The EU Corporate Sustainability Due Diligence Directive (CSDDD) marks a major step in how companies are expected to manage human rights and environmental adverse impacts across value chains. It requires large EU companies, and non-EU companies with significant EU turnover, to carry out comprehensive due diligence covering both own operations and business relationships globally.

The application of the Directive will start in 2029, covering companies with more than 5,000 employees and €1.5 billion in net global turnover. Non-EU companies will also fall under the scope if they generate equivalent levels of turnover within the EU market.

At its core, key elements include:

Identification, prevention and termination of adverse human rights and environmental impacts, providing remedy when corresponding.

Integration of due diligence into corporate policies and systems.

Coverage of value-chain activities (i.e. not just immediate suppliers).

Enforcement mechanisms: Member States will designate supervisory authorities who will enforce CSDDD at the country level; companies may face administrative sanctions and civil liability for inadequate due diligence.

For Vietnamese companies, this Directive has far-reaching implications. Even if not directly in scope, local subsidiaries or suppliers of EU companies will increasingly be expected to demonstrate compliance with due diligence standards. This means providing transparency over labour practices, environmental management, and governance systems – and, ultimately, adapting to meet the higher sustainability expectations of EU buyers, parent entities, and investors.

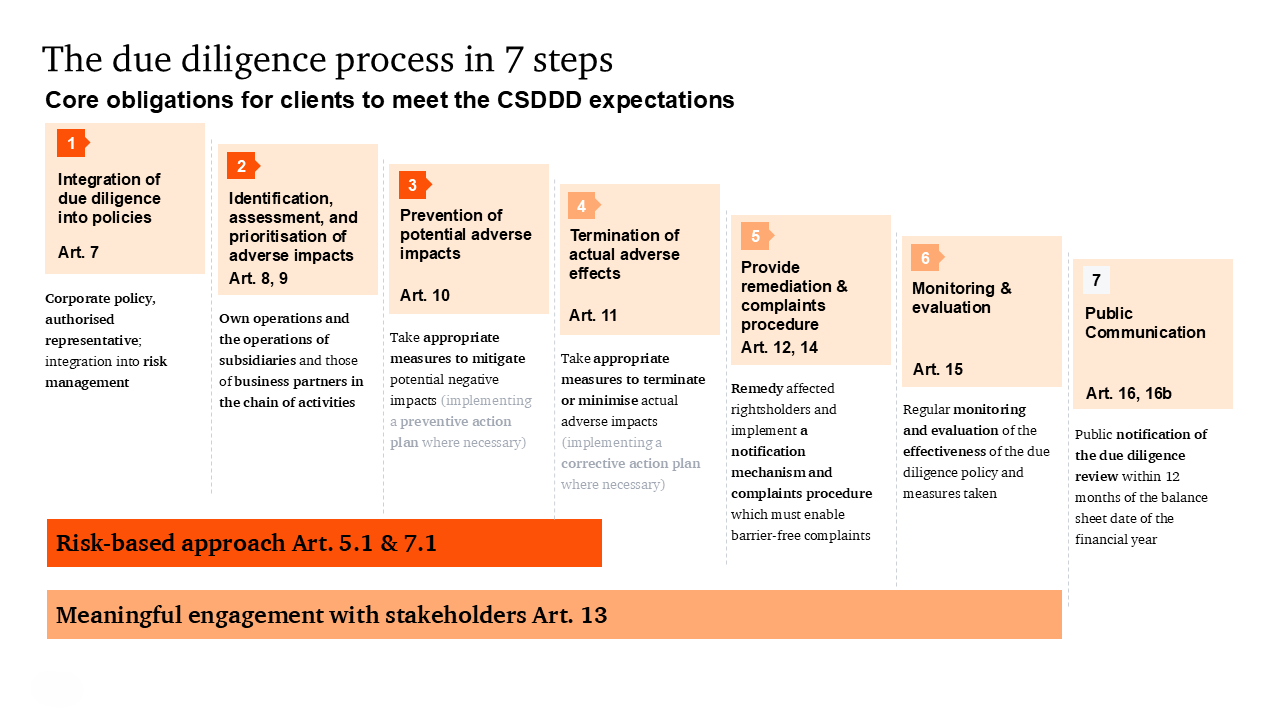

CSDDD core obligations for companies (7 steps)

Companies in scope will typically need to implement the following core due diligence steps (in alignment with the OECD / UNGPs framework):

01

Integrate due diligence into policies and risk management systems

02

Identify and assess actual and potential human rights and environmental adverse impacts across own operations, the operations of subsidiaries, and the operations of business partners, prioritising those impacts where necessary

03

Prevent or mitigate potential adverse impacts

04

Bring to an end or minimise actual adverse impacts, proving remedy when corresponding

05

Establish a notification mechanism and a complaints procedure, covering own operations, subsidiaries, and business partners

06

Monitor the implementation and the adequacy and effectiveness of the due diligence policies and measures

07

Report and publicly communicate efforts

These steps reflect the “appropriate measures” standard under the CSDDD, emphasising processes rather than perfect results. In other words, CSDDD requires an intentional compliance approach instead of a checklist understanding.

Impact on Vietnamese suppliers and local subsidiaries of EU companies – expectations from EU in-scope companies

The information-requesting process and the needs of the in-scope entity will be mostly guided by a risk-based approach, with plausible information of adverse impacts as main driver. For Vietnamese companies that are subsidiaries of EU in-scope entities or suppliers to them, the effects are significant and include:

EU companies will expect due diligence data from you – e.g., risk mapping outcomes, mitigation plans, supplier questionnaires, traceability.

You may be required to align your policies and practices (labour rights, environmental standards, governance) with the EU counterpart’s due diligence obligations.

You may face contractual obligations or supplier code of conduct updates: responsible business conduct commitments, data processing, corrective action timelines, enhanced transparency.

Being in the value chain means your operations could become a focus area for the EU company’s risk assessment – especially if you operate in higher-risk sectors (product, industry) or geographies.

In short: Vietnamese suppliers and subsidiaries of in-scope entities should view the CSDDD not only as a compliance burden for their EU buyers and counterparts, but as an opportunity to strengthen their own resilience, improve reputational standing, and future-proof business relationships.

Foreseeable challenges & suggested responses

Challenges

|

Suggested actions

|

Solutions from PwC Vietnam to support Vietnamese subsidiaries and suppliers of EU companies

PwC Vietnam is well-positioned to support subsidiaries and suppliers navigate the CSDDD-related requirements and turn them into value-creating initiatives. Organised in three key steps –understanding, implementation and forward-looking – our approach consists of the following:

| By leveraging PwC Vietnam’s offering, suppliers and subsidiaries in Vietnam can not only meet the expectations of EU in-scope companies, but also position themselves as trusted partners, reduce business risk, and capture the longer-term benefits of sustainable supply chain practices. |

Conclusion

Connectivity of Vietnamese business to global value chains is being revolutionised by the emerging regulatory requirements. Digitisation, provenance and traceability will be key to demonstrating values, systems, performance and compliance and will integrate across how companies buy, how they operate and how they sell.

The CSDDD is a strong signal that value chain sustainability and responsible business conduct are moving from voluntary aspirations to enforceable obligations for companies in and beyond the EU. For Vietnamese subsidiaries or suppliers to EU-based entities, this shift means heightened expectations, closer scrutiny and deeper collaboration.

Early readiness is not just about compliance – it is about protecting market access, strengthening buyer relationships and embedding sustainability into the heart of your business. PwC Vietnam stands ready to support you on this journey from readiness to resilience and value creation.

Authors