Effective from 01.01.2026, amendments to the Law “On Taxes and Fees” will come into force, applicable from the reporting year starting in the 2025 calendar year.

These amendments are aimed at reducing the administrative burden for taxpayers and improving the efficiency of transfer pricing risk management in Latvia.

Key amendments to article 15.2

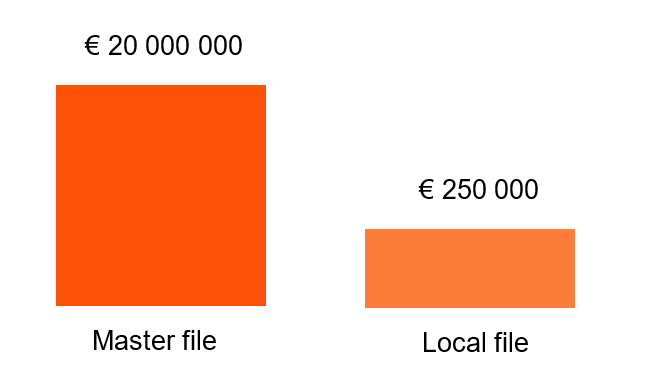

1. Changes with respect to the preparation of Master file and Local file

- Master file must be prepared if the sum of related party transactions in the relevant reporting year exceeds EUR 20,000,000.

- Local file must be prepared if the sum of related party transactions in the relevant reporting year exceeds EUR 250,000.

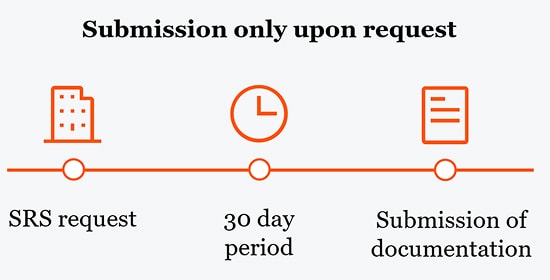

2. Changes in the submission of Master file and Local file

- Submission only upon request: Local file and Master file must be submitted only upon receipt of a request from the State Revenue Service (SRS) within 30 days.

- Documentation submitted via the SRS Electronic Declaration System (EDS) has legal force even if it does not contain the “signature” attribute.

3. Changes with respect to the preparation and update of Local file

Each Local file must be reviewed and fully updated once every three years, provided there are no significant changes affecting the transfer pricing methodology. However, financial data within the Local file must be updated annually.

4. Changes in the review of comparable financial data

- Each benchmarking study must be prepared anew every three years.

- Financial indicators of previously accepted comparables are adjusted annually using the roll-forward approach for two consecutive years.

- The price (value) applied by the tested party is updated every year.

5. Changed threshold for significant controlled transactions

The threshold for significant controlled transactions has been increased from EUR 20,000 to EUR 90,000.

6. Introduction of the controlled transactions report

A “Controlled Transactions Report” must be prepared, which is transfer pricing documentation in a structured data format and contains information about the taxpayer’s controlled transactions. This includes information on the type of transaction, direction, total amount, transaction partner, method used to determine the arm’s length price (value), source of comparable data, tested party, arm’s length price (value), selected arm’s length price (value) indicator, and the applied arm’s length price (value) metric.

Submission procedure and threshold: The report must be submitted to the SRS Electronic Declaration System (EDS) within 12 months after the end of the relevant reporting year. The report must be prepared if the sum of controlled transactions in the relevant reporting year exceeds EUR 250,000. The report in EDS must be submitted in a structured data format.

Illustrative general PwC example “SIA X Controlled Transactions Report” FY2025:

*If the applied market price metric falls within the market value range determined by comparable data, no corrections are required in line 6.5 of the CIT declaration.

To understand how structured reports are prepared in other countries, PwC Latvia provides an example from Poland’s controlled transactions report section regarding the declaration of information on comparability analysis.

Impact and Benefits

These amendments will provide significant benefits for both taxpayers and the tax administration:

- Reduced administrative burden and costs: Many taxpayers will no longer have to automatically submit Local file and Master file every year, but only upon request from the SRS. Additionally, updating documentation once every three years will significantly reduce the financial burden and time consumption for taxpayers.

- More effective risk analysis by SRS: The structured controlled transactions report will enable the SRS to perform semi-automated identification and analysis of transfer pricing risks, maintaining a high level of control and reducing the need for manual information searches.

- Latvia’s competitiveness: The revised documentation requirements are aimed at making Latvia even more attractive to foreign investors, promoting economic development.

We invite you to attend a free webinar (in Latvian)

Significant transfer pricing amendments to be applied from the reporting year starting in 2025

Contact us