Tax Issues on Operation and Investments in Renewable Energy Business

Tax Issues at Establishment Stage (SPE)

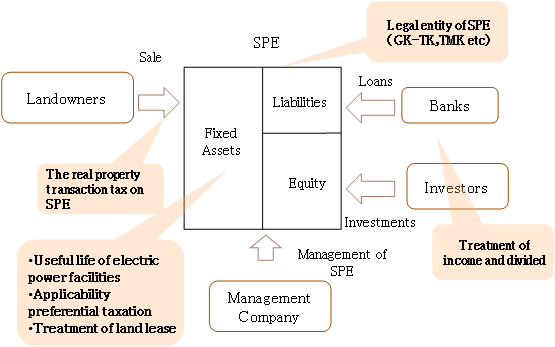

GK-TK (limited liability company/anonymous partnership)

A business operator of an anonymous partnership is subject to corporate taxes. The amount of profit or loss distributed to or assumed by the partnership members in accordance with the partnership agreement, shall be included in calculation of the operator’s loss or profit.

Special Purpose Entity

The amount of profit distributed to the investors shall be included in the calculation of the SPE’s loss, assuming that certain requirements are met. Also, tax relief is offered in relation with the real property transaction tax, which is levied on newly acquired land. However, in cases where the SPE is a key business operator or an asset holding company, consideration is necessary from a perspective of the Act on the Liquidation of Assets.

Tax Issues During the Operating Period

Depreciation of Business Assets

Business assets are generally depreciated in the same manner as other depreciable properties, based on the statutory useful life under the straight-line method or fixed-rate method. As for certain business assets, the green investment tax credits are allowed, where which special depreciation (including immediate depreciation) is recognized in the year the asset becomes available for the use of the business.

Impairment

Impairment recognized for accounting purposes shall not be included in calculation of the loss for tax purpose, unless certain requirements are satisfied.

Land Lease

In the case land lease right is established for the operation of a business, tax treatment of the lease may differ depending on the form of the lease (whether lease practice is accepted in the region etc.).

Business Tax (and Special Local Corporate Tax)

Business tax imposed on an electrical power supplier is based on its revenue instead of profit. The rate of special local corporate tax is 81% of standard business tax rate.

Depreciable Property Tax

Depreciable property is taxed at 1.4% of standard rate. Authorized electric power facilities (certain renewable energy facilities) acquired on and before March 31, 2014 will be charged at two thirds of the standard rate for three years.

Our Team

Partner, PwC Tax Japan