The Protocol amending the Ukraine-Switzerland Double Tax Treaty entered into force

02/11/20

Ukraine and Switzerland have finished all ratification procedures with respect to the Protocol amending the Double Tax Treaty between the countries ("Protocol"). Thus, on 16 October 2020 the Protocol entered into force.

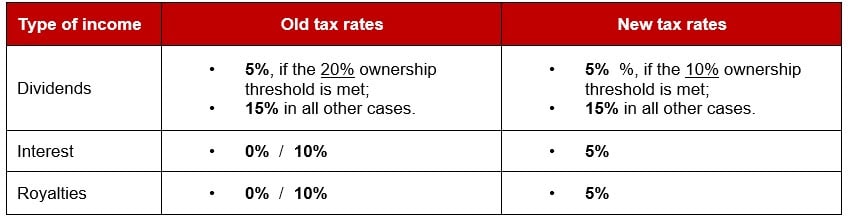

Starting from 1 January 2021 the reduced withholding tax ("WHT") rates are changed as follows:

In addition, the Protocol introduces the so-called ‘principal purpose test’ as per which the tax authorities may deny treaty benefits, e.g. reduced WHT rates, if there are sufficient reasons to conclude that the principal purpose or one of the principal purposes of the particular transaction / arrangement was to obtain those treaty benefits.

The Protocol also amends provisions concerning the exchange of information between the tax authorities, mutual agreement and arbitration procedures.

We will continue monitoring developments in the international tax area and will keep you updated accordingly.

Contact us

Anna Nevmerzhytska

Director, Head of Financial Services & International Tax Solutions practice, PwC in Ukraine

Tel: +380 44 354 0404