Digital tax introduced for e-commerce operators

In brief

Effective from 01 April 2020, the Government of India has widened the scope of its equalisation levy to include e-commerce sales of goods and services provided by non-resident operators to Indian customers.

The equalisation levy is imposed at 2% on the considerations received or receivable by the non resident e-commerce operators. Businesses based in Mauritius or other jurisdictions and engaged in e-commerce activities in India have to assess the impact of this new levy on their business model and start thinking ahead on how this levy could potentially impact on their cost structure or could be used as a foreign tax credit.

The first quarterly filing of the equalisation levy for qualifying e-commerce operators is due by 07 July 2020 for the period April to June 2020. It is important to adhere to this new compliance obligation in India to avoid penalties and interest.

Browse this page

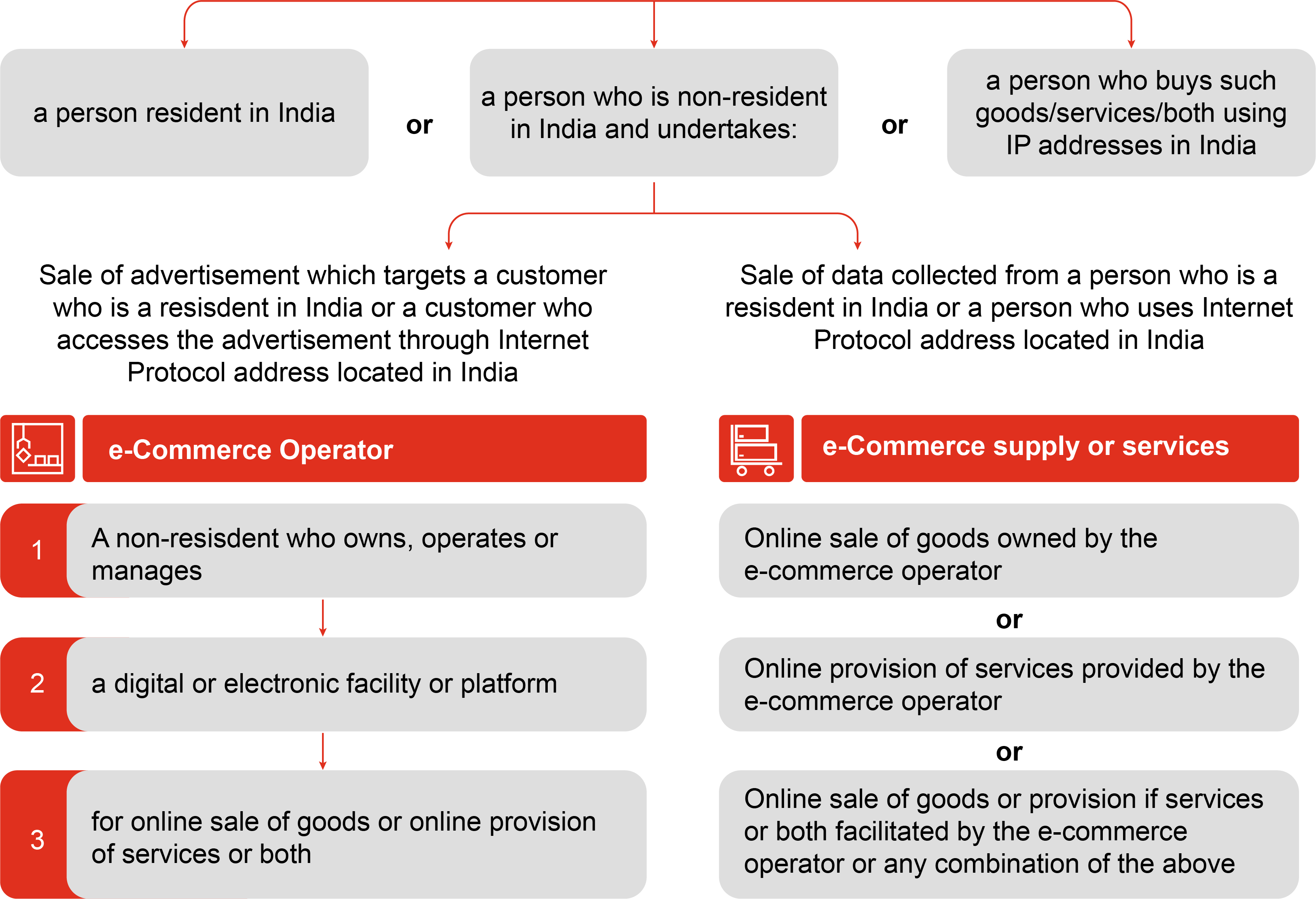

India introduced a digital tax in the form of an ‘Equalisation Levy’ (‘EL’) in 2016. Initially, the EL was levied on online advertisements and other related payments for provision of digital advertising space at the rate of 6% to non-residents not having a permanent establishment (‘PE’) in India.

Effective from 01 April 2020, the Indian Government has expanded the scope of the EL to cover all non-residents who own/operate/manage an e-commerce facility or platform for online sale of goods or services or both or facilitation of such sale.

Imposition of the Equalisation Levy

EL shall be levied at 2% on consideration received or receivable by an e-commerce operator from e-commerce supply or services made or provided or facilitated to:

‘Online’ is defined as a facility or service or right or benefit or access that is obtained through the internet or any other form of digital or telecommunication network.

Exclusions to EL

- Where an e-commerce operator which is making/providing/or facilitating e-commerce supply or services, has a fixed place PE in India & such e-commerce supply or services is effectively connected with such fixed place PE in India;

- Where the EL is chargeable under other specified services such as online advertisement or provision of digital advertising space under the Indian laws; and;

- Sales or turnover or gross receipts from e-commerce supply or services is less than INR 20 million (around USD 264k) during the previous year.

Income subject to EL will be tax exempt under other provisions of the Indian Income Tax Act from FY 2021-22.

Compliance obligations

The levy is structured as a payout by the operator and not as a withholding tax by the payer. Hence, where a Mauritius company is a non-resident operator in a digital platform or facility in India, it will have to make a payout of the EL as a non-resident payee outside India.

It is therefore important for a non-resident supplier of goods and services outside India to take cognizance of the impact of this new provision made by the Government of India.

The EL is required to be deposited by the e-commerce operator to the credit of the central Government of India on quarterly basis on the below mentioned due dates:

Quarter ending |

Due Date |

|---|---|

30 June |

07 July |

30 September |

07 October |

31 December |

07 January |

31 March |

31 March |

Due date for payment of the EL for the first quarter, i.e. April to June 2020, is 07 July 2020. Accordingly, it is important to determine and finalise the position on the application of this levy at the earliest.

Also, as per the existing provisions, every person deducting the EL is required to furnish an annual EL statement on or before 30 June of each year. (The rules and form with respect to the EL paid by the e-commerce operators are yet to be prescribed)

Failure to furnish such a statement shall attract a penalty of INR 100/ for each day of default. If a false statement has been filed, then the e-commerce operator may be subject to imprisonment of up to 3 years and a fine.

Key decision making points for non-resident e-commerce operators

The definition of e-commerce operator

- Whether an entity in Mauritius will be considered as an e-commerce operator?

- Will owning / operating / managing an electronic and digital facility characterise the Mauritius entity as being an e-commerce operator?

- What is the scope of the phrase ‘online provision of services’? Would online subscription of software /eBooks /movies /music etc, distributor and other licenses, B2B arrangements, etc. constitute an online provision of services? It is important to evaluate the facts of each case.

Rendering of services

- Whether the Mauritius entity will be considered as rendering services or supplying goods to residents in India while being an e-commerce operator?

- What will be the position of the Mauritius entity vis-a-vis taxability?

Historically, there have been debates around the characterisation of income from software, particularly whether these should be classified as royalty or business income. The characterisation of income from software agreements are usually assessed on a case to case basis.

Therefore, in such cases, businesses would need further guidance on whether such income would be classified as business income and therefore be subject to the EL of 2% or such income would be treated as royalty or Fee for Technical Services (“FTS”) and would be subject to tax at 10% (including surcharges and cess).

Permanent Establishment

- Would the online provision of services be said to be effectively connected with the PE in India?

- If yes, would the Mauritius entity be eligible for the EL exemption?

Tax credit in Mauritius

The EL is neither a direct or an indirect tax. Therefore, businesses have to determine whether this levy should be expensed or could be treated as a withholding tax and be claimed as foreign tax credit in Mauritius or elsewhere.

How PwC can help:

- Talk to us to see how this EL would impact your business especially where the position of income characterisation from online software providers could be more difficult now.

- We can review the agreements in place for online services provided and evaluate to what extent the EL could be claimed as a credit in offshore jurisdictions and as such minimise the overall tax leakage.

- We can also assist in the compliance obligations of qualifying non-resident companies in India.

Follow PwC Mauritius