The International Energy Agency highlights in its net zero scenarios that building new, low-emitting assets and technologies is one of four key broad sets of measures to achieve emissions reductions. Climate tech is showing strong growth as an emerging asset class globally, but the Central and Eastern Europe (CEE) region has only attracted less than one percent of global investments.

The CEE edition of PwC’s Net Zero Future50 report, produced in partnership with Wolves Summit, presents a first look of its kind at the state of climate tech investment in 27 countries and 8 sectors across the CEE region and features a selection of 50 climate tech start-ups.

In Central and Eastern Europe, sustainability goals have also become security goals. We have even more motivation to work toward the goals set out by the European Green Deal: reducing CO2 emissions by at least 55% by 2030, and achieving climate neutrality by 2050. Net zero obligations and the need for energy independence and security will not be met by business as usual. One of the most exciting ways of making progress is to scale up the impact of climate tech solutions – and to match investor funding with climate tech entrepreneurs.

The climate tech investment landscape in CEE

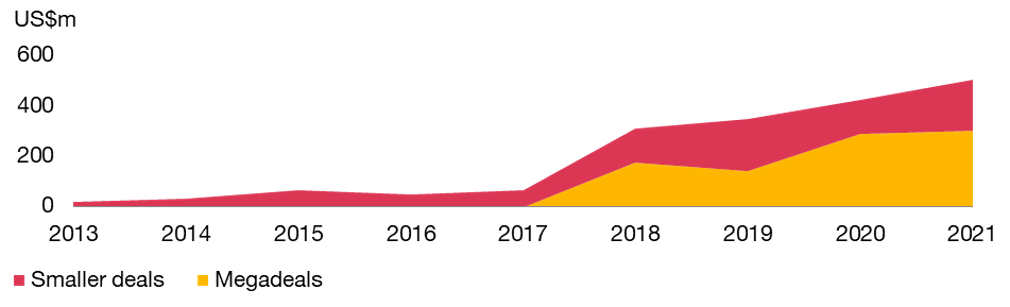

Climate tech investments in CEE are showing steady growth, with more than US$1.76 bn invested between 2013 and the first half of 2021. Investments have risen from US$10.6m in 2013 to US$398m in 2020, and to over US$502m in the first half of 2021 alone.

This rapid growth is mainly driven by the rise of megadeals (deals valued at more than USD $100m) in sectors such as Mobility and Transportation, and Industry, Manufacturing and Resource Management.

CEE Climate tech start-up funding by deal size

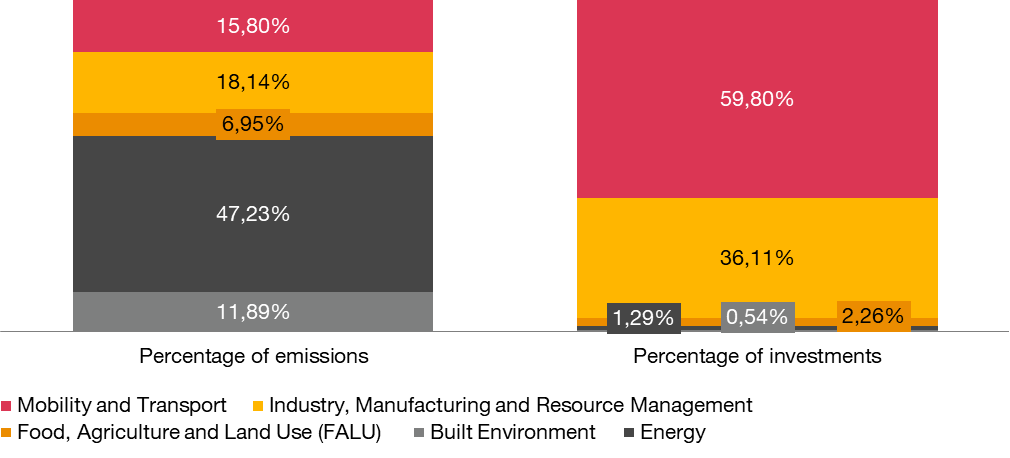

The CEE region as a whole only contributes approximately 3.73% of global GHG emissions. At the same time, the region’s share of global climate tech investment is just 0.79% of the total. Given that many countries in CEE are showing positive economic growth, it is crucial to ensure more funding flows to scaling up decarbonisation technologies in the region.

Comparing climate impact against climate investments in CEE

Climate tech investments in CEE are heavily concentrated in the Mobility and Transport sector (59.8%). Most notably, between 2013 and first half of 2021 CEE start-ups in the Food, Agriculture and Land Use sector attracted just 2.26% of total funding, and those in the Energy sector a mere 1.29%.

Breakdown of investment by sector

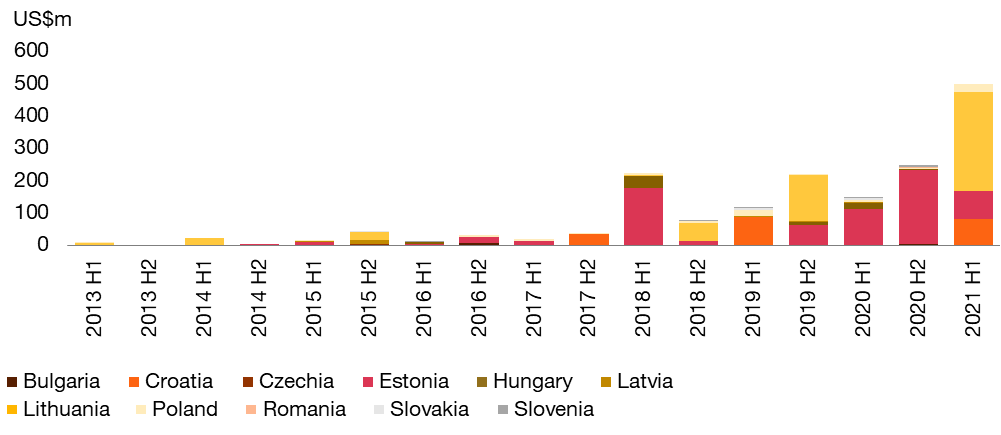

Estonia and Lithuania-based start-ups have raised 74.8% of total CEE climate tech funding. Tallinn (Estonia), Vilnius (Lithuania), and Sveta Nedelja (Croatia) are the top three most active climate tech investment hubs in the region. Although Poland has the largest economy in the region, and it serves as a strategic hub for some industries, start-ups in Poland only raised 4.65% of total CEE climate tech funding.

Breakdown of investment by country

Sector breakdowns

- Built Environment

- Climate Change Management and Reporting (CCMR)

- Energy

- Financial Services

- Food, Agriculture and Land Use (FALU)

- GHG Capture, Removal and Storage

- Industry, Manufacturing and Resource Management (IMRM)

- Mobility and Transport

Built Environment

11.89% Share of CEE GHG emissions |

9 Start-ups in the Net Zero Future50 report – CEE Edition |

0.54% Share of total investment for H1 2013 - H1 2021 |

Climate Change Management and Reporting (CCMR)

N/A Share of CEE GHG emissions |

3 Start-ups in the Net Zero Future50 report – CEE Edition |

N/A Share of total investment for H1 2013 - H1 2021 |

Energy

47.23% Share of CEE GHG emissions |

10 Start-ups in the Net Zero Future50 report – CEE Edition |

1.29% Share of total investment for H1 2013 - H1 2021 |

Financial Services

N/A Share of CEE GHG emissions |

N/A Start-ups in the Net Zero Future50 report – CEE Edition |

N/A Share of total investment for H1 2013 - H1 2021 |

Food, Agriculture and Land Use (FALU)

6.95% Share of CEE GHG emissions |

12 Start-ups in the Net Zero Future50 report – CEE Edition |

2.26% Share of total investment for H1 2013 - H1 2021 |

GHG Capture, Removal and Storage

N/A Share of CEE GHG emissions |

1 Start-ups in the Net Zero Future50 report – CEE Edition |

N/A Share of total investment for H1 2013 - H1 2021 |

Industry, Manufacturing and Resource Management (IMRM)

18.14% Share of CEE GHG emissions |

9 Start-ups in the Net Zero Future50 report – CEE Edition |

36.11% Share of total investment for H1 2013 - H1 2021 |

Mobility and Transport

15.80% Share of CEE GHG emissions |

6 Start-ups in the Net Zero Future50 report – CEE Edition |

59.80% Share of total investment for H1 2013 - H1 2021 |

CEE Net Zero Future50 start-ups

Leveraging the Wolves Summit community of 8,000+ start-ups and 3,700+ investors across Europe, PwC and Wolves Summit identified over 170+ start-ups and invited them to present an application for potential inclusion in the report.

PwC ESG professionals in Warsaw then assessed the applicants against a range of indicators across three categories (maturity stage, scalability, climate impact), and shortlisted 50 climate innovators as an indicative illustration of the state of climate tech start-ups in the region.

Historically, founders in CEE lacked the networks, funding and connections that entrepreneurs in Western Europe and the US could otherwise easily tap into. We are now starting to witness more specialised accelerator programs and impact funds designed to speed up the maturation of climate tech start-ups in this region. It’s clear that the best days for Central Eastern Europe remain ahead of us.

CEE Net Zero Future50 start-ups composition

- By country

- By sector

By country

CEE Net Zero Future50 start-ups by country

Twelve countries are represented in this cohort of 50 start-ups: Poland (14), Estonia (13), Lithuania (5), Ukraine (4), Latvia and the Czech Republic (3 each), Croatia and Romania (2 each) and Bulgaria, Hungary, Slovakia and Serbia (1 each).

By sector

CEE Net Zero Future50 start-ups by sector

In terms of sector, there are represented: Food, Agriculture and Land Use (12), Energy (10), Built Environment (9), Industry Manufacturing (9), Mobility (6), climate change management and reporting (3), and GHG, capture, removal and storage (1).

Looking at the average start-up profile, it is clear that most start-ups are in the early stages of their journey. Only 20% of start-ups have secured Series A/B funding. The remaining 80% are either bootstrapped or operating off of seed funding or grants. Interestingly, 40% of the CEE Future50 start-ups report to have limited understanding of their technologies’ emission reduction potential.

Start-ups should consider implementing early-on impact assessment methodologies to support their value proposition. Investors are increasingly expecting to know their portco’s climate impact and this area should not be overlooked to secure future funding and stakeholder support.

The new report’s analysis suggests that the climate tech ecosystem in CEE is in its early days, especially when compared with more developed climate tech hubs – or other start-up hubs in general. The findings suggest that currently the right class of investor for the overall climate tech ecosystem in CEE are early-stage venture capitalists who are actively seeking to invest in pre-seed, seed, growth, and early stage companies.

About the report

The PwC Net Zero Future50 report – CEE Edition looks at the state of climate tech in our region and features a selection of 50 climate tech start-ups.

The following CEE countries are covered in the report (27 in total): Albania, Armenia, Azerbaijan, Bosnia and Herzegovina, Bulgaria, Croatia, Czech Republic, Estonia, Georgia, Hungary, Kazakhstan, Kosovo, Kyrgyzstan, Latvia, Lithuania, North Macedonia, Mongolia, Montenegro, Moldova, Poland, Romania, Serbia, Slovakia, Slovenia, Turkmenistan, Ukraine, Uzbekistan.

Climate tech is defined as technologies that are explicitly focused on reducing greenhouse gas (GHG) emissions, or addressing the impacts of global warming. The 8 sectors of focus are based on the PwC climate tech taxonomy. Learn more at PwC State of Climate Tech.

The PwC Net Zero Future50 – CEE Edition start-ups were selected from an application and selection process which took place in between May and July 2022. We focused on analysing the size of the prize in terms of environmental and commercial impact, their maturity and their potential to scale to achieve breakthrough results.

Sign up for a further discussion

Contact us

Agnieszka Gajewska

Global Government & Public Services Leader | CEE ESG Leader, PwC Central and Eastern Europe

Tel: +48 517 140 537

José Miguel Salazar Hernández

CEE ESG Hub, Manager, PwC Central and Eastern Europe

Tel: +48 519 505 899

CEE Director of Brand and Communications, PwC Central and Eastern Europe

Tel: +48 519 506 633

Marta Laskowska

CEE Digital Marketing & Brand Manager, PwC Central and Eastern Europe

Tel: +48 519 505 529