services, PwC Middle East

Tel: +971 5 6418 9776

Follow us