EU Sustainable Finance and the increasing importance of ESG factors in accessing finance

What is ESG?

The evolution of corporate sustainability

Sustainability emerged as a topic in the 80s from environmental issues to a broader set of subjects. It has evolved from the “do no harm” and public relations approach of “CSR” to a holistic approach of creating and protecting value through proactive management and reporting of environmental, social and economic impacts as well as stakeholder concerns and expectations. The pursuit of achieving sustainability and alongside with the changing of global era has urged and transformed the investments to be not only financially but also social and environmentally sustainable. Therefore, there is an arising need for the development of a regulatory framework that defines sustainable investments and links Environmental, Social and Governance (ESG) factors in the investment decision–making process and access to funds. Corporate sustainability criteria are now core issues guiding the ever-increasing “sustainable” or “ESG” investing.

Linking Sustainability and CSR to Sustainable investment

Investors are increasingly factoring sustainability considerations into their investment decisions and portfolio management strategies

According to a PwC Private Equity Responsible Investment Survey conducted on 2019, with a total sample of 162 respondents, the following significant results were arisen:

81% of respondents report ESG matters to their Boards at least once a year

67% of respondents have identified and prioritised Sustainable Development Goals (SDGs) that are relevant to their investments (compared to 38% in 2016)

91% of respondents have already adopted or are currently developing a responsible investment or ESG policy

83% of respondents are concerned about climate risks in their portfolio

Linking ESG to financing and investment activities

EU Sustainable Finance Regulation aims to support EU to achieve three ambitious climate and energy targets by 2030.

Targets - Issue - Solution

- EU Committed to specific environmental targets

- The issue

- The solution

EU Committed to specific environmental targets

40%

Reduce greenhouse gas emissions compared to 1990

32%

At least a 32% share of renewables in final energy consumption

30%

At least 30% energy savings compared with the business-as-usual scenario

The issue

The annual EU investment gap to meet these targets is estimated to be between € 175 to 290 billion.

The solution

The financial sector will be part of the solution and will play a critical role in achieving the EU’s sustainability goals. The purpose of the EU Sustainable Finance Regulation is to finance sustainable growth that will help the EU to achieve the 2030 goals.

What are the objectives of the new regulation:

- Establish a unified EU classification system of sustainable economic activities (‘taxonomy’).

- Improve disclosure requirements on how investors integrate environmental, social and governance (ESG) factors in their risk processes.

- Create a new category of benchmarks which will help investors compare the carbon footprint of their investments.

- Protecting private investors by avoiding risks of green washing.

- Providing the basis for further policy action in the area of sustainable finance, including standards, labels, and any potential changes to prudential rules.

Six key elements of the Sustainable finance regulation:

Standards for green financial products

EU Green Bond Standards and ecolabels for financial products, defining minimum ESG requirements and terms.

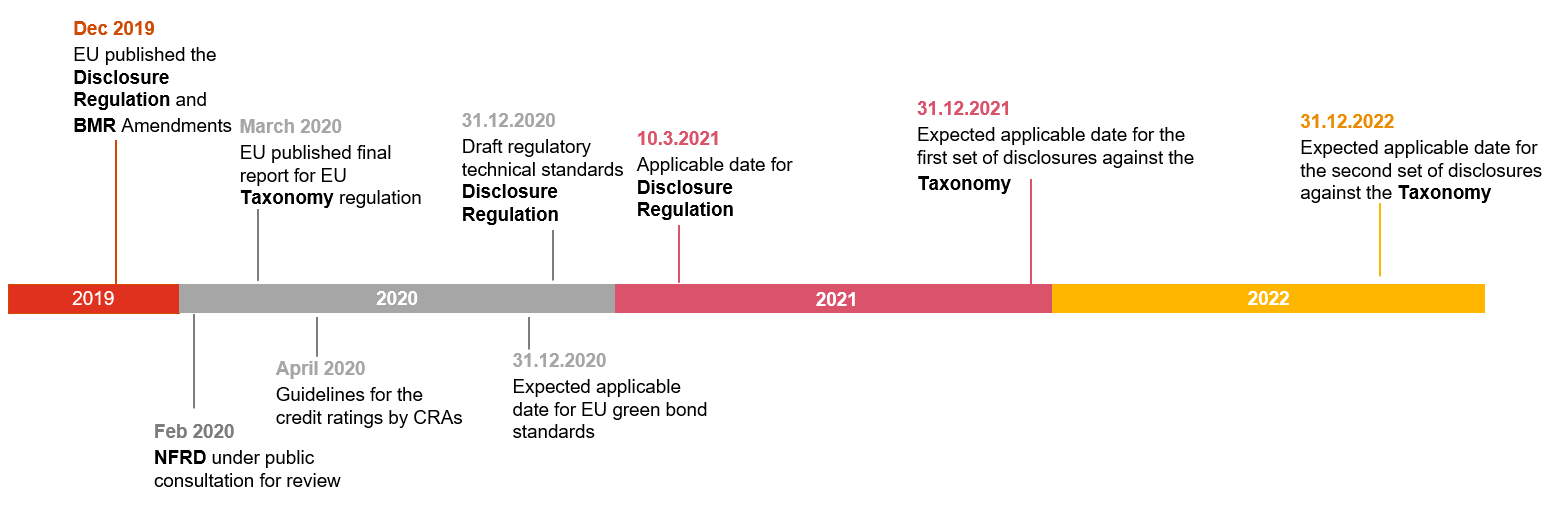

Report issuance date: By 31/12/2020

Credit Ratings

Guidelines and disclosure requirements for integrating ESG factors into credit ratings by CRAs

Date of applicability: 01 April 2020

ESG Benchmark Regulation (BMR)

Requires companies that publish financial benchmarks & indexes to disclose how they incorporate ESG factors into their calculations.

Date of applicability: 1/1/2022

Taxonomy

Index, including minimum thresholds for key ESG KPIs. Environmental threshold for shipping will be CO2 emissions.

Economic activities: Agriculture and forestry, Manufacturing, Electricity, gas, steam and air conditioning supply, Water, sewerage, waste and remediation, Transport, ICT and Buildings.

Date of applicability: 1/1/2022

Non-Financial Reporting Directive (NFRD)

EU law requires large companies to disclose certain information on the way they operate and manage social and environmental challenges.

Public consultation for review launched: 20/2/2020

ESG Disclosure Regulation

Framework defining the minimum content to be disclosed by financial market participants, including web site disclosures.

Date of applicability: 10/3/2021

Overview of the six key policy areas of the sustainable finance regulation

Description – Current Stat |

Applicability Date |

|

|---|---|---|

Taxonomy |

The Taxonomy Regulation is an index, including minimum thresholds for key ESG KPIs. More specifically, this regulation will affect the following economic activities: Agriculture and forestry, Manufacturing, Electricity, gas, steam and air conditioning supply, Water, sewerage, waste and remediation, Transport, ICT and Buildings. The Council adopted the lawyer linguist text on 15 April 2020 (https://data.consilium.europa.eu/doc/document/ST-5639-2020-REV-2/en/pdf). The final vote in the Parliament is anticipated in May 2020 for publication in Official Journal in June 2020. |

1/1/2022 (first set of disclosures 1/1/2023 (second set of disclosures) |

Benchmark Regulation (BMR) |

The Regulation on Climate Benchmarks requires companies that publish financial benchmarks & indexes to disclose how they incorporate ESG factors into their calculations. The Regulation was published in December 2019 (https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32019R2089) and will become binding for benchmark administrators from 30 April 2020. |

1/1/2022 |

ESG Disclosure Regulation |

The Disclosure Regulation constitutes a framework defining the minimum content to be disclosed by financial market participants, including web site disclosures. The Regulation was published in December 2019 (https://eur-lex.europa.eu/eli/reg/2019/2088/oj). Part of Regulation will be amended by the Taxonomy Regulation. |

10/3/2021 |

Non-Financial Reporting Directive (NFRD) |

EU law requires large companies to disclose certain information on the way they operate and manage social and environmental challenges. The Commission is consulting on a revision of the NFRD. The proposal of the renewed legislative act will be announced in December 2020 or in the first months of 2021. |

Proposal for the new regulation: December 2020 |

Standards for green financial products |

EU Green Bond Standards and ecolabels for retail financial products, defining minimum ESG requirements and terms. The technical Expert Group adopted a report in March 2020, suggesting a creation of voluntary EU Green Bond Standard through a legislative procedure. Commission’s Joint Research Centre (JRC) published a draft proposal within the second technical report in December 2019 regarding the ecolabel criteria (https://susproc.jrc.ec.europa.eu/Financial_products/docs/20191220_EU_Ecolabel_FP_Draft_Technical_Report_2-0.pdf). The final criteria will be published by JRC in Q1 2021, which will then be adopted under the EU Ecolabel Regulation. |

Report issuance date: By 31.12. 2020 |

Credit ratings by CRAs |

Guidelines and disclosure requirements for integrating ESG factors into credit ratings by Credit Ratings Agencies (CRAs). In July 2019 ESMA published the guidelines on disclosure requirements (https://www.esma.europa.eu/sites/default/files/library/esma33320_final_report_guidelines_on_disclosure_requirements_applicable_to_credit_rating_agencies.pdf). |

01 April 2020 |

ESG requirements and reporting

What will banks and investors request from companies?

Banks and investors will periodically increase their ESG requests. We believe that relevant ESG requirements will evolve in 3 phases. We are now in Phase 1.

Phase 1: Focus in environment

- Request annual data mainly related to environmental performance.

- Ensure that the investment or activity to be financed complies with all applicable regulations and financing standards (i.e. ESMS)

Phase 2: Disclose complete ESG performance

- Incorporate in relevant requests Social and Governance related metrics.

- Disclose ESG performance through annual reports.

- Develop measures consistent with the industry requirements and comparable over the years.

- Perform 3rd party assurance over the respective KPIs.

Phase 3: Improve ESG performance

- Establish an ESG strategy, depicting short and long term commitments.

- Define an action plan in order to improve ESG performance.

- Become taxonomy eligible.

- Achieve higher ESG ratings.

- Link ESG performance with financing terms.

Why monitor and report ESG performance?

- Meet the requirements of investors and financial institutions.

Investors, funds and financial institutions are increasingly taking into consideration the ESG performance of companies. As a result, companies that demonstrate transparency, and good performance in ESG related matters achieve higher ESG ratings and enjoy better access to funding as well as more favorable financing terms. - Access to capital markets.

Investors assessing organizations' sustainability performance in the context of good corporate governance and risk management. The transparency of how (well) an organization is addressing sustainability builds trust with investors. Sustainability performance improves brand and reputation. - Improve performance.

Companies are increasingly trying to improve performance related to issues such as environmental impact, people wellbeing, health and safety and business ethics. It is therefore required to continuously monitor KPIs related to ESG and compare against targets and industry peers.

- Gain a competitive advantage.

Companies that understand the implications of sustainability to their business models can use this information to both enhance and develop new products and services. For example (a) first mover advantage and (b) reputational position in new and/or growing markets. - Demonstrate ethical and socially responsible business practices.

At its core, ESG and sustainability promote business ethics and social prosperity, thus adopting and promoting sustainable practices enhances both of these causes and allows companies to obtain a social license to operate.

Related content

Follow us