Our solution to the new CRR III requirements for RWA calculation under the standardised approach

Adoption of CRR III requirements

The adoption of CRR III requirements poses a new challenge for banks by introducing more complex rules for risk weights assignment under the standardised approach to credit risk.

The revised regulation enhances the risk sensitivity and changes the methodology for several exposure classes. More details about the changes are described in our quick manual for STA banks.

The CRR III regulation also introduces changes applicable to the internal-ratings based (IRB) models for the RWA calculation. Further it requires the institutions using the IRB approach to also implement the standardized approach which serves for calculation of the so-called “Output Floor”. More details are summarized in our quick manual for IRB banks.

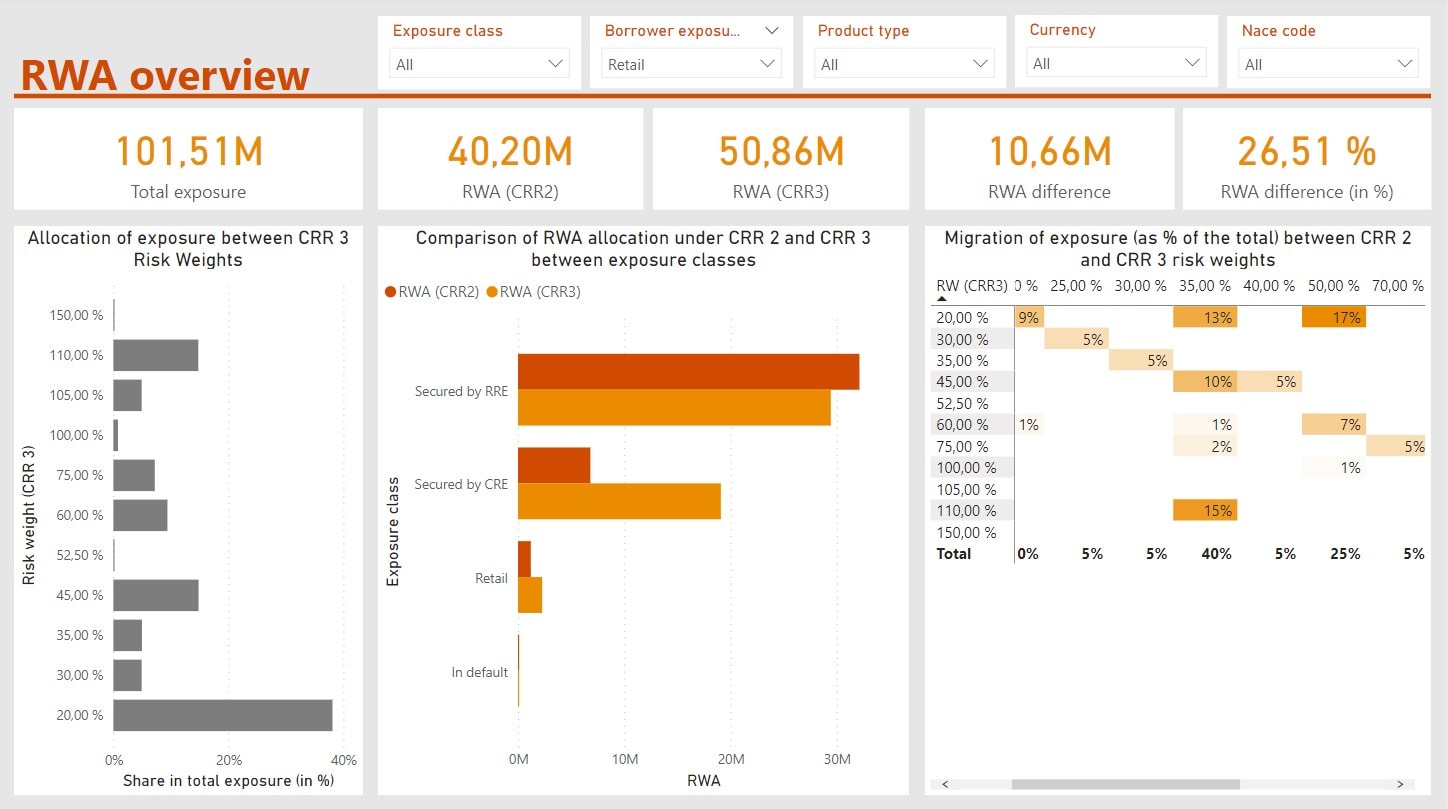

Given the scope of the changes and the time-consuming nature of their implementation, it is crucial for banks to start the CRR III adoption process promptly. To support the banks, we introduce a Risk Weights Calculator that can evaluate the impacts of CRR III requirements on the risk weighted assets. With this tool, we are able to conduct a comprehensive impact assessment, highlight the key impacted areas and identify additional data requirements for the new RWA calculation.

Risk Weights Calculator

The Risk Weights Calculator is an SQL based solution that assigns the risk weights to individual exposures and calculates the risk weighted assets based on the CRR III requirements for the Standardized Approach to Credit Risk.

The tool:

| Assigns the risk weights based on the decision logics for each exposure class. |

| Calculates the risk weighted assets according to both CRR II and CRR III risk weights. |

| Generates results in the form of Power BI dashboard that provides an overview of new risk weights impact as well as further details for the most impacted exposure classes. |

| Contains Satellite modules for additional “subcategories” determination (IPRE, specialized lending, etc.), which can be tailored to the specific needs of a bank. |

| Serves as a proof of concept for successful application of the implementation manual for allocation of risk weights under the Standardized Approach to Credit Risk. |

The Risk Weights Calculator performs several easy-to-follow steps that start with the data import and ends with generation of output reports in the Power BI dashboards.

1. Flexible data input

Import of data either from the flat file or from the client’s data warehouse.

4. Risk weights assignment

Assignment of risk weights based on the CRR III decision logics for each exposure class.

2. Data preparation and quality checks

Preparation of data into standardised form and review of data quality.

5. Report generation

Smart visualization of results in Power BI dashboard.

3. Satellite modules

Possibility to include client-tailored satellite modulus for determination of subcategories like specialized lending, ADC, etc.

What are the practical applications of this tool?

Impact assesment

The tool can be used for recalculation of the risk weighted assets under the CRR III requirements in order to compare to the current RWA and evaluate the overall impact of the new regulatory changes.

Review of implementation

The tool can serve the bank as a challenger model to an internal RWA calculator. By comparing the results from both solutions, the bank can verify a correct implementation of new regulation and can point out any deficiencies in the bank solution.

Support for development

The risk weights assignment logic, incl. the SQL code and input data set, can be used by the bank when developing an internal solution for implementation of the new regulatory requirements.

Portfolio analysis

The Power BI dashboard provides useful insights into the bank’s distribution of the RWA impacts stemming from the regulatory changes and provides further splits to various aspects in the portfolio, such as product type, currency, maturity, etc.

{kind=link}

You are looking for an expert to help you; you want to request our services; or simply ask something? Let us know about yourself and we will get back to you as soon as possible.