2021 Double Tax Treaty Update

12/01/21

Ukraine is actively broadening its network of double tax treaties ("DTT") and is amending the provisions of existing ones. Below we provide a quick overview of changes taking effect this year and what to expect next.

Changes taking effect from 1 January 2021

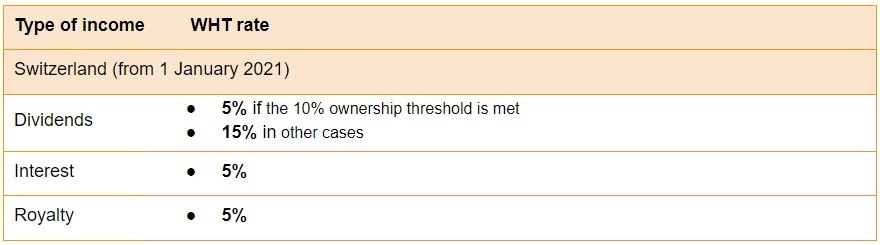

In 2020 Ukraine and Switzerland finalized the ratification of the Protocol to the DTT between the two countries. Thus, starting from 1 January 2021, Ukrainian taxpayers should apply the following withholding tax ("WHT") rates upon making payments to their Swiss counterparties:

More and more countries are joining the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting ("MLI"). Thus, the number of Ukrainian DTTs modified by the MLI is increasing. Starting from 1 January 2021, the principal purpose test ("PPT"), which is one of main MLI changes, became part of the DTTs with the following jurisdictions: Cyprus, Egypt, Jordan, Kazakhstan, Latvia, Portugal, Saudi Arabia, South Korea. As a reminder, the PPT stipulates that the tax authorities may deny treaty benefits, e.g. reduced WHT rates, if there are sufficient reasons to conclude that the principal purpose or one of the principal purposes of the particular transaction / arrangement was to obtain those treaty benefits.

During 2020, the ratification procedures for the Protocols to the DTTs with Singapore and Turkey were completed as well and the Protocols entered into force. The Protocols do not change the WHT rates. The one with Singapore only amends the provisions on the exchange of information between the tax authorities. The Protocol to the DTT with Turkey also introduces an article on assistance in the collection of taxes and restates several definitions (resident, taxes covered, etc.).

Further changes to the DTTs in effect

In 2020, Ukraine and Austria completed all internal procedures for the ratification of the Protocol to the DTT between the two countries save for the last technical formality on the exchange of ratification letters. Therefore, the Protocol to the DTT with Austria is expected to enter into force this year and from 1 January 2022 (1 January 2023 for royalty payments) the following WHT rates should apply to the payments to Austrian residents:

Ratification in progress / awaiting ratification

Earlier, in 2019, Ukraine ratified the new DTT with Malaysia. However, the new DTT is not in force yet, because Malaysia has not completed the ratification procedures from its side yet.

The Protocol to the DTT between Ukraine and the Netherlands as well as the new DTT with Spain are already signed, but they are waiting for both treaty countries to launch the ratification procedures.

Awaiting signing

Ukraine also plans to sign soon the DTTs with Oman and Sri Lanka, and the Protocols to the existing DTTs with Denmark and the UAE. The respective texts of the DTTs / Protocols are already approved by the Government of Ukraine for further signing.

We will continue monitoring the developments in the international tax area and keep you updated.

Contact us

Anna Nevmerzhytska

Director, Head of Financial Services & International Tax Solutions practice, PwC in Ukraine

Tel: +380 44 354 0404