“CEOs in Kuwait are investing, transforming and scaling today, using confidence, capability and collaboration to turn near-term uncertainty into long-term advantage.”

In PwC’s 29th Global CEO Survey, business leaders in Kuwait stand out for their confidence, conviction and readiness to act. With optimism underpinned by strengthening economic fundamentals, major infrastructure investment and the ambitions of the Kuwait Vision 2035, business leaders are looking at sustained value creation. This confidence is translating into tangible action, accelerated AI adoption, scaling innovation through partnerships and pursuing large, transformative deals to access new capabilities and markets.

Key findings for the region

% of CEOs in Kuwait expect economic growth in their territory to improve

% expect revenue growth over the next three years

% say their organisational culture enables AI adoption

% plan at least one major acquisition in the next three years

% expect acquisitions to drive exposure to new sectors outside their core business

% say they can lead an effective response when disruption occurs1 What’s driving CEO confidence

Kuwait’s CEOs have demonstrated significant confidence in domestic economic growth. 86% of business leaders expect economic growth in their territory to improve in the next 12 months – a clear contrast to the global outlook, where just 55% of CEOs express similar sentiments about their own territories (see Figure 1). This optimism reflects a strong belief in domestic fundamentals and is grounded in a steady economic recovery in 2025, with the IMF projecting real GDP growth of 2.6%, driven by rising oil output and resilient non-oil activity. Following the unwinding of OPEC+ cuts, oil sector growth is expected to reach 2.4%, while non-oil growth is projected at 2.7%, reinforcing momentum beyond hydrocarbons. The World Bank expects GDP expansion to accelerate further, forecasting growth of 2.7% in both 2026 and 2027.1 Recent policy actions, including the enactment of the Public Debt Law, strengthen this outlook by easing fiscal pressures and enabling renewed infrastructure investment as Kuwait returns to international debt markets after an eight-year hiatus.

Figure 1: What do you believe economic growth (i.e. gross domestic product) will be over the next 12 months in your territory?

Looking ahead, CEOs in Kuwait are more cautious about short-term revenue growth but remain strongly confident over the longer term. Nearly 40% are confident in their company’s revenue growth prospects over the next 12 months, ahead of the global average of 30%. Confidence strengthens significantly over the medium term, with 75% of CEOs in Kuwait expecting revenue growth over the next three years, compared with 49% globally - reflecting a leadership outlook that is focused on sustained value creation (see Figure 2). For the current fiscal year, CEOs in Kuwait report having stronger average revenue growth of 13%, compared with 8% among business leaders globally, and profit margins of 18%, significantly higher than compared than the global average of 10%.

Figure 2: How confident are you about your company’s prospects for revenue growth over the next three years / over the next 12 months?

This longer-term confidence aligns closely with Kuwait Vision 2035. The ‘New Kuwait’ plan sets out an ambition to transform the country into a leading financial and trade centre, driven by a competitive, private-sector-led economy. The vision is underpinned by enabling government institutions and emphasises production efficiency, with modern infrastructure playing a central role in supporting sustainable, long-term progress.

The ambition is being translated into action through major investments and economic reforms. Kuwait’s economic momentum is being reinforced by large-scale infrastructure and development projects, including Silk City, the Mubarak Al-Kabeer Port, the expansion of Kuwait International Airport, and significant residential and commercial developments. The projects represent investment of more than KD92 billion (US$299.5 billion), alongside long-awaited reforms aimed at strengthening the non-oil sector and diversifying sources of income.

Against this backdrop, CEOs in Kuwait are sharpening their near-term focus, with 40% of their time devoted to planning activities within the next 12 months, reflecting a deliberate and disciplined approach to capturing immediate opportunities (see Figure 3).

Figure 3: What proportion of your typical schedule is dedicated to activities associated with the following time horizons? (Mean)

An attractive investment destination

A number of regulatory and legislative reforms have strengthened the competitiveness of Kuwait’s economy and improved the appeal of its capital market to foreign investors. The country has moved into the top 10 investment destinations for Middle East CEOs outside their home markets, with interest strengthening year on year. In 2026, 13% of Middle East CEOs identify Kuwait as one of the three countries that will receive the greatest share of their company’s investments, up from 8% in 2025, a five-percentage point increase. Foreign trading activity in the market has grown at an average annual rate of around 9%, while the value of foreign ownership has increased by approximately 18% over the past two years, reflecting sustained confidence in the Kuwaiti economy.

CEOs in Kuwait are confident not only in domestic growth, but also in the wider region’s prospects. This confidence is translating into tangible regional engagement, with Kuwait investing in a major AI and data centre infrastructure project in Abu Dhabi, underscoring deepening cooperation with the UAE in advanced technology and future-facing sectors.2 At the same time, business leaders are exploring opportunities in Saudi Arabia’s industrial and mining sectors, including expanded collaboration in industrial and petrochemical activities, while seeking to increase trade flows and direct joint investments toward emerging, high-potential areas of growth.3 Reflecting these priorities, Saudi Arabia and the UAE rank as the top regional investment destinations for Kuwaiti business leaders, alongside Iraq, where CEOs see significant opportunities to invest in infrastructure to support the country’s economic transformation.

2 Reinventing with Innovation and AI

CEOs in Kuwait are less likely than their GCC or global counterparts to position innovation as a core part of overall business strategy, with 44% viewing it as critical, compared with 60% of GCC averages and 50% globally. However, under the New Kuwait 2035 plan, digital innovation is positioned as a central enabler of economic diversification, private-sector job creation, and the expansion of e-government services.

What is optimistic is that CEOs are taking a positive approach to innovation. 53% collaborate with external partners to accelerate innovation, well above the global average of 33%, while 47% have routine processes to stop underperforming R&D projects, nearly double the global level of 24%. Business leaders in Kuwait also show a higher tolerance for risk in innovation projects (33% vs. 25% globally), reflecting an approach that emphasises collaboration and disciplined risk-taking (see Figure 4). According to the survey findings, CEOs in Kuwait report that 17% of their company’s total revenue in the current fiscal year is attributable to new products or services introduced within the past three years.

Figure 4: To what extent do each of the following statements characterise your company’s approach to innovation? (SUMMARY NET: To a large or very large extent)

From ambition to application: AI at scale

Technology and AI are playing a central role in enabling and accelerating Kuwait’s future growth. The nation is at a critical point in its digital transformation, moving from building foundational infrastructure to scaling AI adoption across government, business, and academia. While coordination challenges remain, momentum is growing, highlighted by the Kuwait Investment Authority’s entry into the AI Infrastructure Partnership alongside MGX, BlackRock, GIP, and Microsoft.4 AI is being integrated across sectors including public services, finance, education, energy, and healthcare, supported by an emerging ecosystem of start-ups, partnerships, and investments in data governance and skills.

Survey findings indicate this with 50% of CEOs in Kuwait using AI to a large or very large extent in sales, marketing, and customer service, compared with 43% across the GCC and just 22% globally (see Figure 5). CEOs are also outperforming the global average in support services (42% vs. 20% globally) and demand fulfilment (36% vs. 13% globally), while broadly aligning with GCC peers in these areas. Adoption is more moderate in products and services (31%, compared with 36% in the GCC) and direction setting (22%, versus 29% in the GCC).

Recent examples of AI integration include Kuwait Oil Company partnering with IBM to use AI in reservoir management and geological analysis,5 while telecommunications provider Ooredoo has integrated AI for predictive maintenance and customer service, as well as establishing an AI centre of excellence.6

Figure 5: To what extent has AI been applied in the following areas of your business? (SUMMARY NET: To a large or very large extent)

As business leaders moves from ambition to application of AI, a notable 83% of business leaders in the country say that the culture of their organisation enables the adoption of AI, 80% said their technology environment is enabling the integration of AI, while 74% said their organisation had a clearly defined roadmap for AI initiatives.

Yet this confidence coexists with growing strategic pressure. Reflecting the growing pressure to adopt AI in Kuwait and accelerate digital transformation, a quarter (25%) cite business transformation as a key concern. In addition, 17% are concerned about business viability over the medium to long term, while 14% question whether their organisations’ innovation capabilities are strong enough to navigate an increasingly uncertain future.

3 Dealmaking as a catalyst for reinvention

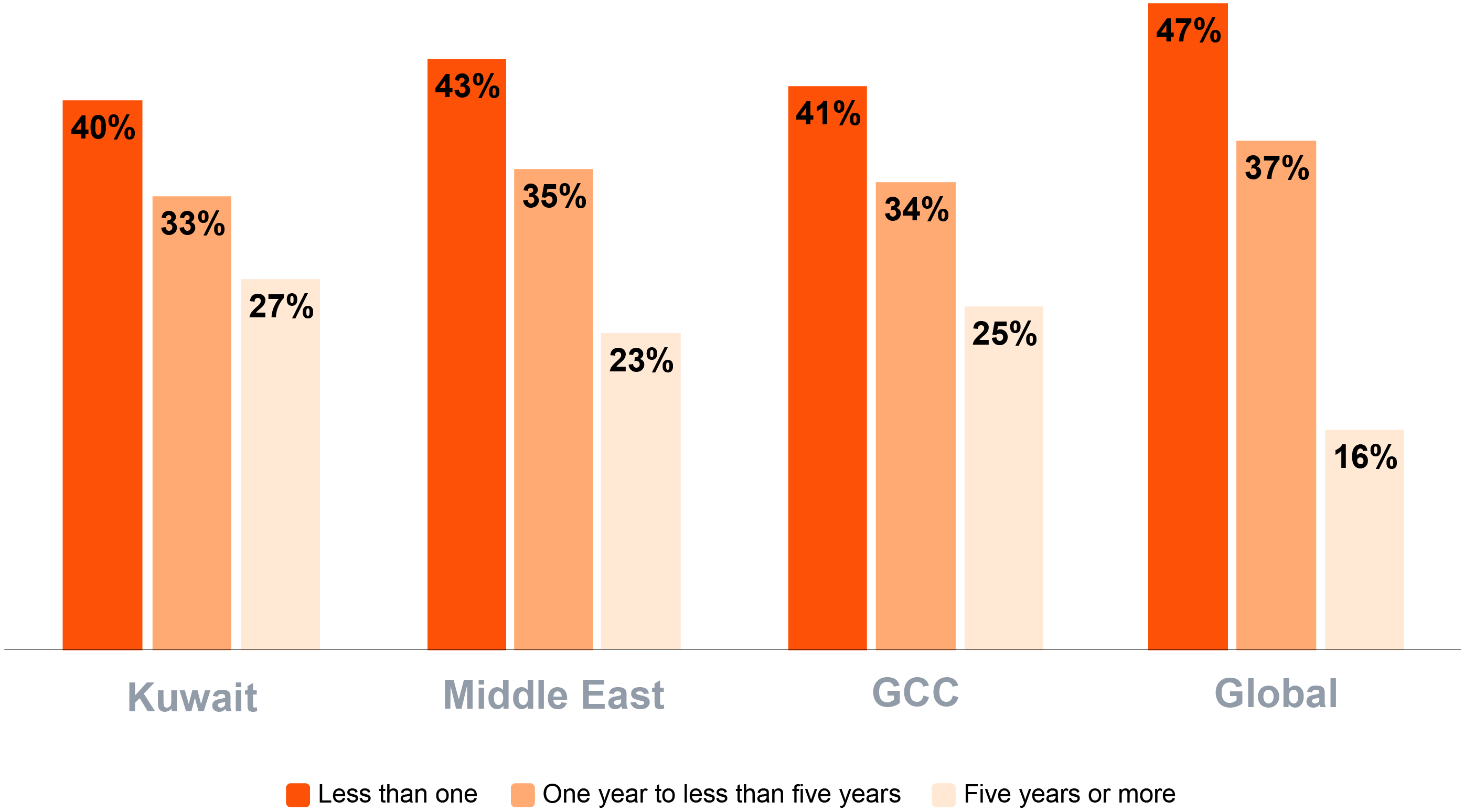

Large-scale acquisitions are a cornerstone of CEOs’ growth strategies in Kuwait. An overwhelming 92% say they plan to make at least one acquisition equivalent to more than 10% of their company’s assets (see Figure 6) over the next three years, largely to build new capabilities, enter adjacent sectors and form cross-sector partnerships to capture the next wave of growth.

Figure 6: How many major acquisitions, worth more than 10% of your company’s assets, is your company planning to make in the next three years?

Business leaders in Kuwait have historically diversified faster than their regional peers – 61% expanded into new sectors over the past five years compared with 39% across the Middle East. This dynamic continues, with 97% of CEOs expecting deal value to come from sectors or industries outside their core business over the next three years, signaling a clear pivot towards faster reinvention.

The key industries that CEOs in Kuwait aim to expand into are Technology, Media and Telecoms (44%), Financial Services (39%) and Consumer Markets (36%).

4 Growing resilience in the face of uncertainty

While geopolitical conflict remains the top concern for CEOs across the region, business leaders in Kuwait are significantly less concerned than their GCC and Middle East peers, with 25% citing it as a key risk compared to 38% regionally. A similar confidence gap is evident around other macro risks, including cybersecurity and economic volatility, which are also viewed as less pressing by CEOs in Kuwait (see Figure 7). To address cybersecurity challenges, 39% of CEOs are planning to significantly strengthen enterprise-wide cyber defences, reflecting recognition that digital exposure is the most immediate vulnerability.

Figure 7: How exposed do you believe your company will be to the following key threats in the next 12 months? (SUMMARY NET: Highly or extremely exposed)

Skills shortages are a notably lower concern for CEOs in Kuwait than across the GCC. Only 9% of CEOs in Kuwait identify the availability of key skills as a major threat, compared with 17% across the wider region. And despite experiencing sharp increases in summer temperatures that impact the environment, climate risk remains underweighted in near-term CEO priorities. Just 8% of CEOs in Kuwait view climate change as a key threat over the next 12 months, even as the country targets 50% renewable energy adoption by 2050.

CEOs in Kuwait demonstrate a notably higher appetite for risk, with 28% reporting an increased willingness to make large new investments over the past year, despite geopolitical uncertainty, well above the Middle East average of 21% and more than double the global figure of 11% (see Figure 8).

Also, rather than viewing uncertainty around tariffs as a headwind, many see it as a source of opportunity. In particular, 64% of CEOs surveyed in Kuwait view tariffs as having little or change to profit margins over the next 12 months. This outlook is underpinned by a strong sense of organisational resilience, with 64% of business leaders confident in their ability to lead an effective response to disruption, and 44% believing they can successfully capture new business opportunities arising from it.

Figure 8: Compared to last year (2024), how has geopolitical uncertainty (including tariffs) impacted your company’s likelihood of making new, large investments?

Alongside external risks, CEOs highlight internal, long-term challenges linked to leadership continuity. Concerns around personal legacy and the strength of leadership teams feature prominently, reflecting the fact that many of Kuwait’s largest businesses are family owned. As these organisations scale, diversify, and undergo digital transformation, questions of succession, governance, and leadership renewal are becoming increasingly critical to sustaining performance and preserving long-term value.

Your next move

Contact us:

Consulting Partner, PwC Middle East

Mohamed Al Mahroos

Partner, Bahrain Country Senior Partner, Government & Public Sector, Tax & Legal Services, PwC Middle East