{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

In February we published the Middle East findings of PwC’s annual Global Consumer Insights Survey (GCIS), just before governments across the region took rapid and decisive action to contain the COVID-19 pandemic. This new report is based on a GCIS COVID-19 Pulse – a snapshot survey that analyses how attitudes and habits of urban consumers in the region have been affected by lockdown. It identifies key regional trends to watch in a retail landscape likely to be impacted by social distancing and other virus-suppression measures for some time to come. The report focuses specifically on urban consumers to provide a timely update for businesses in the region about how better to understand this group following the unprecedented shock of the pandemic.

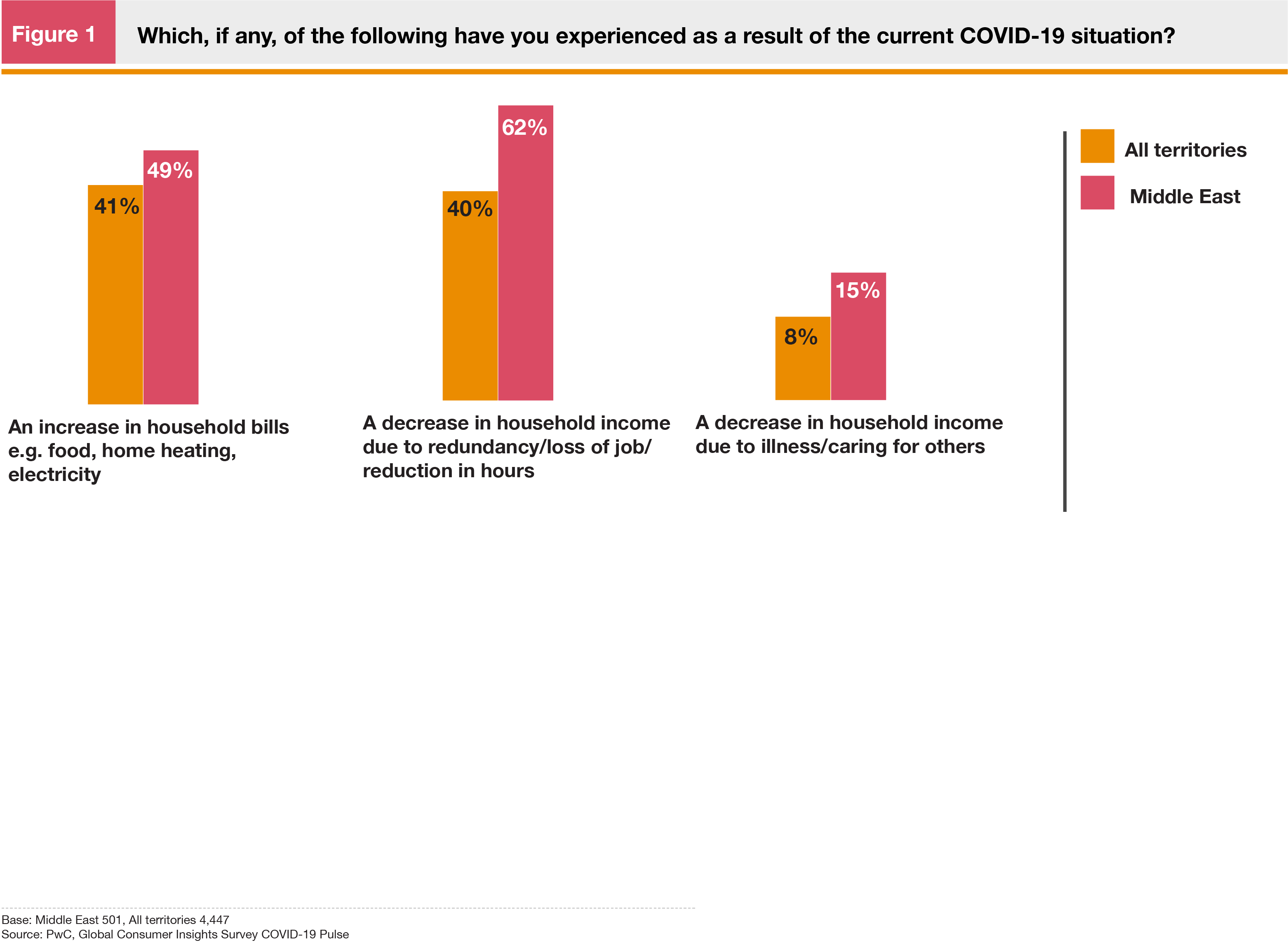

While 62% of the Middle East survey respondents said they had experienced a decrease in household income due to redundancy or reduction in hours (Figure 1) – the highest proportion of any territory surveyed – almost half (49%) expect to spend more in the next few months. This is a reduction from 63% pre-pandemic but higher than the all territories average of 33% (Figure 4).1 In the region, this trend is mostly led by Cairo, where 64% are planning to spend more (Figure 5).

On the other hand, a third of regional respondents to our COVID-19 Pulse expect to spend less in the short term, whereas pre-pandemic, just 13% of Middle East respondents expected to curb their spending in the next 12 months. In this fragile retail environment, where another spike in infection rates could puncture consumer confidence, our findings indicate that COVID-19 and measures taken by governments to control the spread of the disease have added greater momentum to three existing regional trends:

We surveyed 501 consumers in Abu Dhabi, Cairo, Dubai, Jeddah and Riyadh as part of a wider PwC global survey of the impact of COVID-19 on consumers. The majority (87%) of the Middle East survey respondents were aged between 18 and 44, with 13% older than 45. Three-quarters (73%) came from households with children and two-thirds were either in full-time employment (53%) or part-time work (11%). The survey was conducted between 1 and 13 May 2020.

Overall, 62% of Middle East survey respondents said they had experienced a decrease in household income due to redundancy or reduction in hours – the highest proportion of any territory surveyed. An additional 15% had lost out on earnings as a result of caring for others or illness, meaning 77% in total reported a fall in household income, compared with an all-territory average of 48% (Figure 1).

Within these regional figures were some notable differences between the results from different cities. For example, 61% of consumers in Jeddah said they had seen an increase in household bills such as food, air cooling and electricity as a result of COVID-19, markedly more than their counterparts in Abu Dhabi (40%), Riyadh (48%), Dubai (49%) and Cairo (50%). However, these contrasts between cities were less significant than the wider evidence that COVID-19 has damaged the finances of most urban consumers in the Middle East (Figure 2).

The speed of the spread of the pandemic has had a devastating impact on the global economy, bringing with it a rise in financial concerns and employment security worries. However, having to stay indoors due to imposed local lockdown measures, what COVID-19 did bring for some was the much needed time to rethink, reevaluate and reset.

When we published our pre-pandemic Middle East findings in February, health and wellness were already in focus. More than half (58%) of respondents said they were making time each week to improve their health and general wellness as well as adopting a better diet. This desire for a healthier lifestyle arguably grew stronger during lockdown. In the current survey, over half the respondents “strongly agreed” that they are more focused on taking care of themselves because of COVID-19, across the following categories: mental health and wellbeing (83%); physical health and fitness (85%); diet (84%); and medical needs (88%).

These figures were significantly higher than the equivalent all-territory results for the four categories, which were 69%, 69%, 63% and 64% respectively (Figure 3).

This phenomenon of a care-centric customer base and business culture could be one of the positives to come out of the COVID-19 pandemic. In the near term, companies focused on health and wellness – food manufacturers that offer healthy, nutritious products and grocery chains that sell local and organic products, for example, will continue to thrive.

Despite their financial anxieties, it is striking that 49% of Middle East respondents still expect to spend more in the next few months (Figure 4), ahead of China (43%), France (39%), Germany (38%) and the UK (33%). Shoppers in Cairo led the way, with 64% expecting to spend “much more” or “slightly more”, compared to 39% of consumers in Dubai planning to spend “much more” or “slightly more” in the coming months (Figure 5).

Nonetheless, their buying habits will be different. Prior to lockdown, urban consumers prioritised travel, accommodation and entertainment, based on the regional findings we published in February – respondents identified travel (41%) and restaurants (42%) as two of the top three ways they chose to spend their disposable income. However, as a result of COVID-19 consumers say they are now spending more on groceries (61%) and entertainment and media (41%). Revealingly, given fear of catching the virus, 37% report that they are shopping less often for groceries, but filling up bigger baskets.

Meanwhile, expenditure by Middle East urban consumers on clothing and footwear has fallen 50% since the outbreak, in line with a similar drop (47%) for all territories. Restaurant food delivery and pick-up have witnessed the second biggest fall in the Middle East (42%), a markedly steeper decline than the all-territory average (33%) (Figure 6).

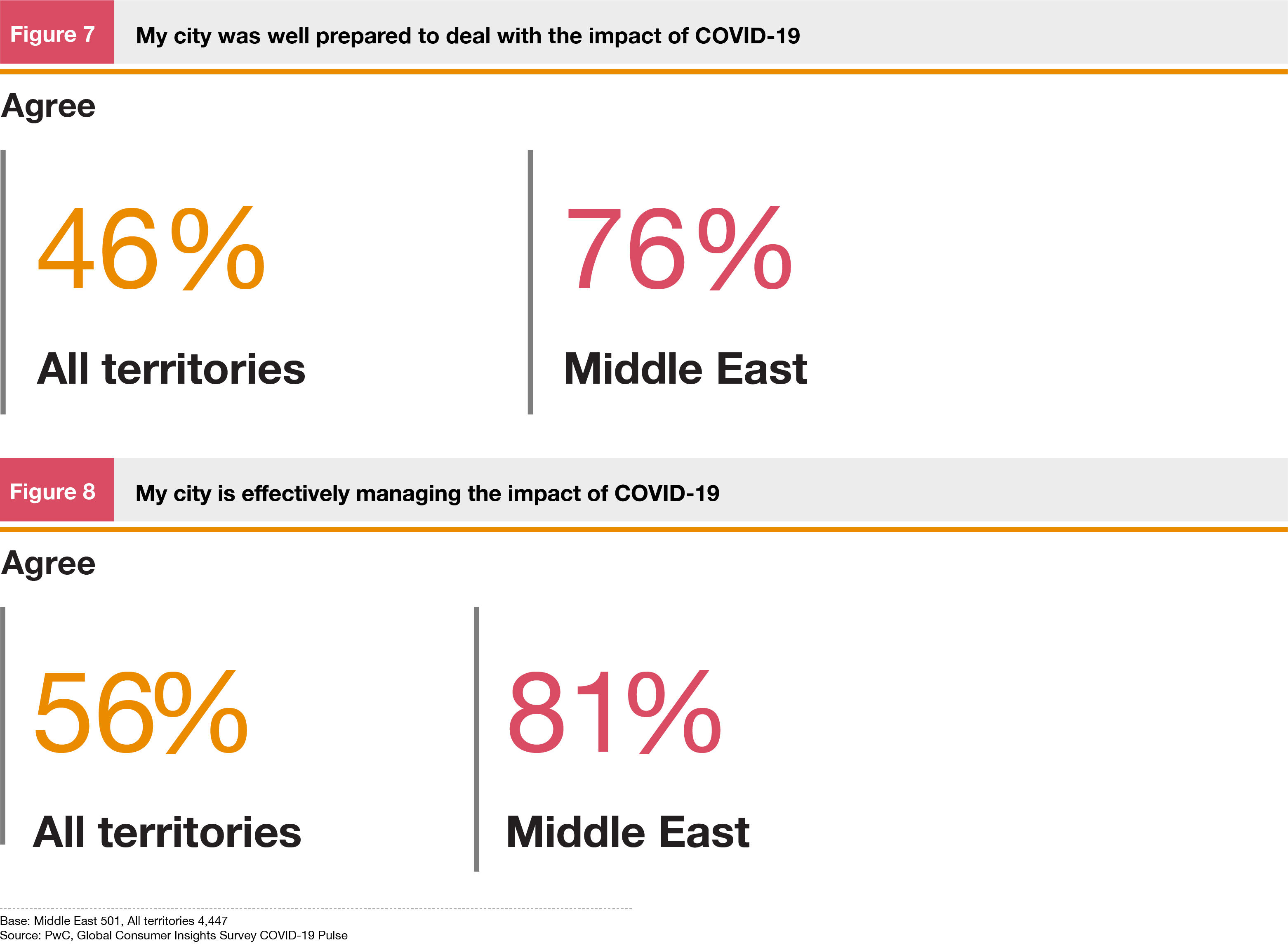

The level of confidence going forward among Middle Eastern shoppers could be explained by the region’s strong response to COVID-19. 76% of Middle East consumers agreed that their city had been well prepared to deal with the impact of COVID-19 – far more than the 46% for all territories (Figure 7). Furthermore, 81% of Middle Eastern respondents agreed that their city was managing the pandemic effectively, compared with 56% across all territories (Figure 8).

Even so, Middle Eastern consumers are transitioning from lockdown into a bricks-and-mortar retail landscape where measures to contain the virus are likely to remain in place for months. In this unsettling context, shared by consumers around the world, our findings indicate that COVID-19 has accelerated three regional consumer trends that have been growing in importance in recent years.

In PwC’s 2019 Global Consumer Insights Survey, we highlighted that the use of mobile payments by Middle Eastern respondents had increased from 25% in 2018 to 45% – a bigger increase than any other region. The findings we published in February 2020, before the Middle East went into lockdown, provided further evidence of the increasing popularity of mobile payment channels and shopping via smartphone throughout the region: at that time, 31% of Middle East consumers used their mobiles for daily and weekly shopping, and 44% said they had placed an order using a mobile app, more than the global survey average of 38% (Figure 9).

Our COVID-19 Pulse survey conducted in May 2020 found that 53% of Middle East respondents had increased their use of smartphones for shopping in response to the pandemic, compared with 34% for all territories in the survey. Meanwhile, 39% of the Middle East survey said they had increased their shopping via computer, with 31% using a tablet more often for purchases. These results are unsurprising because many consumers would have been using multiple devices as a result of working from home or simply browsing to pass the time while adhering to local lockdown measures. Also not surprisingly, 49% said they had reduced their in-store shopping, in line with the survey average (Figure 10).

The results suggest in particular that shopping via smartphones will continue to rise after lockdown ends, with 92% of those consumers who increased their shopping via smartphone reporting that they were “very likely” (63%) or “likely” (29%) to continue with this purchase method once social-distancing measures are removed (Figure 10). We must remember that unlike the Western world, mobile shopping still continues to be a growing trend here in the region. The impact of COVID-19 has forced change: consumers who were previously resistant to using mobile payment channels discovered that purchasing goods and services on their smartphone was not only easy but convenient too.

However, this is only one aspect of a more complex emerging picture of the post-lockdown balance between clicks and bricks shopping in the Middle East, in a retail setting where COVID-19 is a continuing threat and social distancing measures remain in force.

Online grocery shopping has been on the rise across the Middle East in recent years. In last year’s survey, 73% of respondents in the region said they were likely to purchase groceries online in the next 12 months, up from 58% in 2018. In our pre-pandemic findings published in February 2020, only 16% of Middle East respondents said they had not bought any groceries via the internet during the previous year, lower than the global average of 23%.

Findings from the COVID-19 Pulse survey in May 2020 indicate that the pandemic has predictably strengthened the online grocery shopping habits of consumers in the Middle East’s leading retail centres. Around half (51%) of respondents said they were shopping for groceries online or by phone, either to pick up in-store (18%) or, more commonly, to be delivered to their homes (33%). This is an increase of 24% compared to before COVID-19 when only 27% of Middle East respondents in February 2020 said they were shopping for groceries “exclusively” or “mainly” online.

More than half (57%) of Middle East consumers in the COVID-19 Pulse survey who indicated that they mainly do their grocery shopping online or by phone also reported that they were buying more groceries when they ordered remotely, compared with before the pandemic. For some respondents, it appears that the experience of online shopping during lockdown has broken down previous resistance to shopping for food and household items via the internet. In total, 92% said they were either “very likely” (56%) or “likely” (36%) to continue doing their grocery shopping online once the social distancing rules have ended (Figure 11).

Three-quarters (75%) of the Middle East survey said they had increased their consumption of social media such as Facebook, Instagram, Twitter and TikTok as a result of social distancing and other isolation measures, substantially more than the average of 52% for all territories. In parallel, 71% of Middle East respondents reported that their usage of WhatsApp, WeChat and other messaging apps had increased since the outbreak of the pandemic, while 54% said they were using video chat apps like FaceTime, Zoom and House Party more often. These results highlight that social media, messaging and video chat apps were an essential lifeline for many consumers looking to stay connected to their family, friends and the community as whole during lockdown.

As with online grocery shopping, this rise in social media and messaging usage appears to be here to stay among consumers in the region. Overall, 95% of Middle East consumers who said that their social media use has increased indicated they were either “very likely” (70%) or “likely” (25%) to continue using social media to the same extent as they have during lockdown once COVID-19 containment measures are removed, with almost identical proportions for the equivalent question on messaging apps. Meanwhile, 90% of the regional survey expected to carry on using video chats, split between 53% who said it was “very likely” and 37% who thought it was “likely” (Figure 12).

It is too soon to tell how these intentions will influence short-term and long-term consumer behaviour as the Middle East emerges from lockdown and the pandemic is eventually suppressed. However, one message from our results is already clear: companies with established digital solutions had a competitive advantage and were able to capitalise on consumers’ time indoors. Going forward, retailers from entertainment to groceries will need to be able to reach their customers via social media, both for marketing purposes and to better understand their expectations.

Our latest, post-pandemic results suggest that consumer-facing businesses should keep a close watch on several trends that have accelerated since the pandemic reached the region.

Most strikingly, the lockdown has prompted more urban consumers who were previously resistant to change to try out online retail channels, with most respondents willing to continue to use them once the pandemic is over. It therefore appears certain that digital engagement by Middle East shoppers will become stronger and more widespread, even after the lifting of current social distancing measures. In this increasingly digital market landscape, retailers will need to leverage insights gained from data analytics to target consumers and meet their expectations as closely as possible.

At the same time, retailers will need to find the appropriate balance between their online offering and traditional stores. Our survey results show that consumers are not only buying more products online and, in some cases, using online retail services for the first time. They are also exploring alternative ways to choose or substitute products – for example, by combining initial store visits with subsequent online purchases. Price and value will consequently become critical for retailers as they chase increasingly sophisticated, internet-savvy customers, both online and in-store. The growing pre-pandemic demand for digital payment and credit solutions, reflected in our February findings, has also been further boosted by the lockdown.

In addition, COVID-19 has reinforced the importance of health and wellness for urban Middle East consumers. This accelerating trend is shifting spending patterns, with relatively more spent on food and greater variations in purchasing choices across the non-food sector. To respond effectively, retailers will need to develop a wider range of health and general wellbeing products, with the focus shifting away from discretionary categories such as clothing and footwear.

Above all, the key watchwords for Middle East retailers following the pandemic will be agility and resilience. Coming out of lockdown, businesses that successfully pursue consumers who are increasingly at ease with online shopping will emerge as winners in a challenging market where customer loyalty cannot be taken for granted.

To analyse how consumer attitudes and habits have been affected by social distancing, PwC surveyed 4,447 consumers from China, the UK, France, Germany, Italy, the Middle East, Netherlands, Spain and Sweden for the Global Consumer Insights Survey COVID-19 Pulse. The territories were selected because they were at different stages of recovery from COVID-19.

In the Middle East, we polled 501 consumers between 1 and 13 May 2020. Respondents were from a cross-section of industries and were based in Abu Dhabi (103), Cairo (102), Dubai (102), Jeddah (93) and Riyadh (101).

Before COVID-19 survey results refer to PwC’s 2020 Global Consumer Insights Survey Middle East findings released in February 2020. 2019 data is from PwC’s 2019 Global Consumer Insights Survey Middle East report.

Not all figures add up to 100% as a result of rounding percentages.

For views of consumers around the globe, see the global report from the same period.

1) Territories that participated in Global Consumer Insights Survey COVID-19 Pulse: China, France, Germany, Italy, Middle East, Netherlands, Spain, Sweden, UK (“all territories”)