Blockchain: A new tool to cut costs

Blockchain is a unique opportunity for financial institutions, changing our lives in profound ways and unleashing a set of new capabilities to transform the way we interact and collaborate in our activities with better security and better authenticity of files, says Max Di Gregorio of PwC Middle East.

The pace of innovation has been hectic in the past few years with the surge of new disruptive technologies. Amongst all these new solutions, the most promising one available today is blockchain. It is a distributed ledger providing an immutable, reliable and shared view of transactions – such as monetary transactions, property records or other valued assets – between engaging parties in a fully untrusted environment.

Its unique characteristics enable institutions to operate a lot quicker and in a cheaper way, with a far lower error rate, with less resulting risks, lower capital requirement and is less vulnerability to cyber attacks.

Financial services is the sector most likely to be disrupted by this technology, with a shared consensus that blockchain represents a tangible innovation over many of the systems and processes used today. Blockchain may have a long-term influence on the global economic system, reshaping market structure, customer experience and product features. According to the PwC 2016 FinTechreport, blockchain-related interest and investment have reached critical mass, and the technology has shown itself to be capable of driving major change.

Max Di Gregorio

Technology Consulting FS Lead Middle East & North Africa

In financial services

The blockchain potential in financial services is huge, and has several applications which span across payments, capital markets, trade services, investment and wealth management, securities and commodities exchanges. Blockchain technology can be considered as one of the main drivers to achieve a substantial cost saving. According to a Santander FinTech study, distributed ledger technology could reduce financial services infrastructure cost between US$15 billion and $20 billion per annum by 2022, providing the possibility to decommission legacy systems and infrastructure and significantly reduce IT costs.

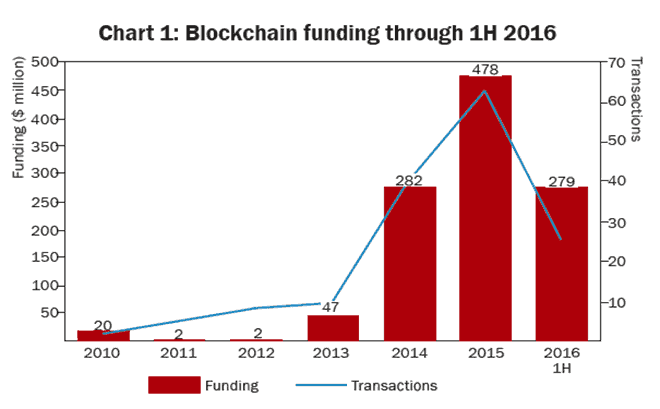

Firms will have the possibility to reduce the need for manual intervention in aggregating, amending and sharing data, and regulatory reporting and audit documents could become easier, requiring less manual processing. As a result, employees could focus exclusively on value-added activities. Post-trade reconciliation and settlement are clear examples of time-consuming and expensive processes that financial institutions could completely redesign by adopting blockchain technology. Financial firms would be able to share a common digital representation of asset holdings and to keep track of the execution, clearing and settlement of securities transactions outside their legacy proprietary databases, without needing the involvement of a central database management system (Chart 1).

Smart contracts for insurance

An interesting application of blockchain technology in financial services, and in particular in the insurance sector, is related to smart contracts.

A smart contract is a digitally signed computable agreement between two or more parties containing some business logic that is capable of initiating certain actions when predefined conditions are met. While P2P insurance as a business model is already being offered using standard technology, blockchain makes it even more transparent and trustworthy for consumers as no central authority controls its operation. As an example, the start-up InsureETH demonstrated a P2P flight insurance policy built on Ethereum blockchain with smart contracts. These smart contracts initiate payouts for insured flight tickets when the cancellations or delays are reported from verified flight data sources.

Claims management

Claims management process can benefit from blockchain, ensuring that only valid claims are paid. The major benefit that this approach would achieve is a reduction – if not a full prevention – of fraud since multiple claims for the same event would be rejected by the network because the network itself already contains the information that the claim has been paid. Moreover, storing historical claims information on the ledger will enable insurers to identify suspicious behaviour and improve fraud assessment.

In the Internet of Things, cars, electronic devices or home appliances can have their own insurance policies registered and administered by smart contracts in a blockchain network, automatically detecting damage first, and then triggering the repair process, as well as claims and payments.

A car insurance smart contract would be embedded in the car, and register a wide range of driving information such as speed, time of drive, driving style, weather, road risk and traffic conditions, providing a trustworthy way to determine the insurance premiums based on predetermined factors.

For financial institutions

Considering the exponential progression of blockchain start-ups in the past years, large traditional financial services companies face the increasing challenge of how to make sure that they are not running behind the innovative companies that are shifting the way financial services are provided.

They face a choice of whether to fully commit to developing their own inhouse innovation, or buy up or partner with innovative start-ups to “import” their knowledge. Another trend is to join consortia, such as R3 or Digital Asset Holdings, to agree on common standards and use cases. In 2016, nearly every major financial institution was experimenting with blockchain.

Unique opportunity

Blockchain is a unique opportunity for financial institutions, where its value can be compared to the impact of the Internet in 1995, changing our lives in profound ways and unleashing a set of new capabilities to transform the way we interact and collaborate in our activities.

However, it is still an emerging technology, and there are outstanding open points related to security, regulation and scalability that need to be addressed. It may take three to five years to reach the maturity stage and become mainstream.

Max Di Gregorio

Technology Consulting FS Lead Middle East & North Africa

This article first appeared in Middle East Insurance Review in February 2017.

© 2017 PwC. All rights reserved.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers (Dubai Branch), its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision

Contact us