Vietnam stands at a pivotal moment in its growth story. According to PwC’s Value in Motion latest research shows trillions are flowing globally towards new, sustainable domains of value—driven by climate transition, technological advances, and shifting stakeholder demands. For Vietnam, this aligns with a strong national focus on green growth, offering both opportunity and urgency for businesses.

In 2022, our inaugural ESG Readiness Survey found that while awareness was high, Vietnamese businesses were just beginning their journey. Today, our latest findings chart a significant evolution. Momentum is building as commitment solidifies into strategy and tangible action.

Our latest ESG Progress Tracker captures the perspectives of 174 respondents from prominent Vietnamese businesses. This report shows progress yet also reveals that challenges now evolve in their complexity. While many organisations are advancing, they face uneven maturity across ESG dimensions and require more sophisticated data capabilities to bridge the gap between reporting and genuine value creation.

The message from our findings is clear: while governance provides a strong foundation, the next stage of maturity requires embedding ESG into the very core of business operations. This is the essence of moving beyond compliance to reinvention—leveraging data, driving efficiency, and collaborating across the ecosystem to build lasting competitive advantage.

Key themes from survey result

The inaugural ESG Readiness Survey in 2022 highlighted a landscape more defined by awareness than action. Businesses were at the early stages of their ESG journey, focused on initial perceptions and plans.

As the landscape evolves, the 2025 ESG Progress Tracker survey examines the shift from intent to implementation, measuring progress since 2022 and identifying momentum and persistent challenges. Findings from amongst businesses operating in Vietnam have been grouped into three themes:

Rising ESG Commitment ❯

ESG has rapidly evolved from an emerging consideration to a strategic imperative for businesses in Vietnam, with a clear shift from planning to execution.

This progress, however, is not uniform. Varied rate of ESG adoption is evident across different company types.

Narrowing the Action Gap❯

Organisations are making notable strides in embedding ESG into their operations, yet challenges remain. While a majority have formal ESG strategies and leadership in place, fewer have fully integrated these into their core business models.

Tangible initiatives and data practices are gaining traction, but the use of advanced tools and standardised reporting still lags behind.

Accelerating ESG Maturity ❯

The foundations-first approach prioritises governance and risk management, with environmental and social themes following.

As organisations mature, challenges are shifting from internal capability gaps to external systemic barriers, with progress enabled by clearer policies, accessible capital, and tailored support.

Vietnam’s ESG Journey in Context

The Global ESG Development Landscape

The global ESG narrative is increasingly defined by divergence. The European Union is forging ahead with comprehensive rules like CSRD and CSDDD, while the United States presents a more fragmented landscape. Asia-Pacific markets such as Japan, Singapore, and Australia are adopting ESG frameworks at varying speeds, often aligning with global standards but tailoring them to local priorities. In Latin America and Africa, ESG adoption is growing, though enforcement remains uneven.

A unifying trend is clear: the era of voluntary promises is over. We are now in an age of mandatory, data-driven, and externally assured ESG information. Regulators are cracking down on greenwashing and demanding verifiable proof of sustainability across supply chains. This new era of scrutiny demands genuine action, making the global stage more complex to navigate than ever before.

Asia’s ESG Journey: Policy to Practice

While mirroring global trends, Asia is entering its own distinct phase focused on implementation. Acknowledging a degree of ESG fatigue, the region is shifting from rapid policy creation to the practical application of new standards. This is defined by two key forces:

- Firstly, Asia is rapidly unifying around the International Sustainability Standards Board (ISSB) framework as a regional baseline, promising greater harmonisation.

- Secondly, the ripple effect of EU regulation is being felt strongly, as the CSDDD cascades due diligence requirements down through Asian supply chains.

This is happening alongside a regional race for transition finance, where access to capital is increasingly conditional on having a credible corporate transition plan.

Vietnam’s ESG Imperatives in a Global Economy

For Vietnam's export-driven economy, global regulatory developments create immediate and tangible challenges. Meeting stringent environmental and human rights requirements is essential for maintaining access to international markets.

- In the US, enforcement of regulations—particularly those targeting forced labour—continues to exert pressure on exporters and manufacturers. Rising tariffs are further disrupting supply chains, increasing operational risks, and prompting Vietnamese businesses to explore alternative markets such as the EU and Asia-Pacific.

- In Europe, though sustainability regulations are being simplified, the aim is to reduce duplication while not diluting their substance. Recent updates to the Carbon Border Adjustment Mechanism (CBAM), the Corporate Sustainability Reporting Directive (CSRD), and the EU Deforestation Regulation (EUDR) reflect this approach.

To remain competitive, Vietnamese companies must embed sustainability into operations and governance. A credible ESG strategy is now critical to unlocking new markets, attracting foreign investment, and meeting the expectations of global brands seeking responsible suppliers. Navigating this evolving landscape requires proactive adaptation, strategic foresight, and a commitment to long-term resilience.

Vietnam's ESG Efforts: Ambition and the Implementation Gap

Vietnam’s pledge at COP26 to achieve net-zero by 2050 marked a pivotal turning point in its climate policy. The government has since moved decisively from ambition to action, establishing a robust policy framework with NDC 2.0 and a comprehensive National Climate Change Adaptation Plan in November 2024. Initiatives include piloting a carbon market, promoting renewable energy, and enacting numerous regulations.

Despite this momentum, a significant implementation gap remains. World Bank analysis suggests current policies, including Power Development Plan VIII, may reduce emissions by only 55%, short of the net-zero goal. Vietnam is expected to achieve just a 38% reduction by 2030, compared to its pledged 43.5%.

Structural challenges include high emissions intensity, reliance on fossil fuels, limited technology adoption, financing bottlenecks, and uneven coordination. Vietnam is preparing NDC 3.0 for 2026–2035, aiming to finalise it before COP30. Bridging the gap will require stronger policy coherence, institutional reform, and accelerated investment in technology, capacity building, and international cooperation.

Navigating the ESG Journey in Vietnam

1 Rising ESG Commitment: From Intent to Strategy

ESG Commitment is Solidifying

ESG has rapidly evolved from an emerging consideration to a strategic imperative for businesses in Vietnam, with a clear shift from planning to execution.

This progress, however, is not uniform. Varied rate of ESG adoption is evident across different company types.

Compliance and Stakeholder Pressure Set the Pace

The key drivers for ESG adoption in Vietnam are clear and compelling, shaped predominantly by external and top-down pressures, complemented by intrinsic operational benefits. Our survey reveals that the motivations are less about immediate financial gains and more about securing a licence to operate in an increasingly demanding market.

- Compliance is the dominant force. An overwhelming 70% of respondents cite compliance with regulations as a top driver, establishing it as the primary motivator for ESG action.

- External and top-down pressures reinforce the trend. This is followed closely by responding to stakeholder pressure (40%) and directives from leadership (39%). Together, these factors show that the ESG agenda is being set from the outside in and the top down.

- A missed opportunity is revealed. Tellingly, reducing costs is a driver for only 16% of businesses. Similarly, access to finance (25%) is not yet a top-tier driver, indicating that the benefits of green financing may not be fully understood or accessible. This significant gap suggests that most companies still view ESG primarily as a cost of compliance, rather than a powerful lever for operational efficiency and value creation.

2 Narrowing the Action Gap: Progress and Persisting Challenges

Decisive Shift from Ambition to Measurable Action

The past three years have seen a clear shift from initial ESG ambition to concrete measurable actions. The proportion of businesses with no formal ESG plan has more than halved, falling from 35% in 2022 to just 15% today. However, a critical distinction remains between strategy on paper and action on the ground.

The overarching story is one of significant progress. The conversation has moved beyond if a company needs a strategy to how well it can be executed. The key challenge now is closing the 'action gap' and building the capabilities to translate strategic ambition into measurable impact.

However, only

Leadership Engagement Deepens and Formalises

A key development since 2022 is the formalisation of ESG leadership. Where ambiguity once existed, clearer structures are now taking shape, establishing ESG as a core governance topic that demands accountability from the top.

- Fully empowered ESG leaders are becoming more common, but they are not yet the norm. The proportion of respondents saying their company has ‘no clear ESG leader’ has fallen from 38% in 2022 to just 25% today. However, while leaders are being appointed, half (50%) of surveyed businesses still operate with either distributed roles or limited authority.

- Despite this progress, two critical challenges persist. A concerning 32% say their boards remain completely uninvolved in ESG - a figure unchanged since 2022 - and only 13% demonstrate active, strategic leadership.

This suggests that for many, board involvement is still procedural rather than a deep, strategic engagement integrated across the entire business.

Governance as The Anchor of Understanding and Structure

Our findings show that Governance is the most mature ESG pillar, both in leadership understanding and formal structure. This comfort is reflected in practice, where over half of boards have now formalised oversight through dedicated sub-committees or designated members

Leadership Maturity and Board Oversight in pillars of ESG

34%

Governance

23%

Environmental

21%

Social

In contrast, leadership’s grasp of environmental and social issues is far less developed. This knowledge gap helps explain a recalibration we observe in governance structures. The number of respondents now describing their structure as ‘informal’ has risen to 33%. This trend could be a sign of maturing self-awareness: what passed for a formal structure three years ago is now rightly seen as insufficient for today’s complex demands.

Despite this progress, a concerning 26% say that still have no defined governance structure at all. The overarching challenge is therefore clear: to build upon the solid foundation of governance and develop the same level of expertise and structural rigour for the equally critical environmental and social dimensions.

Data is The New Frontier of ESG Maturity

Over the past three years, the primary challenge for businesses in Vietnam has shifted from understanding what to measure to effectively managing and utilising data. While the knowledge gap has narrowed, with only 18% of companies now lacking data or KPIs, a “three-tier” market has emerged based on data capability.

- Leaders (10%): A sophisticated group leverages Business Intelligence (BI) tools for continuous capture and strategic analysis, moving beyond simple reporting.

- The Developing Majority (47%): The largest cohort is wrestling with manual or inconsistent ESG data collection, resulting in unreliable data that is difficult to analyse or assure.

- Laggards (43%): A significant group remains at high risk, with many still capturing no data at all.

The core challenge is now capability, not awareness. The focus must be on equipping businesses with the systems and skills to leverage ESG data as a strategic asset rather than a compliance burden.

Professionalising ESG Reporting and Assurance

The ESG landscape is progressively maturing, shifting from a focus on initial participation to a drive for professional quality. This has created a stark divide between market leaders and the majority across both reporting and assurance.

Reporting intent has become the norm

Commitment to reporting has become mainstream. The portion of respondents that say they have external reporting has risen to 57% (up from 52% in 2022); additionally, 23% indicate that they plan to do ESG reporting in the next 12 months. However, a ‘developing majority’ (57%) now lacks a structured approach, using no formal standards or operating on an ad-hoc basis. This highlights a significant gap between intent and effective implementation.

In contrast, the proportion of respondents saying they are reporting with established standards has grown significantly to 43% (up from 30% in 2022), demonstrating a clear advancement in sophistication among market leaders.

3 Accelerating ESG Maturity: Internal Hurdles and External Enabler

- A ‘Governance-First’ Approach

- Evolving Hurdles on The Path to Maturity

- A call for Clarity, Capital, and Customised Support

A ‘Governance-First’ Approach

To align with this Vietnam's agenda of achieving high-income status by 2045 and Net Zero emissions by 2050—anchored by government resolutions linking sustainability to economic growth, businesses must accelerate their own ESG journeys.

The path to acceleration, however, is not uniform. It is defined by their stage on the ESG journey, internal priorities, and the specific hurdles it faces, creating a clear demand for tailored support and enabling policies. In response, current corporate priorities in the next 12 months reveal a clear and pragmatic focus on building foundational capabilities first.

The top priorities are unequivocally foundational:

This reflects a pragmatic ‘house-in-order’ strategy, focused on building robust structures and processes.

Evolving Hurdles on The Path to Maturity

As Vietnamese businesses move from ESG commitment to action, they face a new set of hurdles. Our survey shows that these challenges are not static; they evolve significantly as a company progresses, shifting from internal capability gaps to external systemic friction.

- For developing companies, the main barriers are internal. They face a classic resource and capability problem as their primary obstacles. By contrast, external factors are a lower-priority concern as they lack the capabilities to benefit from policies that even exists.

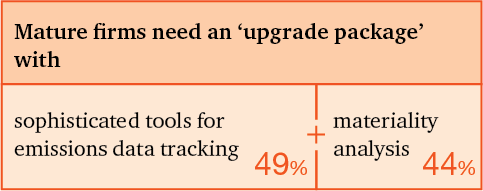

- For mature companies, barriers evolve and become more complex e Primary constraints become external. Meanwhile, internal challenges evolve in complexity. This reflects the shift from the initial challenge of ‘how to start’ to the more demanding, continuous effort of ‘how to scale’ and maintain momentum

A call for Clarity, Capital, and Customised Support

To accelerate their ESG journey, businesses are not waiting for mandates; they are calling for practical enablers. This requires a dual approach: policymakers must provide clear financial incentives and standards, while the service market must offer support tailored to a company’s specific stage of maturity.

From Government: A call for Capital and Clarity

From the Market: Tailored Support from Direction to Precision

Across both groups, two needs are constant: accessing financial resources and integrating ESG into procurement. This shows that funding the transition and managing the value chain are persistent challenges for all.

From sustainability compliance to business reinvention

Embracing the Reinvention Imperative

The global landscape is being rapidly reshaped byadvances in AI, rising climate risks, and geopolitical shifts.

The Strategic Imperative for Vietnam

For Vietnam, this global pivot makes ESG progress a strategic imperative. As regional markets accelerate their shift to low-carbon energy, early investment in clean technologies, energy efficiency, and innovative power solutions positions businesses to capture growth, attractgreen finance, and meet rising international expectations. To fully realise these opportunities, ESG strategies must also ensure respect for human rights and support a justtransition—one that safeguards livelihoods, promotes equity, and leaves no one behind.

From Compliance to Competitiveness

While many Vietnamese businesses currently approach ESG as a compliance exercise, this is a critical opportunity. By integrating ESG into core strategy and operations, companies can move beyond a defensive posture to accelerate maturity and enhance long-term competitiveness.

To advance, businesses must view ESG as a value driver,not just a compliance task, investing in the capabilitiesthat transform ambition into tangible outcomes.

Mastering Reporting and Compliance

Building a robust foundation for transparency and accountability.

- Assess readiness through a technical disclosure gap assessment and organisational maturity assessment across people, process and technology.

- Identify the sustainability impacts, risks & opportunities that matter to your business and your broader stakeholders to determine material sustainability matters and how those interact with your business strategy.

Our approach: Impact management

Identify and understand your business’s impact on planet and people through our comprehensive framework: 360 degree lens.

Harnessing AI and technology

Leveraging data for predictive insights and smarter decision-making.

Create and implement a data and technology strategy with the appropriate data architecture and flows to support the reduction of ongoing regulatory costs.

Optimise the finance function to produce high quality data to measure and forecast performance.

Identify sources of data and the systems used for data collection and consolidation to define data architecture and single source of truth for internal and external reporting.

Our assets: ESG digital tool

Explore our suite of sustainability tools for emissions tracking, benchmarking, and making data-informed decisions.

Driving Efficiency and Margin Improvement

Using sustainable practices to optimise operations and enhance profitability.

The regulatory framework and data insights provided will enhance the business case for transformation and reinvention.

Embed sustainability into business functions, such as finance and risk, to measure, monitor and forecast progress against goals and enable holistic decision making.

Deliver insightful data to unlock margin improvement opportunities and related cost reduction initiatives, like energy demand and waste reduction.

Mitigate potential disruptions and vulnerabilities within a company's supply chain.

Our approach: Sustainable corporate governance

Integrating environmental and social considerations into corporate leadership to drive long-term productivity, impact, and value.

Achieving Business Model Reinvention

Enable long-term growth through Business Model Reinvention

- Evolving regulations will continue to accelerate the need for organisations to reinvent their business models to harness value creation opportunities brought by sustainability regulations.

- Reconfigure your future business model, delivering on the need to decarbonise and adapt to the impact of climate, and strengthen your competitive differentiation.

Our insight: Reinventing your company for growth

The next decade will be defined by transformation from technology and climate change. Businesses that make strategic, 'no-regret' moves today will capture the new domains of growth tomorrow.

New ESG regulations aren’t a risk; they are the single greatest opportunity for differentiation we have today. By embracing collaboration and advanced technology, businesses can turn ESG reporting from a challenge into a strategic lever for innovation, trust, and growth.

Download full report here

ESG Progress Tracker Survey report 2025

Get in touch

Nguyen Hoang Nam

Sustainability and Climate Change (ESG) Leader and Partner, Assurance Services, PwC Vietnam

Tel: +84 28 3823 0796