Working efficiently and effectively to help you stay ahead of the curve.

One size does not fit all. Your firm and its partners are unique. You know where you want to go and need a team that’s built around your specific law-firm needs to get you there.

It’s deep expertise. It's a connected perspective that comes from a global team sharing, insights and best practices who can deploy specialized resources across the major US markets and offer the in-country knowledge you need to transact successfully.

Our community of solvers thrive on the unexpected. We’ll deploy the innovative tech powered solutions that accurately and efficiently handle the ins and outs of your global, national and local assurance, tax and operational needs. We’ll keep your growth in focus.

How PwC can help

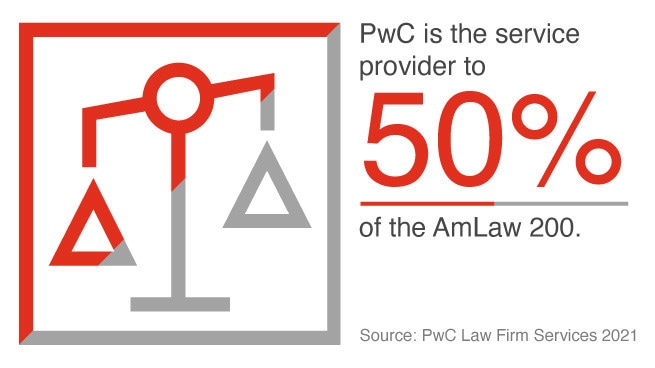

We provide a comprehensive range of services and unparalleled industry and technical knowledge to assist law firms and their partners.

Trust solutions (Assurance and Tax services)

Insights to act with confidence to build trust. We’re a connected team with unparalleled experience in the issues your firm and partners are facing. We will work with you to keep your goals in focus through the delivery of solutions tailored to meet your needs. It’s about keeping you ahead of the curve with smarter tech and specialists who truly understand your firm and its business. That’s why leading firms look to PwC to meet their assurance and financial reporting needs, provide a greater understanding of the fundamentals of law firm operations to inform their business decisions, as well as to assist in navigating the complexities of multi-jurisdictional taxation, including global structuring to maximize tax efficiency.

Find out more about our capabilities below.

Consulting solutions

Business as usual is not an option for law firms. You’re embracing how technology, disruption and client demands can change your business and operating models for the better. Our community of solvers will come together in unexpected ways to help you turn today’s turbulence into long-term transformation and sustained outcomes by tackling:

- Cybersecurity & privacy

- Finance effectiveness

- Mergers & acquisitions - due diligence and other considerations

- Operations

- Pricing & profitability

- Strategy

- Technology

- Workforce transformation

Law firm benchmarking

For almost 60 years, we’ve armed premier law firms with comprehensive benchmarking information on a broad range of management topics important to law firm leaders. We invite you to join our community with this benchmarking program which can allow your firm to gain a deeper understanding of its position in the market, identify potential opportunities to improve profitability and make better informed strategic decisions.

Three ways you can get involved:

The Law Firm Accounting and Financial Management publication, authored by PwC, delivers explanations and illustrative exhibits on the latest management, tax planning and accounting strategies for law firms; new information reporting requirements; and special issues affecting multinational firms.

It’s packed with insights and tried-and-trusted information including:

- Fundamentals of law firm financial information

- Financial management concepts

- Tax planning and reporting

- Law firm structures

- Advanced accounting and financial considerations for law firm management

Beyond those basics, our specialists also dive into the latest trends and implications for sustained outcomes in: managing risk; management information reporting; benchmarking; M&A accounting and strategies for successful mergers; capital structures and financing; the uniform task-based management system; and partner compensation.

Related content

Follow us