It concerns cross border arrangements between an EU taxpayer and a person or entity in a third country.

It concerns cross border arrangements between an EU taxpayer and a person or entity in a third country.

On 25 May 2018 the ECOFIN Council formally adopted the Directive on mandatory automatic exchange of information in the field of taxation in relation to reportable cross-border arrangements (DAC6). The main purpose of DAC6 is to strengthen tax transparency and fight against aggressive tax planning through the disclosure of cross-border arrangements, CRS avoidance schemes and offshore structures.

DAC6 requires disclosure to the relevant EU tax authority of a cross-border arrangement entered into by an EU taxpayer which bears any of the prescribed hallmarks.

It concerns cross border arrangements between an EU taxpayer and a person or entity in a third country.

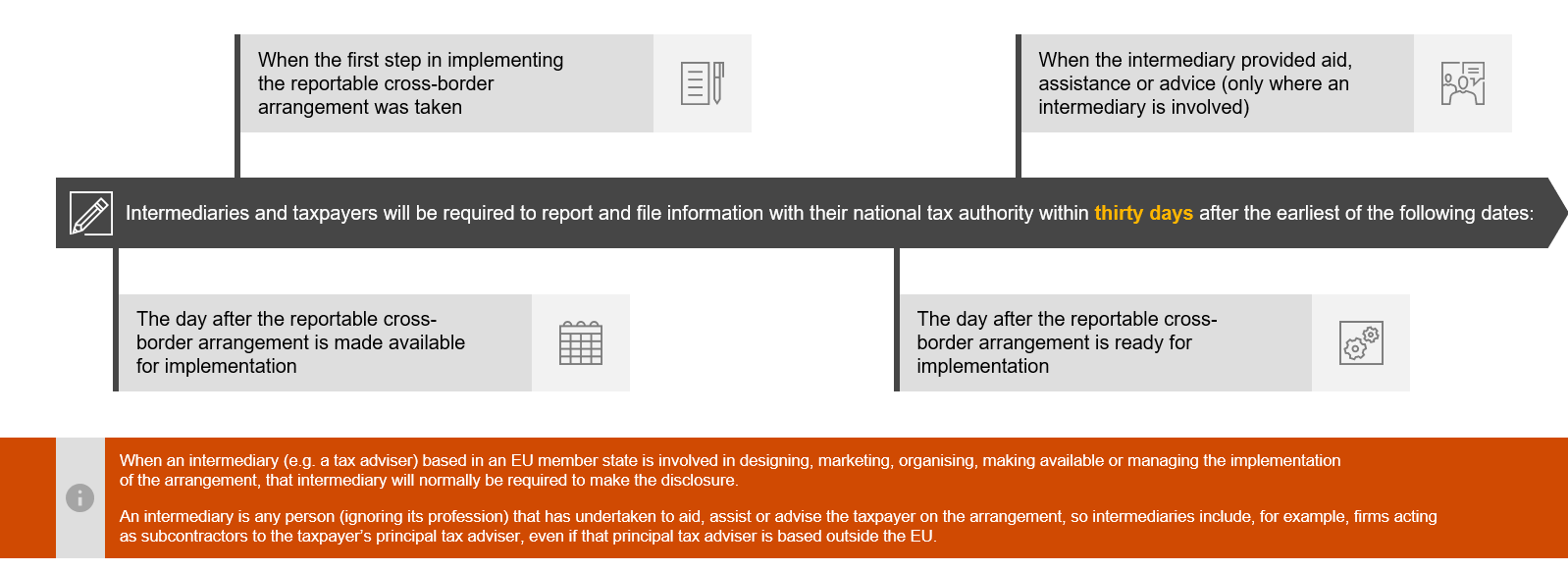

An obligation to report certain information about relevant cross border arrangements

Failure to comply will result in penalties and reputational risk for the taxpayer/intermediary.

The hallmarks are very broadly defined and many commercial transactions might fall within the scope of the reporting obligation, even though they are not tax driven.

There are six broad categories of hallmarks covering different types of cross-border arrangements. Some of the hallmarks are subject to a tax main benefit test, so they are relevant only if the main benefit, or one of the main benefits, of the arrangement is obtaining a tax advantage. The other hallmarks do not require there to be any tax benefit.